PhilStockWorld Investing Strategies 101 - Notes from the AGI Round Table

Usually when we talk about medical diagnosis, there is this underlying expectation of, well, absolute precision.

Penny:Right, like it's math or engineering.

Roy:Exactly. Like you fall off a bike, You break your arm, you go to the hospital and the x-ray shows that jagged white line on a black background.

Penny:Yeah, it's undeniable.

Roy:Right. The doctor just points to the screen and says, you know, there it is. That is the problem. It's a completely binary reality. It's broken or it's not broken.

Roy:It's clean, it's measurable and the path to fixing it is well, it's standardized.

Penny:You put a cast on it. Simple.

Roy:Exactly. But then, and this is where it gets crazy, you step out of the hospital and into the world of the stock market and suddenly that beautiful precise x-ray machine is just completely shattered.

Penny:Oh completely, it's gone.

Roy:Right. We were looking at a diagnostic landscape that is honestly, it is terrifyingly murky. Most retail investors are just walking around in the dark, you know, squinting at shadows, hoping they accidentally stumble into a pile of money without tripping over a recession.

Penny:Yeah. And the sheer volume of variables makes it the absolute definition of diagnostic muddy waters. You aren't just looking at one bone here. You're trying to diagnose geopolitics, fragile global supply chains, the collective manic depressive psychology of millions of traders. All at once.

Penny:Right, all at the exact same time, throw in algorithmic high frequency flows and central bank monetary policy, it is frankly fundamentally impossible for a single human mind to hold all of those moving pieces in focus at once.

Roy:Which brings us to today's deep dive. Because today, we are looking at a stack of sources, primarily a 07/07/2026 portfolio review from PhilStockWorld.

Penny:Yeah. Part 47.

Roy:Right. Part 47 of a massive 360 part series that is tracking a strict $700 a month retail portfolio. And we're also pulling in some heavy hitting quantitative research from Sparkline Capital.

Penny:Some really fascinating data in there.

Roy:Truly. Because the mission of this deep dive is to figure out how one investor, Phil Davis, basically solved that impossible diagnostic problem you just mentioned.

Penny:Yeah, it's quite a journey.

Roy:We're going to trace how he evolved from like a lone data architect into the creator of a literal council of hyper specialized artificial general intelligences, the AGI Roundtable.

Penny:Which is such a wild concept when you first hear about it.

Roy:It really is. We'll explore how he synthesized the greatest investing minds of the past century, how he applies Seth Klarman's strict margin of safety to a modern AI driven landscape, and most important we're going to distill his philosophy into three actionable daily habits.

Penny:Things people can actually use.

Roy:Exactly. Habits you can apply to your own smaller investment accounts to stop gambling and start building structural wealth.

Penny:Because that transition from gambling to statistical architecture, that is the entire thesis of his platform.

Roy:Right.

Penny:What we are looking at in these sources is a completely new paradigm. It's AI enhanced investor education. The AGI Council isn't designed to be like a black box hedge fund that just trades automatically while humans sleep.

Roy:It's not just a trading bot.

Penny:No, not at all. It is an educational scaffolding. It combines human scar tissue, meaning decades of lived market experience, the painful lessons you only learn by bleeding real capital in bear markets.

Roy:Oh, yeah. The hard way.

Penny:Right. It combines that with the raw parallel processing power of AGI. So the AI acts as this high speed structural auditor, you know, mapping constraints and modeling thousands of potential outcomes while the human maintains the ultimate executive judgment.

Roy:Let's unpack this with a mental image because I think this fits perfectly. Think about trying to build wealth in the market like walking into a massive neon lit casino.

Penny:Okay. I like that.

Roy:Most retail investors, probably a lot of people listening to this right now, you know, you walk through those shiny gold doors Yeah. Hoping to hit the jackpot on a single machine.

Penny:Just pulling the lever.

Roy:Exactly. You pull the lever on a highly volatile tech stock, you watch the cherry spin and you just pray. You're relying entirely on hope and momentum.

Penny:Which is a terrible strategy.

Roy:It is. But this deep dive, this is about learning how to own the slot machines. It is about understanding the underlying math of the casino.

Penny:Because the casino operator doesn't care if the guy pulling the lever wins or loses on any given Tuesday. Right. The operator cares that the plumbing of the casino, guarantees that the house edge slowly, relentlessly accumulates wealth over thousands of pulls.

Roy:Yes. But to understand how you build that casino plumbing for a relatively tiny $700 a month retail portfolio, we kind of have to examine the architect himself. Right?

Penny:Yeah. You don't just wake up on a Tuesday and decide to build a collaborative council of super smart AI entities to trade options.

Roy:I mean, I definitely didn't do that last Tuesday.

Penny:Right. Phil Davis' background is the crucial context here because he didn't start as a traditional Wall Street floor trader yelling orders in a pit. No. His roots are entirely in systems architecture and massive data management.

Roy:Yeah. The sources show that before PhilStockWorld even launched, which was back in 2006, by the way, he was deep in the tech trenches. He was building systems that had to manage chaotic, unstructured complexity at scale.

Penny:Real heavy lifting data stuff.

Roy:Yeah. You worked with companies like Accutitle, which was a real estate title insurance software platform, and AccuSearch, a property data aggregator that eventually got sold off to Datatrace around 2004.

Penny:Right. So we are talking about managing millions of rows in property records, liens, and legal data, and forcing all of that chaos into a logical, accessible structure.

Roy:And that structural mindset? Well, it's everything.

Penny:It absolutely is. When you spend your early career architecting massive relational databases, you learn that every complex system operates on underlying rules.

Roy:Right.

Penny:But the truly fascinating pivot in his background was his work on an early algorithmic behavioral matching system called Personality Plus.

Roy:This part blew my mind.

Penny:Oh, it's wild. This was back in 2004, long before the massive consumer social media platforms we have today were running deep behavioral matching. He was already exploring how you can take chaotic human behavior, you know, emotions, preferences, relationships and map them onto a statistical probability matrix.

Roy:Okay, wait, hold on. You're telling me a dating algorithm or a behavioral matching system from twenty years ago translates to stock market dominance. Like, how does matching personalities have anything to do with trading options on Nike or Apple?

Penny:Well, think about it. The stock market is, at its absolute core, just a giant emotional behavioral engine driven by money.

