Hardware Bottlenecks Shatter Deceptive Market Highs

You know, usually when you look out of the ocean on a, a really beautiful summer day, there's this profound expectation of tranquility.

Penny:Oh, absolutely. It just looks perfect.

Roy:Right. You see the flat shimmering blue surface, know, the gentle lap of the waves against the boat, you just point and say, look how peaceful it is. Yeah. But then if you were to put on a pair of sonar headphones and drop a microphone beneath that surface, that tranquility is completely shattered.

Penny:You hear the reality.

Roy:Exactly. What you actually hear is like grinding metal

Penny:Yeah.

Roy:The chaotic swirl of currents and predators hunting in the dark.

Penny:It's a completely different world down there.

Roy:It is. You realize that beneath that glassy surface, you are looking at an environment that is honestly a war zone. And that submarine war is exactly what is happening in the financial markets today, Monday, 07/06/2026. So welcome to Deep Dive.

Penny:Yeah. The surface of the market today is, I mean, it's the absolute definition of deceptive calm. If you look at the mainstream financial the narrative is entirely triumphant.

Roy:So let's look at that surface for a second, right? The major market indexes are printing record highs. We just saw the Dow close above 53,000 for the first time in history.

Penny:Which is a massive psychological number. Huge.

Roy:And the Nasdaq rallied another 1.24%. So for the casual observer, yeah, the tourist trader who is currently extending their fourth of July holiday weekend and sipping a margarita on the beach somewhere, the market just looks completely unstoppable.

Penny:Right. But the volume tells a completely different story.

Roy:Yeah.

Penny:And that is the first major red flag in the structural plumbing today. The volume is completely dead.

Roy:Like, how dead are we talking?

Penny:We are talking about barely 200,000,000 shares turning over on the SPY, which, that's the ETF that tracks the S and P 500.

Roy:Wow. Barely 200,000,000. So if the market is hitting all time highs, but literally nobody is actually trading, what is driving the price up? I mean, are these just phantom numbers?

Penny:Well, yeah. Essentially, when volume evaporates like this, the price action you see on your screen becomes an illusion. It is no longer driven by, you know, human conviction or actual institutional capital allocation. Instead, it's just driven by automated flows, algorithmic rebalancing, and passive indexing.

Roy:So the machines are just trading with each

Penny:other? Exactly. The machines are trading with each other in a vacuum. So to cut through that noise, we have to look at the raw macroeconomic data completely objectively and just strip away all that bullish sentiment.

Roy:Right.

Penny:And when we run today's data through our macro logical frameworks, specifically the scorecards we use from the AGA roundtable to measure market efficiency, massive structural warnings are just flashing red.

Roy:So I want to dig into those warnings because the first metric jumping out of the PhilStockWorld Morning Report is a number that seems almost too big to comprehend.

Penny:The liquidity drain.

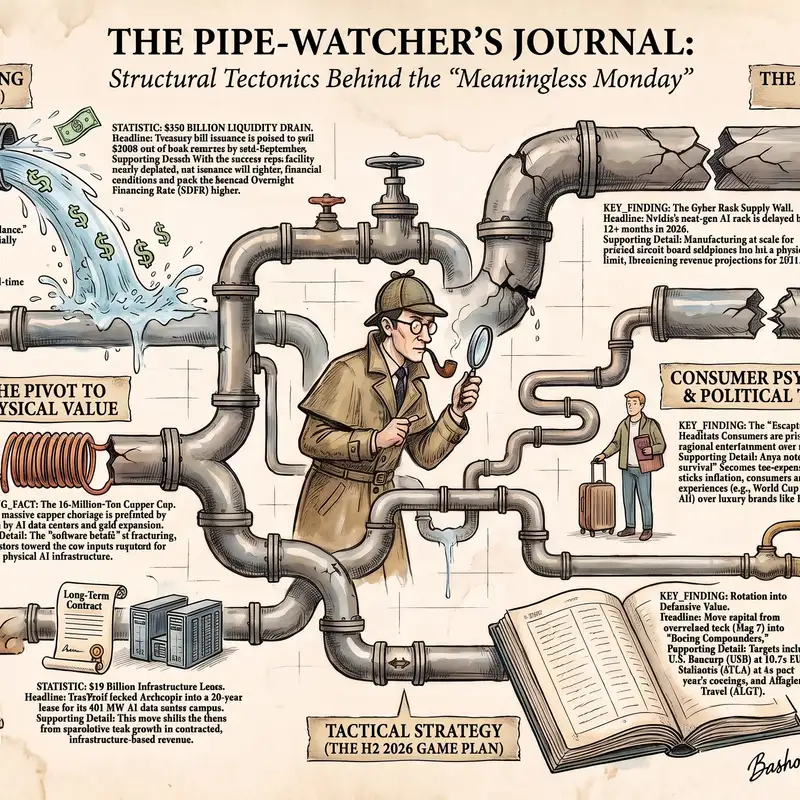

Roy:Yeah. A $350,000,000,000 liquidity drain hitting the markets by mid September. How does a third of $1,000,000,000,000 just, you know, vanish from the financial system?

Penny:It comes down to the mechanical plumbing between the Federal Reserve, the Treasury Department, the commercial banking sector. For the last couple of years, the financial markets have been really cushioned by something called the reverse repo facility.

Roy:Okay stop right there because I hear that term thrown around constantly on financial networks but it's rarely ever explained. Mhmm. What is the Reverse Repo Facility in just plain English?

Penny:Sure. Think of it as a massive, high yield savings account operated by the Federal Reserve, specifically for money market funds and large financial institutions.

Roy:A giant savings account. Got it.

Penny:Right. When these institutions have way too much cash and nowhere safe to put it, they park it overnight at the Fed. The Fed takes their cash, give them treasury securities as collateral, and pays them interest. Okay. So it acts like a giant sponge just soaking up excess liquidity from the system.

Roy:So sponge is full of cash. But you're saying right now the sponge is currently drying out?

Penny:Rapidly. The balances in that reverse repo facility have just plummeted. The excess cash is nearly gone. And this is colliding with a massive problem at the Treasury Department. The US government is running a massive fiscal deficit, meaning they are spending far more than they take in through taxes.

Roy:Which is not exactly a secret at this point.

