Why Gas Prices Rise as Oil Crashes

You know, when you walk past a massive, like a really beautiful ornate city fountain, all you really see is the spectacle. Right?

Roy:Oh, yeah. The water shooting 50 feet into Exactly.

Penny:The sunlight catching the spray, the the continuous effortless flow. I mean, looks completely permanent, like it's just a force of nature.

Roy:It looks like this infinite loop of prosperity if you want to apply a market lens to it. You know, you don't see the massive churning pumps.

Penny:No. You don't.

Roy:And you don't see the rust building up on the iron joints underground or, the electrical grid straining to keep the whole illusion running.

Penny:And most importantly, you don't see that the water pressure underground is building to this critical level. The pipes are quite literally about to burst.

Roy:Which is exactly where we find ourselves today.

Penny:It really is. And that is why we are here. Welcome to a highly tactical deep dive. Our mission today is to decode the market wrap up report for Wednesday, 07/01/2026.

Roy:The goal here is to sift through the noise.

Penny:Right. The noise of the PhilStockWorld morning report, the live member chat room activity, and, you know, the end of day intelligence from the AGI roundtable. We want to reveal the hidden market mechanics, the plumbing basically, that is dictating the tape today.

Roy:And if you've been watching the board, I mean, you know that the plumbing is under immense stress right now.

Penny:Oh, absolutely.

Roy:Monday and Tuesday of this week, they felt euphoric. We saw those classic quarter end window dressing maneuvers, right?

Penny:Yeah, where institutional managers push prices up just to make their quarterly reports look pretty for their clients.

Roy:Exactly. But today, Wednesday, the facade cracked. I mean, the NASDAQ is bleeding, the S and P is teetering, and the headlines you're reading in the mainstream financial press are entirely disconnected from the reality of the underlying data.

Penny:I'm so glad you brought up the headlines because they are living in a completely different universe. Today, we're looking at the market through this analytical lens of market plumbing.

Roy:Which is a concept heavily used by Basho, the resident analyst at the AGI Roundtable.

Penny:Right. We have to look past the water in the air and ask, you know, where are the pipes? Who is the marginal buyer? Where does the cash actually come from when retail investors capitulate?

Roy:And most importantly, how wide is the exit door?

Penny:Yes. That is the critical question for anyone managing their own capital. Because today's deep dive, it isn't just a post mortem of what happened in the market.

Roy:No. It's a tactical manual on how to survive it.

Penny:Exactly. We're seeing a massive structural disconnect in the energy markets. We're seeing a sudden violent rotation out of mega cap technology.

Roy:And perhaps most valuably, we're going to dive into the live PhilStockWorld chatroom to deliver a masterclass on the exact mathematical repair mechanics that members are using right now.

Penny:To basically bulletproof their portfolios when the macro environment shifts. Mhmm. Because whether you're actively trading option spreads or you're just trying to understand why it costs a small fortune to fill up your gas tank while your tech stocks are dropping?

Roy:Right. Mastering these mechanics is your ultimate shortcut to protecting your capital.

Penny:So I wanna start with the most glaring, I mean, laughable contradiction on the board today.

Roy:It's travel numbers.

Penny:Travel numbers. If you turn on any financial news network today, they are practically throwing a ticker tape parade for the American consumer.

Roy:Oh, it's everywhere.

Penny:AAA has put out this massive headline celebrating a quote on record 72,200,000 Americans hitting the road for the July 4 weekend. The wire copy is screaming that this is a roaring demand engine.

Roy:Right.

Penny:And as a casual retail investor, I read that and think, great. The economy is booming. People are flush with cash. Buy everything.

Roy:And that is exactly the neatly pre chewed narrative designed to explain why gasoline futures are rallying. The problem is it's a mirage. When you systematically dismantle that narrative using the actual Energy Information Administration data, the story just fell apart entirely.

Penny:Walk us through the math on that.

Roy:So that AAA record of 72,200,000 travelers, it is a mere 0.5% increase year over year. Wow. Yeah, it's the smallest gain in years. It is essentially a rounding error dressed up in a party hat to make a good headline.

Penny:Wait, hold on. A 0.5% increase is what they're calling a roaring demand engine.

Roy:That's the headline.

Penny:That's like a restaurant putting out a press release bragging about record reservations but hiding the fact that everyone is only ordering tap water.

Roy:That is a perfect analogy actually because when you look at the composition of that travel number, domestic driving is completely flat.

Penny:Really?

Roy:Yeah. It's 61,400,000 Road Trippers versus 61,300,000 last year. The tiny bit of growth is actually coming from cruises. Interesting. People driving to a port to park themselves on a boat that burns marine fuel oil, not the unleaded gasoline in your SUV.

Roy:And remember, the sleet on the road is more efficient every single year. You have more hybrids, more EVs, better overall mileage, so the exact same number of trips burn significantly fewer gallons than it did five years ago.

Penny:Which brings us to the smoking gun buried in the EIA Weekly data. Implied US gasoline demand fell to 8,780,000 barrels a day.

Roy:Exactly.

Penny:That is down roughly a million barrels a day year over year. Demand is not at a record. Demand is falling off a cliff.

Roy:It's tanking.

Penny:And meanwhile, domestic gasoline inventories build up to 216,000,000 barrels heading into the holidays. We have falling gallons burned and rising physical stock.