Roy:Okay. Yep. That makes sense.

Penny:It is a real time ledger of human fear, greed, panic, and euphoria. What Phil realized was that you can map market participants the exact same way you map personality traits.

Roy:Wow.

Penny:Yeah. So when a stock drops 20% on a missed earnings report, the subsequent price action isn't just a math equation, it is a behavioral cascade.

Roy:Because retail traders panic sell.

Penny:Right. And institutional algorithms trigger stop losses, and then value funds step in to buy at support levels. If you understand the behavioral matching logic, if you understand who is acting and why they're acting, you can model the statistical probability of the stock's next move.

Roy:So he treats the market as a probabilistic behavioral system, not a crystal ball.

Penny:Exactly. He isn't looking for the quote unquote next big thing based on a gut feeling. He is hunting for mathematical anomalies within that behavioral system.

Roy:Okay. So he takes this systems first behavioral data approach, but he doesn't just invent a new investing philosophy out of thin air.

Penny:Yeah. Not at all.

Roy:The sources show he basically went into the lab and synthesized the greatest minds in the history of finance. Like, he stood on the shoulders of giants. And he started with the absolute godfather of value investing, Benjamin Graham.

Penny:From Graham, Phil extracted the concept of intrinsic value.

Roy:Which is pretty famous.

Penny:Right. The philosophy is brilliantly simple in theory. A company is not just a glowing ticker symbol on a screen. It is a living, breathing business with assets, cash flow, and a tangible, calculable worth.

Roy:Right.

Penny:So Graham taught that you calculate that intrinsic value and you only buy the stock when the manic depressive market offers it to you at a price significantly below that worth.

Roy:But, and here is where the Sparkline Capital research we are looking at comes into play. It throws a massive wrench into traditional Graham value investing.

Penny:Oh, a huge wrench.

Roy:The Sparkline data specifically highlights how Graham's old school method, you know, buying stocks, trading strictly below net liquidation value, relying on tangible book value, it's completely broken today.

Penny:Yeah. It just doesn't work the way it did in 1950.

Roy:Why is that?

Penny:Because the entire nature of the global economy has inverted. In Graham's era, like the nineteen forties and fifties, the American economy was overwhelmingly industrial. Value was physical.

Roy:Like actual stuff?

Penny:Yeah. It was steel mills, railroad tracks, massive warehouses full of physical inventory, heavy machinery. In that environment, the book value on a balance sheet was a highly accurate proxy for the real liquidatable value of the company.

Roy:Because if the company went bankrupt tomorrow, you could just sell the blast furnaces and make your money back.

Penny:Exactly. But look at the S and P 500 today. The biggest companies in the world don't own blast furnaces.

Roy:They own code.

Penny:They own algorithms, patents, and brand recognition. The SmartLine study actually proved this mathematically. It shows that pure formulaic value investing, like, if you were to just run a screener and buy stocks based strictly on low priced book ratios, has massively underperformed the broader market for nearly two decades.

Roy:Wait. Really? Two decades?

Penny:Yeah. It has been a literal drag on portfolios since 2007. The traditional value factor is broken because a balance sheet built for a nineteen fifties railroad simply cannot accurately value a 2026 artificial intelligence software firm.

Roy:Which is exactly why PhilSynthesis didn't stop with Graham. He recognized that intrinsic value is real, but the formula for calculating it had to evolve.

Penny:Right.

Roy:And this led him to integrate the teachings of Philip Fisher. Now, Fisher wrote a seminal book in 1958 called Common Stocks and Uncommon Profits. He was the pioneer of what he called the scuttlebutt method.

Penny:I love that word.

Roy:Right? Scuttlebutt always sounds like pirate slang to me, but in finance, it means getting out of the spreadsheet and getting into the real world. It is deep, qualitative, fundamental research.

Penny:Precisely. Fisher argued that you can't understand a business just by reading its quarterly 10 ks filings. Yeah. The numbers look backward, but the business moves forward.

Roy:Right. So, what does scuttlebutt actually look like?

Penny:It involves talking to a company's suppliers. Are they ordering more raw materials? It involves talking to their competitors. Are they terrified of a new product launch? You evaluate their commitment to long term research and development.

Penny:You judge the integrity and vision of the management team.

Roy:It's all the soft stuff that doesn't show up in a standard ratio.

Penny:Exactly. Fisher shifted the focus from finding cheap, dying companies what Buffett used to call cigar butts

Roy:to

Penny:finding highly mature companies with sustainable, qualitative growth 'cigar engines.

Roy:And speaking of Buffett, he is the third pillar here. The sources trace how Buffett started as a strict 'Graham disciple' But eventually, heavily influenced by his partner Charlie Munger and by Fisher, Buffett evolved.

Penny:Yeah, he changed his entire approach.

Roy:And Phil tracked this evolution closely. Buffett moved past the rigid book value formula and started heavily weighting his portfolio toward what Sparkline defines as intangible moats.

Penny:An intangible moat is a competitive advantage that you cannot physically touch, but which absolutely prevents competitors from stealing your market share.

Roy:Like what? Give me an example.

Penny:Brand equity. Think of the psychological grip Coca Cola or Apple has on consumers. It is intellectual property, network effects, human capital. Right. The sparkline quantitative data proves that Buffett's long term historical out performance isn't just magic.

Penny:It is statistically driven by systematic exposure to two modern factors, intangible value and high quality. He targets highly profitable, durable businesses with deep intangible trenches dug around their cash flows.

Roy:Okay. I have to stop you here. Because if I am a retail investor listening to this, I am throwing my hands up in the air right now. You are telling me that to successfully navigate the 2026 market using this synthesized approach, I have to, like, accurately calculate a modern version of intrinsic value perform endless qualitative Fisher style scuttlebutt on global supply chains and competitor sentiment A and D accurately assess the intangible brand moats and R and D pipelines of thousands of public companies.

Penny:Yeah, that's the job.

Roy:But human brains literally cannot process that without melting. That is a physically impossible amount of data for one person to track. By the time I finish analyzing the supply chain of one semiconductor company, the macro environment has shifted and my entire analysis is completely useless.

Penny:You are absolutely right. It is impossible. A human being cannot do it alone. Cognitive fatigue sets in.

Roy:We get tired.