Penny:No, not at all. But to fund that gap, the Treasury has to issue a tidal wave of new debt in the form of Treasury bills.

Roy:Let me make sure I understand the mechanics here, for my own sanity and for you listening at home. If the treasury is issuing hundreds of billions in new debt, someone has to buy it. Correct. Previously, the money market funds would just take the cash out of the Fed's reverse repo sponge, right, and use it to buy those treasury bills. It was kind of a closed loop.

Roy:It didn't really affect the broader economy.

Penny:You nailed it. But because the sponge is now empty, that closed loop is totally broken.

Roy:Oh, man.

Penny:Yeah. The buyers of this new government debt have to find the cash somewhere else, and that somewhere else is commercial bank reserves.

Roy:Meaning capital is gonna be pulled directly out of the banking system to absorb this new government debt.

Penny:Exactly. And when supply of available cash shrinks, the cost of borrowing it spikes.

Roy:Right. Basic supply and demand.

Penny:We monitor a rate called the SOFR, the Secured Overnight Financing Rate. It's essentially the cost of borrowing cash overnight using treasuries as collateral.

Roy:Okay.

Penny:As this 350,000,000,000 gets vacuumed out of bank reserves over the next two months, we expect short term borrowing costs to rise, which rapidly tightens financial conditions for risk assets.

Roy:So the cheap leverage that fuels all this speculative trading is literally being drained out of the room.

Penny:Very quickly. Yes.

Roy:So we had this massive liquidity vacuum forming beneath the surface, but surely the federal reserve is stepping in to manage this right, Which I guess brings up the second major shift in the data today from Zephyr's scorecard: Interest rates and Fed policy.

Penny:Yeah, this is huge.

Roy:We have a new Fed chair, Kevin Warsh, and he just made a policy announcement at the European Central Bank Forum and Sintra that fundamentally changes how Wall Street operates.

Penny:He officially killed the dot plot and he ended forward guidance.

Roy:For the listener who might be prepping for a meeting or just trying to manage their own portfolio, why is the death of the dot plot such a seismic event?

Penny:Historically, the dot plot was the ultimate security blanket for the stock market. Every single quarter, the Fed would publish a chart where every regional Fed president and governor placed a literal dot on a graph.

Roy:Right, predicting where rates would go.

Penny:Exactly, predicting exactly where they thought interest rates would be one year, two years, and three years into the future.

Roy:It was essentially the teacher handing the students the answer key to the final exam before the semester even started.

Penny:That's a great way to put it. Traders could place highly leveraged, risky bets because they felt the Fed was holding their hand, essentially promising them that rate cuts were coming down the road.

Roy:But Warsh's philosophy is entirely different now.

Penny:Completely different. His exact words in Sintra were no forward guidance.

Roy:Wow.

Penny:He wants to force the market to price in risk based on real time economic data, not on promises from central bankers. The Fed is no longer gonna hold Wall Street's hand.

Roy:And flying blind like that is terrifying when you look at the actual data printing this morning. I mean, the ten year treasury yield, is the benchmark for global borrowing costs and mortgages, is sitting stubbornly high at 4.47%. Yeah. But at the exact same time, The US economy just printed a disastrously weak non farm payrolls report for June. We added a mere 57,000 jobs.

Penny:It was a huge miss.

Roy:Yet wage inflation remains incredibly sticky, growing at 3.5% year over year. So we have weak growth colliding with high costs. That's stagflation.

Penny:It is the absolute worst case scenario for an equity market currently priced for perfection.

Roy:Because under the previous Fed regime, if job growth plummeted to 57,000, the market would actually rally. Right? Assuming the Fed would panic and immediately cut interest rates to save the economy.

Penny:Right. The classic bad news is good news dynamic.

Roy:Precisely.

Penny:But under Warsh, with no forward guidance and a strict mandate to crush that sticky 3.5% wage inflation, rate cuts are highly unlikely. In fact, if inflation persists, rate hikes are theoretically still on the table. So capital is getting permanently more expensive, and the broader market has not adjusted its valuations to reflect that new reality.

Roy:Okay. Let me push back on this for a second. If liquidity is draining out of bank reserves to the tune of $350,000,000,000 and the Federal Reserve has taken away the forward guidance security blanket while we slide into stagflation.

Penny:How

Roy:on earth is the Dow Jones Industrial Average breaking 53,000 today? It feels like driving a runaway train on a track that ends in a brick wall in about a mile.

Penny:It looks completely contradictory until you look at the third metric on our macro scorecard, which is extreme market concentration. The indexes aren't climbing because the broader economy is healthy. They are climbing because they're hiding behind a handful of giants. Let's look at the math for the S and P 500.

Roy:Let's do it.

Penny:The entire index is projected to generate $2,350,000,000,000 in net after tax earnings this year.

Roy:Which sounds like a massive healthy number.

Penny:It does, until you realize that 845,000,000,000 of that total is projected to be earned by just seven companies. The magnificent seven tech giants.

Roy:Just seven companies?

Penny:Just seven. They are averaging over $100,000,000,000 in earnings apiece.

Roy:So seven companies out of 500 are carrying more than a third of the entire profitability of The US corporate sector. That's insane.

Penny:And if you expand that lens to the top 50 companies, they generate almost 66 of their earnings. Wow. This means the bottom four fifty companies in the S and P 500 are essentially just ignored by the passive index funds. The algorithmic flows are blindly buying the index, which disproportionately funnels capital into those top seven tech names.

Roy:Creating a self fulfilling feedback loop of valuation expansion, which makes the entire system incredibly fragile. Wall Street analysts are aggressively projecting that the S and P 500 will hit 8 thousand by 2027 based on the assumption that these seven companies will just continue to compound their earnings flawlessly.

Penny:That's the narrative.

Roy:But if this runaway train is being pulled entirely by the AI engine of these tech giants, what happens if that engine runs out of physical fuel?

Penny:And that is the pivotal question of this entire market cycle. When we ask Sherlock to take today's market movements and audit them for logical consistency, we uncover a massive glaring contradiction in the AI narrative.

Roy:So let's lay out the observable facts here. The major tech companies are currently engaged in an arms race, spending roughly $1,300,000,000,000 in capital expenditures to build out AI infrastructure.

Penny:Unprecedented amounts of money?