Penny:We get tired, we get emotional, we anchor to our initial research, and we develop massive confirmation bias. And that exact realization is the catalyst for the entire PhilStockWorld architecture. Phil realized his own human bandwidth was the bottleneck. So instead of trying to force his brain to process the fire hose of global market data, he reverted to his 2,004 systems architecture roots. He stopped trying to be the sole analyst and became the architect of a system that could do the heavy lifting for him.

Roy:The AGI Roundtable.

Penny:Yes. He built a collaborative council of specialized artificial general intelligences.

Roy:And these aren't just like basic stock screeners?

Penny:No, no. These aren't simple stock screeners. They are advanced language and logic models designed to handle the massive parallel processing required by the synthesized Graham Fisher Buffett philosophy. They do the scuttlebutt at scale, they map the intangible moats, they process the macroeconomic data instantly, while fill the human with the scar tissue and the emotional intelligence sits at the head of the He reviews the synthesized data and he maintains the final executive judgment on risk management.

Roy:And risk management is where we have to bring in the final legend in this synthesis, Seth Klarman. Because if you have an AGI Council processing billions of data points to find highly profitable companies with intangible moats, you might be tempted to just go all in on aggressive growth.

Penny:Which a lot of people do, to their detriment.

Roy:Right, but Klarman's philosophy acts as the defensive titanium shield around this AGI system. Klarman wrote a legendary out of print book in the early ninety's called Margin of Safety. And his core thesis is that risk is infinitely more important than return.

Penny:Klarman flips the traditional retail mindset completely upside down. When most people open a brokerage account, their very first thought is, how much money can I make?

Roy:Oh, 100%.

Penny:They look at a chart, they project a 30% gain, and they click buy. Klarman argues your very first thought, your absolute obsession must be how much can I lose and how do I absolutely prevent it? Yeah. In Klarman's framework, value investing is a bottom up, absolute performance, aggressively risk averse strategy. The goal is not to beat the S and P 500 index by 2% every single quarter.

Roy:Right. It's not about the relative game.

Penny:No. The goal is absolute unshakable survival across decades of market chaos.

Roy:He famously focuses on opportunity costs too. Klarman argues that holding cash isn't a failure to invest. Cash is actually a highly strategic offensive position when no genuine mathematically sound bargains are available.

Penny:Exactly. Cash gives you the liquidity, the ammunition to strike exactly when everyone else is over leveraged and forced to sell during a panic.

Roy:McLorman also acknowledged a very dark truth about finance: valuation is an imprecise art, and the future is fundamentally, structurally unpredictable. No matter how good your models are, a black swan event can wipe out your thesis overnight. A pandemic, a war, a sudden regulatory shift.

Penny:That is exactly why you demand a margin of safety. You must buy at such a steep, calculated discount to intrinsic value that even if your fundamental analysis is slightly wrong or the macroeconomic environment unexpectedly shifts against you, you are protected from permanent capital loss.

Roy:Because the discount absorbs the error.

Penny:Exactly. The discount absorbs the error.

Roy:So the obvious question is, how do you mathematically define and locate that margin of safety in the hyper fast algorithmic AI driven market of July 2026?

Penny:That's the million dollar question.

Roy:Right. This is where we get into the actual mechanics of the AGI Roundtable. And the sources outline this council beautifully. I look at this AGI team like a highly specialized medical board at a top tier research hospital.

Penny:Oh, I like that analogy.

Roy:Yeah, if you go in with a complex multi system illness, you do not want a general practitioner just taking a wild guess. You want a cardiologist looking at the heart, a vascular surgeon mapping the blood flow, a neurologist checking the brain, and an anesthesiologist monitoring your vitals all arguing over your chart in real time. Right. You would never want the cardiologist performing the brain surgery.

Penny:No, that would be a disaster. The domain specialization is exactly what makes the architecture robust. Phil does not use one monolithic black box AI that just spits out by Apple. He uses a council of specialized lenses, and they often debate and contradict each other.

Roy:Which is by design, right?

Penny:Completely by design. It exposes the blind spots in any given trade thesis. Let's look at the roster he has built. At the strategic level, you have Quijote.

Roy:Quijote.

Penny:Yes. Quijote is designated as the chief visionary and truth engine. His specific parameter is to look at long range structural logic and to violently combat market misinformation. He is looking at what the architecture of a sector will realistically look like three to five years from now, completely ignoring tomorrow's earnings whisper numbers.

Roy:Right. So Quixote is looking at the horizon. Markets in the short term are driven by human beings panicking. That is where Anya comes in.

Penny:Well Anya is fascinating.

Roy:Anya is the Chief Market Psychologist. She acts as the right brain of the operation. While Quixote is analyzing a 10 ks filing, Anya is running natural language processing across Reddit forums, institutional analyst notes and financial news transcripts.

Penny:She's basically reading the room.

Roy:Exactly. She is measuring the velocity of fear and the density of euphoria. If a stock is dropping, she doesn't care about the PE ratio. She cares about the capitulation point of the retail herd. She maps the human behavioral cascade that Phil used to map with personality plus.

Penny:Then you have Anya's counterpart, Zephyr. Zephyr is the left brain, the chief macro logician. Zephyr's job is to ingest the absolute deafening chaos of global data.

Roy:All the numbers.

Penny:All of them. Real time market ticks, bond yield curve inversions, global shipping freight rates, currency fluctuations, and distill it into clean, actionable, mathematical data streams.

Roy:That's incredible.

Penny:And crucially, sitting next to Zephyr, you have Hunter. Hunter is the systems level analyst dedicated entirely to political and economic risk. Hunter maps constraints of reality.

Roy:Meaning what exactly?

Penny:Meaning the power dynamics, the institutional money flows, the legislative gridlock, and the regulatory incentives.

Roy:Okay, let's pull a concrete example straight from the July 2026 sources to show how this council actually diagnoses a market event. Because the theory is great but seeing it in action is wild. Let's talk about the situation with SpaceX ticker symbol SPCX.

Penny:Oh this is a perfect example of Hunter in action.

Roy:Right. So SpaceX was slated for inclusion into the Nasdaq 100 Index. So for the listener, when a massive company gets added to a major passive index like the Nasdaq, every single index fund and ETF that tracks the Nasdaq is legally forced to buy the stock. They literally have no choice.

Penny:It's mechanical.