Roy:Right. They are buying graphics processing units, GPUs, they are building hyperscale data centers, and they are doing this to chase future software earnings that currently require the market to assign them a 30 times valuation multiple just to justify.

Penny:They are deploying historic amounts of capital based on the fundamental assumption that digital expansion is frictionless.

Roy:Infinite and frictionless.

Penny:Yeah. The market is pricing these companies as if writing better software code automatically translates to limitless revenue.

Roy:But software needs hardware. I mean, expansion is entirely dependent on physical manufacturing. And physical manufacturing just hit a massive brick wall. Because I'm looking at the reports out of the supply chain today regarding NVIDIA's next generation hardware.

Penny:The Kyber delay. This is a structural fracture in the AI timeline.

Roy:Let's unpack this for the listener who might just think of NVIDIA as a stock that, you know, always goes up. Nvidia doesn't just sell individual computer ships anymore. They sell massive integrated data center systems.

Penny:Right.

Roy:Their absolute cutting edge next generation product is a server rack called Kyber. It's designed to house their upcoming twenty twenty seven Rubin Ultra chips. We are talking about packing 144 of the most powerful AI processors on the planet into a single cohesive unit. It is the pinnacle of computing power.

Penny:It really is. And the entire tech industry's revenue projections for 2026 and 2027 are deeply reliant on that Kyber architecture being delivered on time so they can train their generation AI models.

Roy:But the supply chain reports today confirm that Kyber has been delayed by more than twelve months.

Penny:Right.

Roy:It is being pushed to 2028.

Penny:And a full year delay in the tech world is an eternity.

Roy:Why is it delayed? I mean, is it a software bug?

Penny:No. It's actually problem of basic physics and physical manufacturing. Specifically, it involves the printed circuit board midplanes.

Roy:Okay. What is a midplane and why is it causing a trillion dollar bottleneck?

Penny:Well, when you try to connect a 144 hyper advanced GPUs in a single rack, you can't just run traditional copper wires between them.

Roy:Okay.

Penny:The sheer volume of data bandwidth and the immense electrical current require a massive, highly specialized printed circuit board known as a midplane to connect everything seamlessly. Furthermore, the thermal output, the sheer heat generated by packing that much computing power into a small physical space is astronomical.

Roy:Because chips draw power and power creates heat.

Penny:Exactly. And the manufacturing precision required to build these midplanes so they can handle the data bandwidth without physically warping or literally melting under the thermal load is proving to be incredibly difficult to achieve at scale. Innovation has essentially outpaced manufacturing reality. The physics of cooling and power distribution have become the ultimate limiting factor.

Roy:So let me use an analogy here just to ground this. Imagine I secure a million dollars in venture capital to build a state of the art automated bakery because I have customers lined up around the block demanding my bread. My investors are expecting me to double my revenue next year. But then, my supplier calls and says, the high-tech ovens I ordered are melting during testing and won't be delivered until 2028. How does the math work?

Roy:These tech giants are spending $1,300,000,000,000 on the ovens of the AI revolution, but the supply chain just told them the ovens are delayed. How do they justify a 30 times earnings multiple if they physically cannot deploy the infrastructure required to generate those earnings?

Penny:Logically, through SHERLOC's lens, they can't. The market is operating on a fundamental logical flaw, assuming that the transition from a design on an engineer's whiteboard to physical deployment in a data center is just instantaneous.

Roy:Right.

Penny:You cannot simply manifest computing power out of thin air.

Roy:And the real danger isn't just that a few tech stocks might see their share prices drop. The US government is quietly waking up to the systemic risk this poses.

Penny:The treasury report.

Roy:Yeah. The treasury department just released a draft report warning that an AI bubble bursting today could be vastly more devastating than the dot com crash of two thousand.

Penny:We really have to look at the blast radius here. In 1999, if a speculative.com company selling, you know, pet toys went bankrupt, the damage was largely confined to equity investors who took a bad risk.

Roy:Right. It was isolated.

Penny:The broader plumbing of The US economy wasn't deeply affected, but today. The Treasury report outlines how deeply embedded these AI investments are in the core infrastructure of the nation.

Roy:Because it's not just software startups anymore. It's the cloud providers that run the Internet, the public utilities that are scrambling to provide the mass amounts of electricity these data centers require, and the private credit markets that are financing the construction of these facilities.

Penny:Yes. If the AI capital expenditure cycle fractures because of this 2028 hardware bottleneck, the contagion won't just hit tech portfolios.

Roy:It spreads.

Penny:It will spread into the credit markets that lent the money for the data centers and the utility markets that banked on the energy demand. The interconnectedness is what makes the delay of a circuit board midplane an actual macroeconomic event.

Roy:This collision between a digital dream and physical reality is so fascinating because it perfectly explains the massive behavioral disconnect we are tracking today between retail investors and institutional insiders.

Penny:If we

Roy:use Cyrano to deconstruct the narrative the market is telling itself versus the observable actions of the smart money, it is a tale of two completely different realities.

Penny:The psychological arbitrage here is just stunning. If you look at the retail expectation, what everyday investors are discussing on forums and social media, they are entirely focused on digital momentum. They are looking at the hype surrounding AI software and chatbots, and they're blindly throwing margin debt at the Philadelphia Semiconductor Index.

Roy:Which is incredibly dangerous considering that index is currently trading at a fifteen year valuation peak. Retail investors are buying the software hype, essentially assuming that popularity automatically equals infinite profitability.

Penny:But when you track the capital flows of institutional insiders, the reality is entirely different. The smart money is not chasing software multiples. They are quietly hoarding physical hard assets and locking down manufacturing capacity for the next decade.

Roy:Because they know.

Penny:They realize that in a world of infinite digital demand, physical supply is the ultimate bottleneck.

Roy:Give me an example of this institutional land grab from today's tape.

Penny:Okay. Look at the deal announced by TerraWolf. TerraWolf historically operated as as a Bitcoin mining company, but they are rapidly pivoting their infrastructure to serve the AI sector.

Roy:Swarmoo.

Penny:Today, they announced they just locked Anthropic, which is one of the leading foundational model companies, into a twenty year lease for a massive AI data center campus in Kentucky.

Roy:A twenty year lease in the tech sector? That is unheard of. Technology changes every six months. Why would Anthropic sign a two decade agreement?

Penny:Because Anthropic realizes that the hardest part of the AI race isn't writing the code, it's securing the electricity to run the models. Wow. This single contract is expected to generate $19,000,000,000 in revenue for Terrowolf over its term.

Roy:19,000,000,000.

Penny:Yeah. Terrowolf isn't betting on which AI chatbot wins the market. They are literally becoming the toll collector for electricity and the cooling systems required to play the game.

Roy:They are buying the real estate and the power grid. That is brilliant. And we are seeing this exact same panic over physical capacity in the consumer hardware space too. Right? Look at the massive deal Broadcom just announced.

Penny:Broadcom just signed a binding five year agreement to supply Apple with custom ASIC chips stretching all the way through 2031.

Roy:For context, ASIC stands for Application Specific Integrated Circuit. Unlike a general purpose GPU, an ASIC is a chip custom designed for one specific, highly efficient task. But Apple is famous for its ruthless dominance over its supply chain. They historically dictate terms to suppliers on a quarter by quarter basis.

Penny:They bully them.

Roy:Yeah, they do. So why would a giant like Apple lock itself into a rigid five year agreement with Broadcom?

Penny:Because Apple sees the kyber delay at NVIDIA and understands the macroeconomic shift. They know that securing the physical chips and the fabrication plant capacity is now vastly more difficult than actually designing the iPhone.

Roy:Right.

Penny:If Apple doesn't lock down that manufacturing capacity now, someone else will, and they won't have chips for their devices.

Roy:And Apple is already feeling the pain of physical bottlenecks. Ming Chi Ku, one of the most reliable supply chain analysts, reported today that Apple's highly anticipated foldable iPhone is facing severe manufacturing hurdles, pushing its release deep into the fourth quarter of twenty twenty six.

Penny:Exactly. So while retail investors are fighting over hyper expensive tickets to concert, the institutions are quietly buying the arena. They're buying the power lines that run the amplifiers, and they're buying the concrete to build the parking lot.

Roy:They know the game for the next decade is physical resource capture. And if we pull the lens back even further with hunter mapping systemic risks, we see that this panic to hoard physical assets isn't just happening in the technology sector. It is a systemic shift happening across the entire industrial landscape often masked by corporate theater. If we map the political economic risk today, we see defense monopolies executing the exact same playbook as the tech giants.

Penny:The system always rewards those who consolidate the mechanisms of power. Look at the cash acquisition announced today by Lockheed Martin. They quietly bought a company called Ultramaritime for $3,450,000,000 in cash.

Roy:Ultramaritime is not exactly a household name. Why is Lockheed dropping $3,500,000,000 in cash on them?

Penny:Because Ultramaritime specializes in global anti submarine warfare and highly advanced sonar technologies. Alright. While the financial media is completely distracted by the Nasdaq hitting new highs, defense contractors are hoarding the real world physical tools required to project sovereign power. Power. They are consolidating captive markets where the government is the guaranteed buyer, ensuring steady inflation proof cash flow regardless of what happens to the consumer economy.

Roy:Speaking of the consumer economy, let's talk about the everyday person who is actually funding all of this. Because the extraction machine isn't just targeting government defense contracts, it is directly squeezing the middle class. The data surrounding the energy markets today exposes a terrifying trend, the Exdort Valve Tax.

Penny:This is a critical mechanic behind the sticky inflation we discussed earlier. If you look at the price of raw crude oil today, it's relatively cheap, drifting around $68 a barrel.

Roy:Right. Historically, 68 crude means cheap gasoline at the pump for the American driver.

Penny:But if you drive down the street right now gas is incredibly expensive. Where is the disconnect?

Roy:The disconnect is found in the gasoline crack spread.

Penny:Yes.

Roy:The crack spread is the profit margin that oil refiners make when they take raw crude oil and process it into usable products like gasoline or diesel. Right now that refining margin has blown out to an astonishing $54 a barrel.

Penny:Wait, how can the refiners justify charging a $54 premium to turn $68 oil into gasoline?

Roy:Because they have fundamentally altered the plumbing of the energy market. US refiners are currently exporting nearly one third of all the refined fuel they produce to the global spot market. They are putting it on ships and selling it to Europe, Asia, and Latin America.

Penny:So the domestic driver, you and me, commuting to work, we are no longer just paying the local cost of production. We are forced into a bidding war with the rest of the planet.

Roy:Exactly. You are paying global export parity prices for gasoline refined right in your own backyard. And to tighten the squeeze even further, The U. S. Refining industry is aggressively dismantling its own domestic capacity.

Penny:Right. We are seeing major facility closures from companies like Landell, Bassell and Phillips sixty six.

Roy:Let me get this straight. They are shrinking the supply of refineries domestically while simultaneously exporting a third of the product globally.

Penny:Which turns the American driver into a captive audience with literally no alternatives. It is a permanent structural inflation tax engineered entirely through supply chain manipulation.

Roy:It is a master class in systemic extraction. And while the industrial sector is squeezing the consumer physically, the financial sector is executing some truly breathtaking corporate theater in Washington today.

Penny:Oh, RJO had a field day with this.

Roy:Now whenever a policy rolls out of Washington it is incredibly easy to get caught up in partisan cheering or outrage. But if we strip all the politics away, you know we don't care about the red or the blue here, we only follow the mechanical flow of the money. The incentives behind today's major policy announcement are quite revealing.

Penny:Extremely revealing. The administration just rolled out a new initiative called Trump accounts.

Roy:Right.

Penny:These are tax advantaged investment vehicles specifically designed for children, and the president literally rang the opening bell at the New York Stock Exchange from the Oval Office this morning to celebrate it. On the surface, if you read the press release, it sounds like a phenomenal initiative to help family build generational wealth.

Roy:But when you run the front page test with Robojohn Oliver and map the actual mechanics of the legislation, you have to ask, who gains the most and who pays for it? This policy is essentially a legally sanctioned mechanism to route billions of dollars of taxpayer subsidized capital directly into the pockets of legacy ETF managers.

Penny:You are talking about the massive asset management firms like BlackRock or Vanguard?

Roy:Precisely. By creating a tax incentivized mandate for parents to push money into these accounts, the government is creating an automatic, massive recurring bid for the mutual funds and ETFs managed by the largest financial institutions in the world.