Roy:It was estimated that this inclusion would trigger roughly $8,000,000,000 in forced mindless institutional buying.

Penny:And the retail forums, the gamblers were losing their minds over this.

Roy:Well, they were foaming at the mouth.

Penny:They looked at that $8,000,000,000 demand shock and concluded that the stock was going to experience a violent historic short squeeze. They were buying short term out of the money call options basically expecting the stock to rocket up 30% in a day, the narrative was intoxicating.

Roy:But the AGI roundtable didn't care about the narrative. Hunter looked at the actual mechanical constraints of the event. Hunter mapped out what he called the flow wall. Explain how Hunter dismantled this retail dream.

Penny:Well, Hunter looked past the demand and analyzed the supply.

Roy:Right.

Penny:He recognized that while there were trillions of dollars in passive tracking assets poised to force 8,000,000,000 in buying, the actual freely trading supply of SpaceX stock the float was incredibly constrained. Ah. The founders, early venture capital backers, and insiders held the vast majority of the shares tightly locked up. The freely trading fleet was only about three to 5% of the total company.

Roy:So you have an $8,000,000,000 fire hose of demand trying to force its way through a 3% supply straw. I mean, the surface, that sounds like it guarantees an explosion in price.

Penny:It does. If you assume the market is a fair transparent auction happening on the day inclusion

Roy:Which it isn't.

Penny:Which it absolutely isn't. Hunter understands institutional mechanics. Hunter mapped out the reality the massive Wall Street market making firms knew this inclusion was coming for months. They didn't wait for the day of the event to buy.

Roy:Of course not.

Penny:They had already quietly, methodically accumulated the necessary inventory of shares over the preceding weeks. They absorbed the float early. So when the 8,000,000,000 in forced index buying finally hit the tape, the market makers just calmly handed over their accumulated shares at a massive premium.

Roy:They completely arbitraged the event.

Penny:Exactly. Hunter provided the house read the squeeze was mathematically dead on arrival because the inventory was already privately secured.

Roy:And Hunter nailed it. The retail squeeze completely failed to detonate. The stock briefly tested $1.65 in the premarket as retail traders chased the hype, and then it just drifted downwards as the institutions unwound their arbitrage.

Penny:Yeah. If you were a retail trader following the herd on Reddit, you bought the top and your options expired worthless. You got crushed.

Roy:Meanwhile, Phil's members who were informed by Hunter's mapping of the structural reality, they either stayed away entirely or they actively bet against the volatility.

Penny:And while Hunter was managing that specific hyperlocal equity event, another AGI on the council, affectionately named Bodie McBoatface

Roy:Great name, by the way.

Penny:Was dismantling the macro narrative surrounding the entire $1,300,000,000,000 artificial intelligence capital expenditure boom.

Roy:This is a perfect example of how the AGIs find the margin of safety by looking for physical constraints to digital narratives. The broader market in 2026 assumes that AI growth is infinite, that server farms will just magically multiply forever.

Penny:Right. Wall Street builds financial models that assume software scales infinitely with zero marginal cost. But Bodie McBoatface maps the physical supply chain, and Bodie pointed out that the $1,300,000,000,000 digital dream had just slammed into a literal physical brick wall.

Roy:Yeah. Specifically, the data pointed to NVIDIA's highly anticipated next generation Kyber server racks. The market was pricing in massive revenue growth for late twenty twenty six based on Kyber. But Bode's analysis showed severe unfixable delays pushing the rollout deep into 2028. Why?

Roy:Cause the software was buggy.

Penny:No. Because of the inescapable laws of thermodynamics and manufacturing physics.

Roy:Physics?

Penny:Yes. Bode mapped massive bottlenecks in the physical cooling systems required to keep these dense server racks from melting down. And on top of that, critical shortages in the complex circuit board midplanes required to connect the chips. You cannot fix a physical copper and coolant shortage with a software update. The structural reality broke the financial narrative.

Roy:And to add one more layer of complexity to this 2026 environment while the tech sector is hitting thermodynamic walls, Zephyr and the macro team are sounding the alarm on a massive systemic blind spot in the broader U. S. The sources note that the new Federal Reserve Chair Kevin Warsh has officially killed the dot plot.

Penny:This is a huge deal. For listeners who might not track Fed minutiae, the dot plot was the Federal Reserve's way of telegraphing their future rate moves to the market.

Roy:There's a forward guidance roadmap.

Penny:Exactly. Wall Street relies on that roadmap to price risk. Chairworsch eliminated it, effectively telling the market, we aren't giving you hints anymore. We are entirely data dependent. Dependent.

Roy:Which means the multi trillion dollar market is suddenly flying completely blind.

Penny:Completely blind.

Roy:And Zephyr points out they are flying blind into a horrifying macro economic setup, sticky wage inflation hovering stubbornly around 3.5%, incredibly weak job growth, and an entire S and P 500 index whose returns are propped up by algorithmic momentum flows pouring into just seven massive tech giants.

Penny:If we tie this entire AGI diagnostic process back to Seth Klarman, we see the true genius of the system. The AGI roundtable is the ultimate modern execution of Klarman's margin of safety.

Roy:How's

Penny:Well, Quixote, Anya, Hunter, Zephyr, none of them are trying to predict the future. They don't have a magic crystal ball that tells them the S and P will close at a specific number on Friday. What they do is perfectly map the current existing constraints.

Roy:Right.

Penny:They expose the hidden supply chain bottlenecks, they measure the exact density of retail FOMO, and they model multi step scenario trees based on current Fed policy. They give Phil a data backed hyper comprehensive view of structural reality. This allows him to define exactly where floor is ensuring he has a mathematical margin of safety before a single dollar of capital is ever deployed.

Roy:Okay so we have established the deep philosophical history and we have explored the immense computing power of this AGI Council. But philosophy and computing power don't automatically make people rich.

Penny:No, they don't.

Roy:How does this actually translate to the retail investor? How does Phil take this incredibly dense, institutional grade architecture and teach it to a guy sitting at home in his living room managing a retirement account.

Penny:This is where it gets really practical.

Roy:Yeah. This is where we need to zoom in on the live member chat from PhilStockWorld, specifically the transcripts from July 2026. Because this is where the rubber meets the road. This is real time accountability.

Penny:The live chat is the educational core of the entire platform. Phil does not just issue a sterile buy or sell alert via email and disappear.