Penny:It is beautifully orchestrated corporate theater.

Roy:It really is. It's packaged as populist wealth building for the working class, but structurally, it enriches the oligarchy layer of asset managers who collect the management fees on those billions of dollars year after year.

Penny:The house always wins. Always. And speaking of financial theatre, the traditional equity markets don't have a monopoly on absurdity today. You have to talk about the comedy unfolding in the cryptocurrency space with Michael Saylor's company Strategy Inc.

Roy:Oh man, Strategy Inc is famous globally for its massive Bitcoin treasury. Their entire corporate identity championed by Saylor is built on laser eyed zealotry and the explicit promise that they will never ever sell their Bitcoin.

Penny:They treat it as pristine, incorruptible digital gold that will inevitably replace the fiat dollar system.

Roy:Right.

Penny:But over the holiday weekend, Strategy Inc filed documents with the SEC revealing they just dumped 3,588 Bitcoin, liquidating roughly $216,000,000.

Roy:Wow. Why the sudden betrayal of their core philosophy?

Penny:They had to sell the Bitcoin to fund dividend payments for their traditional fiat based credit securities.

Roy:Are you serious?

Penny:I am. Strategy Inc issued preferred stock to raise capital, and that preferred stock requires mandatory dividend payments in US dollars.

Roy:I'm sorry, but that is hilarious. That is the equivalent of a militant vegan influencer getting caught on camera eating a bacon cheeseburger because they secretly needed the animal protein to finish their workout video.

Penny:It's exactly like that.

Roy:The ultimate Diamond Hands cartel is frantically liquidating the decentralized future of money just to make sure legacy fiat bondholders get their dividend checks today.

Penny:It completely shatters the narrative foundation of their treasury strategy, but it actually gets worse because the financial engineering they use to justify their stock price is also unraveling today. The Wall Street Journal's heard on the Street column published a deep dive exposing the math behind Strategy Inc's proprietary valuation metric, which they call MNAV.

Roy:I've seen them promote MNAV in their earnings presentations. It's supposed to represent their enterprise value as a premium multiple to their actual Bitcoin holdings. How are they calculating it?

Penny:Well, to calculate the true net asset value of a company, the standard formula is to take the market value of the common stock, add the debt and preferred stock, and subtract cash. Right. The critical phrase there is market value, but Strategy Inc. Is using the face value of their debt and preferred stock in the numerator.

Roy:I wanna break this down so it makes absolute sense. What is the difference between face value and market value in this specific context?

Penny:Let's say a company issues a bond with a face value of a $100. That is the amount they promise to pay back at maturity.

Roy:Okay.

Penny:But if the market loses faith in the company, investors might sell those bonds and the actual price to buy that bond on the open market, its market value might drop to $70.

Roy:Okay. I follow.

Penny:Strategy Inc's common stock, their corporate debt, and their preferred stock have all plummeted in market value recently. But when they calculate their MNAV metric to present to investors, they are still plugging in the original $100 face value of that debt, not the $70 market reality.

Roy:Why would they do that? I mean, what does inflating that number actually accomplish?

Penny:By artificially inflating the numerator using face value, they make their enterprise value look significantly higher than it actually is. This masks the reality that the broader market is currently valuing the company at a massive discount relative to the Bitcoin they hold. It is a mathematical sleight of hand designed to make the company look stronger and more valuable to retail investors who don't read the footnotes.

Roy:So if we synthesize everything we've covered so far, tech giants are hitting physical manufacturing walls, defense contractors are hoarding sonar capabilities, refiners are squeezing the middle class with an export tax, asset managers are capturing taxpayer funds through ETF policies, and crypto billionaires are using deceptive math to pay fiat dividends while dumping their core asset. When the systemic game is rigged this heavily toward extraction, it inevitably creates a massive psychological breaking point for the everyday investor.

Penny:And that is exactly what we are seeing in the behavioral data today, when Anya maps the emotional state of the market, the psychology is just fracturing.

Roy:I saw Michael Burry, the investor famous for the big short against the housing market, posting on X today. He quoted the Joker, calling the entire AI narrative a mass addiction and predicting it will die a slow death by a thousand cuts.

Penny:Because the carbon based consumer, the actual human being at the end of the supply chain is completely exhausted. Outline the structural inflation in gasoline, add to that the deeply sticky inflation in housing, insurance, and groceries, and it's hitting consumer tech as well.

Roy:Right. Apple is quietly jacking up the base prices of their iPads just to cover the soaring wholesale inflation of the memory chips required to build them.

Penny:Exactly. The basic cost of physical existence is climbing rapidly, yet retail investors are somehow still scrounging up margin debt to blindly buy semiconductor stocks at fifteen year valuation highs.

Roy:It is a complete detachment from reality. And if we look at how consumers are behaving with whatever discretionary income they have left, Anya points out an emotional arbitrage taking place.

Penny:The prevailing emotion has shifted from greed to preservation and more specifically to escapism. Yes. When human beings are financially tapped out when buying a house is mathematically impossible and financing a new car carries a suffocating interest rate, they don't just stop spending entirely.

Roy:Right.

Penny:They shift their remaining capital away from durable goods and toward temporary experiences. They want a psychological escape from the financial pressure cooker.

Roy:Which perfectly explains the massive upward revision in guidance from Allegiant Travel, ticker ALGT.

Penny:Exactly. Allegiant operates value priced regional airlines catering directly to leisure demand. They fly people from smaller cities to vacation destinations like Vegas or Florida.

Roy:Makes sense.

Penny:They massively raised their earnings guidance because the American consumer is desperate for a cheap vacation, and crucially, the cost of jet fuel has moderated for the airline. They are capturing the last gas of of consumer spending in the experienced economy.

Roy:But while consumers are escaping to the beach, there is another vice sector that is completely collapsing in the market today. Let's talk about the psychological mispricing in alcohol stocks.

Penny:Historically, retail investors have treated alcohol companies like Constellation Brands, ticker STZ, and Diageo, ticker DEO, as recession proof premium growth staples.

Roy:Right. The logic was always simple. In good times, people drink to celebrate. In bad times, people drink to cope. People will always drink.

Penny:That sounds perfectly logical.

Roy:Right. So why is the market punishing them?