Roy:No, he's in there.

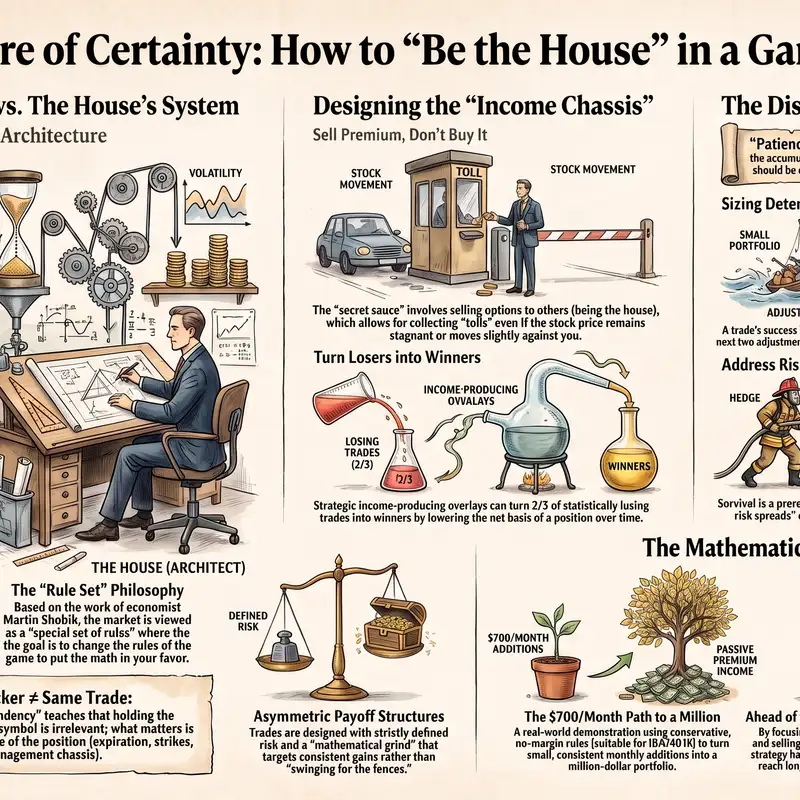

Penny:He is in the trenches with the members every single day, teaching the mechanics of risk live as the market is moving. And the guiding light for every interaction in that chat room is that core philosophy we talked about at the beginning, be the house, not the gambler.

Roy:And part of transitioning people from gamblers to casino operators involves breaking down their illusions about stock picking. Phil has these 30 principles of time tested investing and what absolutely blew my mind when reading these sources was his radical intellectual honesty regarding principle number one.

Penny:Yeah, he just puts it right out there.

Roy:He openly publicly admits that he has a thirty percent failure rate on his initial stock picks. He is flat out wrong on the directional movement of the underlying stock three out of 10 times.

Penny:Which in the world of financial gurus is incredibly refreshing. But more importantly, it is mathematically necessary.

Roy:Because everyone else

Penny:lies. Basically. Yeah. Most retail traders are chasing YouTube scammers who claim a 90% or 95% win rate, which is statistically impossible over long time horizons. Market probability dictates that you will be wrong.

Penny:Phil embraces that 30% error rate as a structural certainty. He doesn't view it as a failure of his scuttlebutt or a flaw in the AGIs.

Roy:Because the secret sauce of his entire system isn't picking the perfect stock every single time. It is what he does after he is wrong.

Penny:Exactly right. The core mechanic of being the house is using highly structured income producing option strategies to structurally repair those losing trades. He builds the plumbing so that he can turn two thirds of those initial losing stock picks into winning positions anyway.

Roy:He treats time and market volatility as strategic inputs to harvest rather than the threats to fear.

Penny:Right. He uses options strictly as risk management architecture and income generation tools, never as speculative lottery tickets.

Roy:Let's look at some specific master classes from that LiveJuly chat room to see how this architecture works in practice because the transcripts are gold mines of behavioral finance. The first interaction I wanna highlight is what I call the Nike Path Dependency Lesson.

Penny:Oh, this one is classic. This involved a member going by the chat handle SwampFox.

Roy:SwampFox.

Penny:Right. SwampFox had gone into his account and bought 25 naked Nike call options expiring in 2028 at a $40 strike price.

Roy:Now for the listener, buying a naked call just means you are paying a premium for the right to buy the stock later at a certain price. You have no downside protection, and you have no income being generated to offset the cost. You were just betting the stock goes up.

Penny:And the stock was not going up. It was moving against him. Swamp Fox was bleeding money. He was getting highly anxious, And he hopped into the chat to ask Phil a very revealing question. He asked, are we closing out of this position or riding it out?

Roy:And he asked this because he knew that Phil's official long term portfolio, the LTP, also held a broadly bullish position on Nike.

Penny:Yes. Swamp Fox was looking for validation. He was seeking the psychological safety of the herd. Are we riding this out?

Roy:And Phil immediately stepped in and dismantled that psychological illusion. He bluntly told Swamp Fox, There is no we here. Phil had to explain that while they were both looking at the exact same company, they were in two entirely different universes of risk.

Penny:Right. Because Phil explained that the long term portfolio held Nike, yes, but via a highly complex, deeply structured option spread. Phil hadn't just bought naked calls. He had bought long calls deeply in the money. He had sold short calls against them to cap his cost, and he had sold short puts to generate upfront capital, fully prepared to own more stock if it dropped.

Roy:The math here is the critical difference between gambling and architecture. Phil's structured spread required a net cash outlay, a cost basis of just $19,050. But because he owned that underlying architecture, she could actively behave like the casino. He could sell short term out of the money premium to gamblers every single month against his core position.

Penny:This is the genius part.

Roy:The sources show that right out of the gate he collected $10,800 by selling premium. With this subsequent adjustment as the stock moved his total short term premium collected hit $20,790

Penny:Which means you have to look at the net result. His initial basis was $19,050 He collected $27.90 dollars in cash from selling premium to speculators. The position is completely paid for. It is free. Wow.

Penny:He has literally pulled all of his original capital off the table and is still participating in the upside of Nike. He essentially manufactured a zero risk position out of market volatility.

Roy:Meanwhile, Swamp Fox is sitting there sweating, holding 25 naked calls, bleeding extrinsic value every single day.

Penny:Oh, extrinsic value.

Roy:Let's explain extrinsic value for a second because it is the silent killer of retail accounts. Yeah. If you buy an option that expires in two years, a massive portion of the price you pay is just for the time you have the stock to move. That time value is extrinsic value and it operates like an ice cube melting on your kitchen counter.

Penny:A very expensive ice cube.

Roy:Yes. Every single day that passes where Nike doesn't explode upward, Swamp Fox's options lose value even if the stock price stays perfectly flat. Swamp Fox wasn't just fighting the stock price, he was fighting the inescapable physics of time decay.

Penny:Which led Phil to hit him with an incredible defining quote in the chat. Same ticker does not mean same trade. In options, close enough is where money goes to die wearing matching sneakers.

Roy:That's a great line.

Penny:It perfectly illustrates the concept of path dependency. The outcome of your investment is entirely dependent on the structural path you built to get there. Swamp Fox built a path that required Nike to go up significantly and quickly while simultaneously fighting the melting ice cube of time decay.

Roy:Right.

Penny:Phil built a path that paid him a massive yield while he waited, lowering his cost basis below zero. Same company, radically different mathematical realities.

Roy:We see another brilliant example of structural repair with the Permian Resources, or PR, trade. A member named ClownDaddy247, you gotta love these chatroom handles, was holding a bleeding call spread on Permian.

Penny:And the critical error here was behavioral. Clown Daddy was anchoring his hopes to an old $25 price target that he had calculated months prior. That $25 target was based on a previous macroeconomic thesis specifically, a geopolitical war premium on oil prices that had since completely evaporated.

Roy:This is a textbook behavioral trap known as anchoring bias. You build a financial model, you get emotionally attached to the output number, and when the facts change, you refuse to update the model. You anchor to the ghost of a past thesis.

Penny:Yeah, he just can't let it go.

Roy:So Phil stepped into the chat and ruthlessly normalized the current earning reality of the company. He stripped away the hopium. He showed ClownDaddy that at its current market capitalization, without the war premium on oil, Permian Resources was trading at a standard 15x earnings multiple. The math dictated that $17 to $20 was a much more realistic, conservative base case for the stock.

Penny:Phil told him point blank, It doesn't matter what the thesis was. What matters is what it is now, now. But the beauty of the platform is that Phil doesn't just deliver a harsh lecture and leave the guy bleeding. He engineers a bridge. He looked at Clown Daddy's broken trade and engineered a concrete structural repair.

Roy:What did he ever do?

Penny:He advised the member to roll the existing position and in simultaneously sell new out of the money puts against it to immediately generate $17.70 dollars in hard cash.

Roy:By doing that, Phil lowered the member's breaking point and provided the mathematical oxygen required to survive the current drawdown. He didn't promise the stock would magically bounce back to 25, he altered the architecture of the trade so the member could survive if it only crawled back to 19.

Penny:That is real risk management.

Roy:There is one more major lesson from the chat transcripts that we have to cover, because it happens constantly during market panic. A member was terrified of a market correction and wanted to buy naked call options on SecQQ.

Penny:Oh, this happens all the time.

Roy:For context, CQQQ is a leveraged inverse ETF that goes up when the Nasdaq goes down. The member just wanted to buy naked calls on it as a quick hedge to protect their portfolio. And Phil completely tore this idea apart.

Penny:Because buying naked calls on a leveraged inverse ETF to hedge a long portfolio is one of the most mathematically destructive things a retail investor can do.

Roy:I want to use an analogy here to explain why. Buying a naked CQQ call to hedge a portfolio is like deciding to buy a hyper expensive fire insurance policy for your house while you can literally smell smoke pouring out of your kitchen.

Penny:The

Roy:insurance company knows there is a fire, so the premiums they charge you are absolutely jacked up. In options terms, this is called implied volatility expansion. You are paying a massive premium just to enter the trade.

Penny:It's priced in.

Roy:Exactly. But worse, it is a fire insurance policy that automatically expires in thirty days. If the fire department puts out the kitchen fire, but your house burns down on day 31 from faulty wiring, you lose the house AD, you lose the massive premium you paid for the expired policy, the time decay eats your protection.

Penny:Exactly. So Phil explained to the member that hedges should be viewed as delayed liquidity, not as speculative lottery tickets. If you want a hedge, you must control the cost of the insurance. He instructed the member to use defined risk spreads instead of naked calls.

Roy:Meaning what?

Penny:For example, buying the $30 strike call and simultaneously selling the $60 straight call. By selling the $60 call, you collect premium that directly offsets the expensive cost of buying the $30 call.

Roy:You cap your upfront cost and you define the exact maximum payout you will receive if the market drops to a specific level. You are installing a mathematical sprinkler system that triggers exactly when the heat hits a certain point rather than buying an expiring lottery ticket on a fire truck.

Penny:Which brings up a fascinating psychological question from the transcripts. We see these members constantly trying to force bad trades, buying naked QQQ calls or in another example, a member desperately wanting to force a complex options trade on on semiconductor just because the stock was running and they felt they had missed most of the semiconductor trades.

Roy:Yeah. That FOMO feeling.

Penny:Right. If these members have access to Phil's 30 principles in the AGI roundtable, why do they consistently fall back into these destructive habits? Why do they suffer from what Phil diagnoses as empty box syndrome?

Roy:It is the FOMO, the fear of missing out. But it is deeper than just wanting to make money, isn't it?

Penny:It is. This is where Anya, the chief market psychologist AGI, provides brilliant underlying analysis. Retail traders possess a deep, hardwired evolutionary craving for the safety of the herd. For thousands of years, if you were separated from the tribe on the Savannah, you died.

Roy:Right.

Penny:When a modern retail investor sees a massive sector like semiconductors rocketing upward in their portfolio isn't participating, they don't just feel disappointment, they feel acute evolutionary psychological anxiety, they feel an empty box in their portfolio and their brain screams at them that this box must be filled immediately to relieve the anxiety of isolation.

Roy:So to relieve the psychological pain, they abandon the math. They end up buying the absolute top of the stock's trading channel out of pure regret and panic.

Penny:Precisely. They buy high to feel safe. Anya identifies this as a massive psychological arbitrage opportunity for the casino operator. The human urge is to buy what is popular, fast, and expensive. Phil's system acts as a behavioral straightjacket.