Penny:Because the institutional investors are looking at the underlying data and realizing that alcohol is no longer a growth staple. It is undergoing a structural decline. The smart money is compressing their valuation multiples down to the low teens, essentially pricing them like legacy tobacco stocks.

Roy:So what changed? Why are people drinking less?

Penny:It is the Ozempic effect.

Roy:Oh, wow.

Penny:The explosive rise of GLP one weight loss drugs is fundamentally rewiring consumer behavior. These drugs reduce cravings across the board, not just for food, but for alcohol.

Roy:That's fascinating.

Penny:Combined with a generational shift toward health and wellness among younger demographics, the sheer volume of alcohol consumption is steadily dropping.

Roy:So demand is shrinking. But these are massive global corporations. Can't they just raise prices to maintain profit margins?

Penny:Not anymore because they are facing severe margin pressure from looming tariffs. Constellation Brands, for example, relies heavily on importing Mexican beer brands like Modelo.

Roy:Right.

Penny:The incoming tariff policies threaten to shatter their cost structure. And here is the fatal flaw the retail investors are ignoring, the debt.

Roy:How bad is the debt?

Penny:Constellation is carrying over $10,000,000,000 in debt against roughly 2,000,000,000 in annual earnings. In an environment where interest rates are high and the Fed is not cutting, which we established earlier refinancing, that debt becomes incredibly expensive.

Roy:So retail investors are buying these stocks, expecting them to be growth engines, but they are actually buying low multiple value traps saddled with massive debt and declining consumer demand.

Penny:Unless you are buying them strictly for the dividend yield and treating them them like a slow burn utility stock, they are a terrible place to deploy capital right now.

Roy:It's an environment that feels increasingly dystopian. And if you want peak dystopia, we ask Rowan to narrate the psychological disconnect happening in the digital world today. The narrative surrounding Reddit is genuinely mind bending.

Penny:While human beings are stressing out over the physical cost of groceries, gasoline, and keeping the lights on, the digital internet is currently fighting an entirely automated civil war.

Roy:Break down what is happening on Reddit today because this sounds like science fiction.

Penny:Reddit operates one of the largest text based forums on the Internet. Right now, their platform is being flooded by automated bots. But these aren't traditional spam bots. Human marketing firms are deploying highly advanced AI algorithms to generate and post stealth spam across thousands of Reddit communities.

Roy:And what is truly bizarre is that they aren't even trying to advertise to human readers.

Penny:No. They are writing this stealth spam specifically to manipulate other artificial intelligence. Large language models, like OpenAI's, ChatGPT, or Google's Gemini, constantly scrape Reddit to train their models and pull real time answers for users. These AI marketing bots are polluting Reddit with fake organic reviews in an attempt to trick the AI search engines into recommending their specific products to users in the future. It is called data poisoning.

Roy:Okay. So AI bots are invading Reddit to brainwash other AI models. How is Reddit responding?

Penny:By deploying their own counter AI models. Reddit's engineering team is using advanced machine learning specifically designed to hunt down and terminate the AI spam bots. The internal data shows they are currently catching and deleting 25,000 fake AI generated posts every single day.

Roy:It's an araboros of garbage. We have humans paying tech companies for AI to write fake spam, which is uploaded to a platform to train other AI only to be hunted down and blocked by Reddit's internal AI. Algorithms are literally fighting each other in a closed loop for control of training data.

Penny:And the software companies funding this automated war are burning through billions of dollars of real capital sustain it. It perfectly highlights the profound disconnect we are mapping today.

Roy:Right.

Penny:Wall Street is assigning multi trillion dollar valuations to companies building an internet that is actively eating itself alive with synthetic spam, while the physical economy that actually sustains human life is constrained by copper shortages and inflation.

Roy:Okay, let's take a breath and synthesize everything we've uncovered. Because this is heavy. The digital world is fracturing into a synthetic bot war. The high beta tech giants are physically constrained by hardware supply chains that are delayed until 2028. A $350,000,000,000 liquidity vacuum is draining out of bank reserves.

Roy:The Federal Reserve has abandoned forward guidance, inflation is structurally sticky, and the human consumer is financially exhausted.

Penny:That's the landscape.

Roy:So if you are an investor listening to this, you are looking at your portfolio and asking, yeah, how do I survive this? How do we stress test our assets for the second half of twenty twenty six?

Penny:To survive a regime shift of this magnitude, we ask Bodie McBoatface to run a strict stress test against the worst case scenario. We use our modeling architecture to build a clean, actionable decision map.

Roy:So what is the scenario we are stress testing against?

Penny:The derailment of the runaway train. What happens to your portfolio if tech multiples suddenly collapse under the weight of that $350,000,000,000 liquidity drain, colliding with the reality that Nvidia's Kyber racks won't arrive to generate revenue until 2028.

Roy:If that tech bubble pops, the passive indexing flows reverse and the S and P 500 plunges. What is the fix? Where do we hide?

Penny:You don't hide. You pivot. You pivot entirely away from digital momentum and into deep value combined with growth. Specifically, we filter the market for companies operating in the physical world with a price to earnings ratio well under 20.

Roy:You insulate yourself from the blast radius of a tech crash by investing in the part of the market that the passive index funds are currently ignoring.

Penny:Exactly. You look at the bottom four fifty companies of the S and P 500. They only account for fraction of the index's total earnings, but crucially, they carry none of the ridiculous 30 times or 40 times valuation multiples. Their downside risk is already priced in.

Roy:Let's get specific. Let's look at the targets that pass this strict filter today. Target number one, Stellantis, ticker s t l a.

Penny:Stellantis is one of the largest global automakers owning brands like Jeep, Ram, and Dodge. If you look at their balance sheet projections, they are modeled to generate roughly 4,000,000,000 in sheer profit next year.

Roy:Okay.

Penny:Yet the current market capitalization, the price to buy the entire company on the stock market today is sitting at just $16,500,000,000

Roy:Let's do that math. A company making $4,000,000,000 in profit is only valued at $16,500,000,000 That is a price to earnings ratio of roughly four. Why is it so absurdly cheap? Are investors terrified that legacy automakers are going to be bankrupted by the transition to electric vehicles?