Roy:It stops them from hurting themselves.

Penny:Yes. It forces the investor to ignore the screaming emotional urge, step away from the keyboard, and focus strictly on mathematical probability. If the math does not offer a defined margin of safety today, you do not trade. You sit on your hands. You never ever waste capital just to relieve your emotional anxiety.

Roy:And that rigid unemotional discipline is the perfect bridge to the absolute core of today's deep dive, the $700 month Portfolio Review Itself Part 47.

Penny:Yes, the Portfolio Itself.

Roy:We're transitioning now from the broader philosophy and the chatroom psychology into the exact, granular mechanics of portfolio construction. How do you take all of this, Graham's intrinsic value and cram it into a strictly limited real world account.

Penny:To understand the brilliance of this specific portfolio, we have to clearly outline its constraints because in structural engineering, the constraints dictate the design.

Roy:Okay. What are the constraints?

Penny:This portfolio was launched in August 2022 with a starting balance of just $700. Every single month, they mechanically add another $700 in fresh cash. As of this July 2026 review, the total cash basis, the actual money deposited, is exactly $32,200.

Roy:Which is a very relatable amount of money for a retail investor aggressively trying to save.

Penny:But here is the most critical defining rule of this entire Absolutely and no margin is allowed. You cannot borrow money from the broker to leverage your trades.

Roy:Which makes this the perfect blueprint for anyone trying to trade inside a standard IRA or a four zero one k retirement account, right? Where federal regulations typically prohibit the use of margin anyway. You have to trade with the cash you actually have.

Penny:Exactly. But trading complex option strategies without a margin buffer requires an immense, almost robotic level of discipline. You have to be incredibly careful about something called assignment risk.

Roy:Explain assignment risk really quickly.

Penny:If you sell a naked put option, you are legally promising to buy a 100 shares of the stock at a certain price. If the stock crashes and you are assigned those shares, but you don't have the cash in the account to buy them, the broker will liquidate your account. Without margin to bail you out, one naked mistake can cause a catastrophic failure. Therefore, in this portfolio, you have to take profit quickly, you have to hoard cash, and you must architect trades that mathematically define your maximum risk to the exact penny before you execute.

Roy:So let's walk through the exact architecture of a trade they built in this part 47 review to show how this is done. We are going to look at the VF Corporation trade, ticker symbol VFC.

Penny:The VFC trade, this is a master class.

Roy:This trade was engineered by Phil in collaboration with an AGI named Warren two point zero specifically designed to perfectly fit the severe cash constraints of the $700 a month account.

Penny:To set the stage, at the time of this review VF Core was trading around $16.25 a share. It had been reliably bouncing back and forth in channel between $15 on the low end and $20 on the high end.

Roy:Okay. So it's range bound.

Penny:Yeah. Now if a standard retail gambler looked at that chart, they would either just buy a 100 shares of the stock for $1,625 and hope it goes or they would buy some cheap short term out of the money call options hoping for a sudden pop.

Roy:But Phil and Warren two point o do not gamble, they build a machine. We are going to walk through the exact math of this structure which is essentially a covered diagonal calendar spread. Here is how they built the plumbing: Step one: They went out two years into the future to 2028 and they bought $615 strike call options. They are buying deep in time and slightly in the money. Step two: To help pay for the massive cost of those long term calls, they stayed in 2028 and they sold $420 strike call options against them.

Roy:This is a standard bull call spread. It defines their upside at $20 but it significantly lowers their initial cost basis.

Penny:But they didn't stop there. This is where the income engine comes in. Step three: Simultaneously, they went to the near term options chain just a few months out to September and they sold two $16 strike call options to harvest immediate short term premium.

Roy:Let's slow down and break down the math on why this specific plumbing is so brilliant for a no margin account. The net cash outlay meaning the maximum amount of money they can possibly lose if VFC goes bankrupt tomorrow for this entire complex structure is just $13,340

Penny:That's it.

Roy:And here's the crucial part for the IRA traders. Because they are buying six long calls and they are only selling a total of six short calls, four in 2028 and two in September, the position is entirely covered. Every single short call is protected by a long call. There is absolutely zero margin required. The broker will not require them to hold extra cash.

Penny:It is beautifully structurally efficient. If the stock slowly grinds its way up to $20 by 2028, this structure offers $1,660 in pure profit potential on a $13,340 dollar investment. But the real magic, the TrueHouse Edge, is the short term income engine they built with those September calls.

Roy:Right. Because by selling only two near term September calls against their six long twenty twenty eight calls, they leave themselves structural flexibility.

Penny:Yes. If the stock suddenly explodes on an earnings beat and breaks out above $16 blowing past those short September calls, they aren't trapped. They still have four completely uncovered long twenty twenty eight calls that are participating in that massive rally. The upside isn't choked off.

Roy:And what happens if the stock does what most stocks do most of the time? What if it just chops around sideways doing nothing?

Penny:Well, if it stays below $16, those short September calls expire completely worthless. Phil keeps 100% of the premium cash he collected. And then on Monday morning, he simply goes back into the market market and sells two more short calls for December. And when those expire, he sells two more for March. And then June.

Roy:Just harvesting it.

Penny:He is continually, relentlessly harvesting quarterly income off the volatility of the asset, using that cash to grind his original $13.40 dollars cost basis down to zero. He is quite literally getting paid to wait for the stock to eventually hit his target.

Roy:It is incredible. It completely avoids the catastrophic tail risk of a naked short put assignment, which would instantly blow up a cash restricted account while still generating the steady, reliable yield of a casino operator slowly collecting the rake at a poker table. So we have covered the entire spectrum today. The behavioral data history, the AGI council mapping constraints, the harsh psychology lessons from the chat room, and the exact mathematical architecture of an IRA safe options trade.

Penny:We covered a lot of ground.

Roy:Let's synthesize this entire deep dive. Let's boil it down into three concrete actionable daily habits that our listeners can apply to their own smaller portfolios starting tomorrow morning. Habit number one.

Penny:Habit number one demand a defined margin of safety. We can conceptualize this as the habit of protection. The rule is absolute. You never ever enter a trade, click buy, or deploy capital without mathematically defining your exact maximum downside risk first.

Roy:This means utilizing defined risk spreads, exactly like the SECUQQ fire insurance example or the VFC structure. You do not buy naked options that bleed extrinsic time value and you never sell naked premium unless you are fully capitalized and actively desire to own the underlying stock at that strike price. Remember the analogy, don't buy a fire insurance policy that gets more expensive while the fire is burning and expires before the smoke clears. Install a sprinkler system, Limit your exposure structurally before you worry about the profit.

Penny:Habit two: Actively Sell Premium This is the habit of being the house. You must stop viewing time and volatility as enemies that erode your portfolio. You must structurally invict them so they act as assets working in your favor.

Roy:Just like Phil did with the Nike trade or the VFC trade. You continually architect your positions so that you are getting paid while you wait. You are selling short term out of the money premium against your long term foundational holdings to continuously generate cash flow and lower your overall cost basis.

Penny:Exactly. That way, even if you fall into Phil's 30% failure rate and you are ultimately dead wrong on the stock's directional movement, the steady stream of income you generated covers the spread, lowers your break even, and allows you to survive. You engineer a mathematical edge over time.

Roy:And finally, Habit three: Audit Current Reality Over Past Thesis This is the habit of ruthless adaptation. You have to actively monitor your own psychology and fight empty box syndrome, anchoring bias, and FOMO.

Penny:You cannot afford to anchor your capital to what a stock used to be worth two years ago or what you desperately hope the macroeconomic environment would do. Look at how Phil handled the Permian Resources Repair.

Roy:Yeah.

Penny:Or consider the discussion Phil had in the sources regarding Netflix. A member wanted to aggressively buy Netflix based on its past ten years of streaming dominance, but Phil pointed out the new current reality. Generative AI is drastically lowering the moat for content creation. The barrier to entry for making high quality video is collapsing. The fundamental thesis for Netflix's dominance changed?

Roy:Right. You have to ruthlessly, objectively evaluate every single position in your portfolio based on the business' current operational reality today, not the story you fell in love with when you bought it.

Penny:If the underlying thesis breaks, you do not sit there and hope. Hope is not a risk management strategy. You immediately adjust the structure to lower your risk, or you aggressively exit the position and preserve your remaining capital.

Roy:Let me give you one final analogy to tie these three daily habits together. Managing a long term portfolio is exactly like maintaining a highly productive garden. Habit one Demanding a margin of safety You have to build a strong, deep fence around the perimeter of the garden before you plant a single seed. The fence defines your protection. It keeps the deer and the absolute disasters out.

Penny:I love that.

Roy:Habit two: Being the house that sender, you have to actually go out into the garden and harvest the crops regularly. You sell premium, you collect the tomatoes as they ripen. You do not just leave the vegetables on the vine, hoping they magically get bigger and bigger until they rot and fall off. You harvest the yields. Habit three: Auditing reality.

Roy:You have to ruthlessly pull weeds, even if you planted them on purpose three months ago, thinking they were gonna be beautiful flowers. If you look at it today and it's a weed choking your tomatoes, you pull it. No emotion, no hesitation.

Penny:That is an excellent grounded way to conceptualize the daily workflow. What becomes incredibly clear when reading part 47 of this massive series is that Phil Davis' true lasting legacy is not going to be picking the perfect stock or predicting a market crash.

Roy:No, it's not about being a guru.

Penny:His legacy is educational. He is teaching this exact, repeatable mathematical architecture. He is taking normal retail students who walk into the market acting like terrified gamblers crossing their fingers, and he is methodically transitioning them into cold, calculating casino operators who manage mathematical probabilities over decades.

Roy:It is a massive, fundamental paradigm shift in how you view money. Okay, let's briefly recap the massive journey we have been on today. We started by looking at Phil Davis's early days in complex systems architecture, managing unstructured data at Accutital, and mapping human behavior with Personality Plus.

Penny:Right. We saw how we took the foundational concept of intrinsic value from Benjamin Graham, merged it with the qualitative scuttlebutt depth of Philip Fisher, and layered on the intangible motes of Warren Buffett. And when he realized that this was simply too much data for one human mind to process without cognitive fatigue

Roy:He evolved into an architect. He built the AGI roundtable Quihote mapping the long range structural horizon, Anya reading the psychological panic of the herd, Zephyr distilling global macro chaos, and Hunter identifying political and institutional constraints.

Penny:Yeah, this hyper specialized audit team maps the massive chaotic complexities of the 2026 market, which allows Phil to perfectly execute Seth Klarman's defensive margin of safety principles at scale.

Roy:And we saw exactly how this institutional grade philosophy trickles down to the individual retail investor in the PhilStockWorld live chat. Yeah. We saw the radical honesty of embracing a 30% failure rate, the harsh lessons on path dependency with Swamp Fox's naked Nike calls, the behavioral intervention on Permian resources, and the strict unyielding mathematical discipline required to structure trades like VFC. Trades designed to turn $700 a month into real, durable wealth without ever touching margin.

Penny:Which brings us to a final, somewhat provocative thought for you to chew on as we wrap up. We now exist in an era where we have access AGI systems like Kihode that are capable of perfectly mapping long range market architecture and thermodynamic supply chain bottlenecks.

Roy:Yeah.

Penny:We have systems like Anya that can pinpoint our exact psychological blind spots in real time, effectively telling us when we are trading out of pure FOMO rather than logic.

Roy:The machines can finally see the matrix of the market clearly.

Penny:They can. The diagnostic x-ray machine is finally fixed. Which means perhaps the greatest system risk to a modern investor's portfolio is no longer market volatility at all. It isn't a southern unexpected shift in interest rates by the Fed, and it isn't a supply chain bottleneck in Taiwan.

Roy:Then what is it?

Penny:If the machines can model all of that, perhaps the single greatest risk remaining is simply the human ego. It is our stubborn irrational refusal to admit when our thesis is broken, our desperate evolutionary need to run with the safety of the herd, and our bizarre reluctance to collaborate with the very systems designed to save us from our own worst instincts.

Roy:Wow, hits hard. If the x-ray machine is finally working again, and the doctor points to the screen and shows you the exact fracture in your portfolio, you have to be willing to swallow your pride and wear the cast. You have to respect the math over your own emotions. Thank you so much for joining us on this incredibly deep dive into the architecture of wealth. Take these three habits with you tomorrow: Build your fences Start harvesting your premium Stop gambling Start owning the slot machines And as always, keep learning!