Penny:Yes. The market is overwhelmingly obsessed with the digital momentum of pure play EV tech companies, so they heavily discount legacy physical manufacturers. They view Stellantis as an outdated dinosaur.

Roy:Right.

Penny:But when the macro liquidity drains and speculative tech multiples crash, that $4,000,000,000 in actual tangible cash flow provides a massive margin of safety. You are buying a global manufacturing powerhouse for the valuation of a mid sized software startup.

Roy:Okay. Target number two is the ultimate physical asset in a time of crisis. Barrick Gold, ticker b.

Penny:If the Fed is flying blind with no forward guidance and inflation remains structurally sticky due to factors like the export valve tax, sovereign central banks around the world will continue hoarding gold to protect their reserves.

Roy:Makes sense.

Penny:This systemic buying has created a massive reinforced floor for gold prices, currently modeled around $4,154 an ounce.

Roy:And Barrick Gold is the premier operator to capitalize on that floor.

Penny:Barrick is sitting on roughly 85,000,000 ounces of proven physical gold reserves in the ground. Based on current commodity pricing, they are projected to generate $8,000,000,000 in earnings next year. And you can buy the entire company right now for a valuation of around $65,000,000,000

Roy:That equates to an eight times earnings multiple. You are paying eight times earnings for a company sitting on a literal mountain of the world's oldest safe haven asset while people are paying 35 times earnings for AI companies that can't even get their servers built.

Penny:Which leads directly to our third target. If we know that the AI hardware space is bottlenecked and we know that building data centers and expanding the public utility grid requires massive physical infrastructure. What is the raw input required for all of it?

Roy:Copper. Everything runs on copper wiring.

Penny:And the macroeconomic projections show a terrifying physical bottleneck approaching. Analysts project a massive 10 to 16,000,000 ton shortage of copper by the year 2040.

Roy:Wow.

Penny:There simply are not enough active mines on the planet to supply the copper required to build the data centers and the electric grid upgrades that the tech companies are modeling.

Roy:So how do you play that shortage?

Penny:You capture physical exposure through the miners themselves. The Global X Copper Miners ETF, ticker CUPX, or the Sprott Copper Miners ETF, ticker CUPP, provide a diversified basket of the companies pulling the metal out of the earth. Let the tech giants burn capital fighting over delayed silicon chips. You own the copper wire that is mandatory to connect them.

Roy:I love that. It's like walking past a flashy, incredibly overpriced casino that might go bankrupt and instead buying the heavily discounted utility company that holds the monopoly on providing their electricity. They can't play the game without you.

Penny:Exactly.

Roy:And that brings us to the final target in the stress test. Yeah. Greenbrier Companies, ticker GBX.

Penny:Greenbrier designs, manufactures, manages railroad freight cars. They are the definition of physical, unglamorous plumbing for North American industrial logistics.

Roy:Why do they make the cut over a sexier logistics or delivery company?

Penny:Because of their utilization rates. Greenbrier currently boasts a 99% fleet utilization rate.

Roy:99%.

Penny:Yeah. That means, essentially, every single physical asset they own is currently deployed, moving goods, and actively generating cash flow. And despite operating at maximum efficiency, the stock trades at just 11 to 12 times forward earnings.

Roy:The thesis here is incredibly clear. You do not need to take on the massive risk of chasing Nvidia at 35 times theoretical future cash flows. Praying that the supply chain fixes the 2028 Kyberak delays, you can deploy your capital right now into foundational cash generating operators trading at four to 12 times earnings. Your downside is protected by tangible assets trains, gold, copper assembly lines and they pay you dividends while you wait.

Penny:It is a deliberate, calculated portfolio pivot from digital hope to physical reality.

Roy:Alright, so we have the Macro Theory, and we know what broad assets we want to target. But theory doesn't make money unless you know how to execute it when the opening bell rings. We need Jubile's tactical playbook. What are the three high impact moves for tomorrow morning?

Penny:The focus here is clarity over theater. We have three specific prioritized tactical moves based on today's data flows and options mechanics. Move number one, the USB catalyst trade.

Roy:USB is US Bancorp, one of the major regional banks.

Penny:Yes. US Bancorp perfectly fits our defensive filter for deep value combined with growth, but crucially it has an immediate short term catalyst. The analyst firm Jefferies just upgraded US Bancorp to a buy rating today.

Roy:Okay, an analyst upgrade is nice but we don't trade just because someone wrote a positive memo. Let's look at the underlying mechanics. USB is currently trading at 10.7 times its projected $20.27 earnings per share. That keeps it safely under our 20 times valuation threshold. But why buy USB specifically rather than a broad regional banking ETF?

Penny:Because of the operational leverage inside the bank, US Bancorp has achieved a massive 300 basis point improvement in their operating leverage.

Roy:Let's translate that. A basis point is one hundredth of a percentage point. So 300 basis point improvement means they widen their margin by a full 3%. That is a massive leap in efficiency for a bank of that size. How do they do it?

Penny:It is driven by a phenomenal 17% return on tangible common equity or ROTCE.

Roy:Another key metric. ROTCE basically measures how efficiently a bank generates profit from the physical, tangible money its shareholders have invested, stripping out fuzzy math like goodwill or brand value. 17% is incredibly strong.

Penny:It is elite. And they have major revenue tailwinds forming. They recently integrated their massive BTI acquisition, and they just signed a highly lucrative long term partnership with Amazon.

Roy:Oh, wow.

Penny:The tactical edge here is timing. While the broader market has been obsessively chasing the tech names higher, US Bancorp's stock price has barely moved in the pre market. You have a window tomorrow morning to step in and establish a position before the smart institutional money fully rotates out of tech and into these high yield defensive financials.

Roy:Move number two is actually a warning. We need to talk about sidestepping sovereign risk in the shipping sector, specifically with Zim Integrated Shipping. Zim dropped 7% in the pre market today. What caused the plunge?

Penny:Up until this morning, financial models across Wall Street had been aggressively pricing in a high probability of a corporate merger between Zim and the German shipping giant Hapag Lloyd.

Roy:Right.

Penny:The models loved the trade because the corporate synergies combining fleets, reducing overhead, optimizing global routes made perfect mathematical sense.

Roy:So what broke the models?

Penny:Geopolitics. Israeli Prime Minister Benjamin Netanyahu publicly stated today that a merger involving Zim is not on the agenda, throwing the entire deal into deep regulatory and political doubt.

Roy:The lesson here is profound. Financial spreadsheets are fantastic at calculating corporate synergy and profit margins. But they chronically underprice sovereign and political risk. When the head of state steps in and says a deal involves national security or sovereign interests, your discounted cash flow model is irrelevant.

Penny:Exactly, when the state intervenes, you step away. The tactical move is to completely avoid the stock until the sovereign risk clears. Do not try to catch the falling knife based on a spreadsheet.

Roy:Which brings us to tactical move number three. And this isn't just a stock pick, it is an absolute masterclass in options mechanics from the PhilStockWorld community regarding Nike ticker NKE.

Penny:This might be the most important mechanical lesson of the week. Inside the live member chat room today, a member named Swamp Fox posted his portfolio, asking if he should close out his long term options position on Nike or try to ride out the recent volatility.

Roy:And what made this fascinating is that SwampFox's trade looked remarkably similar on the surface to a position held in the PhilStockWorld Long Term Portfolio, or LTP. They were both holding options contracts that expire in 2028. But when the community tore the trades apart and compared them, the difference in risk and execution was staggering.

Penny:The overarching lesson is same ticker does not equal same trade. Let's break down the mathematical edge. Swamp Fox executed what is essentially a bull call spread. He bought 25 long call options expiring in 2028, and to offset the cost, he 20 higher strike call options also expiring in 2028. He also sold some near term puts and calls to generate a little premium.

Roy:And when you net out all the money he spent versus the money he collected, his total net cost for the position was $12,845.

Penny:Now let's look at the LTP position. The LTP bought 50 long calls, sold 40 short calls, and aggressively sold 15 short puts. They built a massive multi legged structure also expiring in 2028. The net cost for this vastly larger position was $19,050

Roy:I see the first major difference: Basis and Scaling. The LTP controlled twice the upside leveraged 50 long contracts compared to 25, but it only cost them marginally more capital because they were far more aggressive in structuring the short puts to finance the trade.

Penny:That is the first edge, but the second edge is the killer, and it comes down to active management and path dependency. Swamp Fox essentially built his twenty twenty eight structure, paid his $12,845, and sat back waiting for Nike stock price to stage a heroic recovery.

Roy:He treated it like a lottery ticket. He bought it and waited.

Penny:But the LTP treated the position like a commercial real estate property. They didn't just wait for 2028. They actively and relentlessly sold short term premium against their core long term basis.

Roy:Let's explain that for the listener. Because the LTP owns those long twenty twenty eight calls, they have the right to sell shorter term options like options expiring in thirty or sixty days without taking on naked risk. It's similar to a covered call strategy.

Penny:They systematically sold near term calls and puts, allowing them to expire worthless or buying them back cheap. In the fund cycle, they collected $10,800 in sheer cash premium. Then, as those expired, they rolled the positions and sold another batch of short term contracts, collecting an additional $9,990.

Roy:If you add that up, they collected $20,790 in cash from selling short term premium against a 2028 structure that originally cost them 19,050.

Penny:The position is literally free. They have extracted more cash from the market than they put into the trade. Their net basis is essentially less than zero.

Roy:That is incredible. Swamp Fox was sitting there bleeding capital, praying for the stock to go up while the LTP made the asset pay for itself while it traded sideways. Think of it this way, if two people own the exact same pair of limited edition Nike sneakers, but one guy paid $100 for them and the other guy got them for free because he charged people a rental fee just to look at the shoebox, Well, they aren't playing the same game. You have to make the asset pay rent while it disappoints you.

Penny:It highlights the brutal reality of path dependency in options trading. In the options market, the concept of we does not exist. You cannot say we are in the Nike trade unless your strike prices, your expiration dates, your contract ratios, your entry basis, and your margin requirements are identical, you are in completely different universes of risk. Copying a ticker symbol from a chat room is easy. Copying the mathematical edge and the discipline to manage the premium is the hard part.

Roy:It truly is a masterclass in treating the market like a mechanical system rather than a casino. Okay, we have covered an immense amount of ground today. We started by looking beneath the surface of the record high Dow Jones and exposed a $350,000,000,000 liquidity drain quietly vacuuming cash out of the banking sector as the reverse repo facility runs dry.

Penny:We tracked the collision between digital momentum and physical reality, mapping out how the massive $1,300,000,000,000 AI expenditure boom is slamming into the physical brick wall of NVIDIA's 2028 Kyber manufacturing delays.

Roy:We watched institutional capital panic and hoard real world assets, locking down twenty year data center leases and five year chip supply chains. We navigated the systemic trap squeezing the consumer from the defense monopolies to the gasoline export valve tax, and we stripped away the politics to expose the corporate theater of the ETF protection racket.

Penny:We laughed at the absurdity of Strategy Inc, liquidating their pristine Bitcoin to pay fiat dividends while using deceptive MNAV math, and we tracked the dystopian reality of Reddit's automated bot war.

Roy:And finally, we laid out a concrete actionable playbook to survive the second half of twenty twenty six. Pivoting away from the tech blast radius and rotating into deep value physical assets like Stellantis, Barrick Gold, and Greenbrier while treating our options portfolios like cash generating rental properties.

Penny:It is about protecting your capital by understanding the structural constraints of the physical world.

Roy:But before we sign off, I want to leave you with one final lingering thought. A question that builds on the ultimate contradiction we uncovered today. We know, based on the supply chain data, that the timeline for deploying next generation AI hardware is stretching out to 2028. The physical ships and the mid plane cooling racks are severely delayed. Yet right now, today, the software companies are burning through billions of dollars in capital to fight automated Ouroboros bot wars on platforms like Reddit just to secure training data.

Roy:So ask yourself, what happens to the multi trillion dollar valuations of these software giants if their financial runway runs out before the physical chips even arrive?

Penny:If you are betting blindly on the software, you are betting against the clock of physical reality.

Roy:Tomorrow morning, when you look out at the ocean and see the indexes floating at record highs, remember that the calm surface is a lie. The real game and the real money is made by understanding the submarine war raging underneath. Thank you for taking this deep dive with us. Being well informed isn't just about reading the headlines, it's about understanding the complex plumbing that dictates them. We will see you next time!