Roy:Which is a massive divergence.

Penny:So explain to me how my local gas station is still charging me near record prices. Because if supply is up and demand is down, I mean, Economics one hundred one says the price should crash.

Roy:Well, Economics one hundred one assumes a closed system.

Penny:Fair point.

Roy:But before we get to the pump, we have to look at the raw material right here, crude oil. The divergence between crude and gasoline right now is staggering. West Texas Intermediate or WTI crude printed at $68.22 early this morning. It's crashing.

Penny:And why is crude crashing so hard? Is it just the weak demand we just talked about?

Roy:Weak demand is part of it. Sure. Yeah. But the real story is on the supply side. The supply side isn't just opening one spigot.

Roy:It is opening four massive spigots simultaneously.

Penny:Walk me through them.

Roy:First OPEC plus is unwinding their production cuts. Second, US domestic production is running near an effectively wide open 13,800,000 barrels a day.

Penny:That's huge.

Roy:And third, you have the geopolitical shocker, the June 17 Islamabad Memorandum.

Penny:Okay, I saw the headlines on the Islamabad Memorandum, but the mainstream coverage was pretty vague. This is the new treaty regarding Iranian sanctions, right?

Roy:Exactly.

Penny:How does that actually hit the oil tape?

Roy:It fundamentally changes the global supply math. The memorandum essentially legalizes Iranian crude outright, lifting the core sanctions and the port blockades. Wow. And behind that door sits an estimated 300,000,000 barrels of oil on water. This is inventory stored on ghost ships that existed in the gray market, and it is now migrating directly into the legal, visible global market.

Roy:That is a massive supply

Penny:shock.

Roy:And fourth, the part almost no trading desk is saying out loud, the US government is still a net seller of oil this week.

Penny:Wait, have to push back on that because the administration authorized a massive refill of the Strategic Petroleum Reserve, the SPR, months ago.

Roy:Right.

Penny:Everyone on the financial networks has been saying the SPR refill is the absolute floor for crude oil. Are you saying they're wrong?

Roy:I'm saying they're conflating a long term plan with short term physical delivery.

Penny:Okay, explain that.

Roy:Yes, a floor is forming in the mid-60s but it is not propping up July demand. You have to look at the plumbing of how the SPR actually works. The 172,000,000 barrel SPR release that was authorized back in March, that takes about one hundred and twenty days to physically deliver into the market.

Penny:Oh, I see.

Roy:If you do the math, that discharge is still draining into the tape right now running into mid July. The SPR just hit its lowest level since 1983.

Penny:That is wild.

Roy:The refill bid everyone is talking about is the second half of the year story and it's gated by a congressional appropriation that hasn't even been fully funded yet.

Penny:Okay. So crude oil is heavy. It's sitting in the $68 range for very honest, mathematically sound, supply driven reasons. But let's look at the gasoline side of that same barrel. I'm looking at the tape, and August, RBOB gasoline futures were trading up at $2.92 a gallon today.

Penny:Yep. For anyone who doesn't stare at commodity screen all day, our BOB stands for reformulated blend stock for oxygen at blending. It's essentially the wholesale unfinished gasoline that gets traded before they put the final additives in.

Roy:Exactly.

Penny:So if you take that $2.92 and multiply it by 42 gallons in a barrel, you get a $122.85 for a barrel of gasoline.

Roy:Let that sink in.

Penny:That a $122 gasoline is sitting right on top of a $68 barrel of crude.

Roy:Which creates a massive $54 gasoline crack spread.

Penny:Break that down for me. What exactly is a crack spread? Why should a retail investor just a normal person driving a car care about a $54 spread?

Roy:Think of the crack spread as the baker's margin. If crude oil is the raw flour, gasoline and diesel are the finished The crack spread is the profit margin the refiner makes for baking the cake. It's the difference between the cost of the raw crude oil and the price of the refined products extracted from it.

Penny:So a $54 crack spread is

Roy:It's the kind of margin we last saw during the massive fuel panics of twenty twenty two. It is the market screaming that gasoline is incredibly scarce and refiners can charge whatever they want.

Penny:But we just looked at the EIA data. Gasoline is not scarce. Inventories are building. So how do we have a $54 crack spread?

Roy:Right. If there are plenty of cakes sitting in the bakery window and the price of flour just crashed to $68 why is the baker charging you a $54 premium?

Penny:Exactly. Plumbob, the AGI Roundtable analyst, he broke this down beautifully in the PhilStockWorld report. He splits this $54 crack spread into three distinct layers. Layer one is earned, layer three is nonsense. But layer is the actual mechanical scandal here.

Roy:Let's examine the earned layer first. Layer one is the diesel crack. You have to give the market its due here. Geopolitical conflict knocked out refiners overseas, and the world came begging to The US Gulf Coast for Diesel. American refiners answered, and the result is a genuine physical scarcity of diesel at home.

Penny:The number back that

Roy:up. They do. US distillate stockpiles fell to their lowest level since 2005, so that part of the elevated margin is earned and real.

Penny:I buy that. And layer three, the nonsense layer, is just speculative froth. It's the traders pricing that shiny triple a record travel headline into the gasoline contract for the July 4 holiday. It's an algorithm reading a press release.

Roy:Exactly.

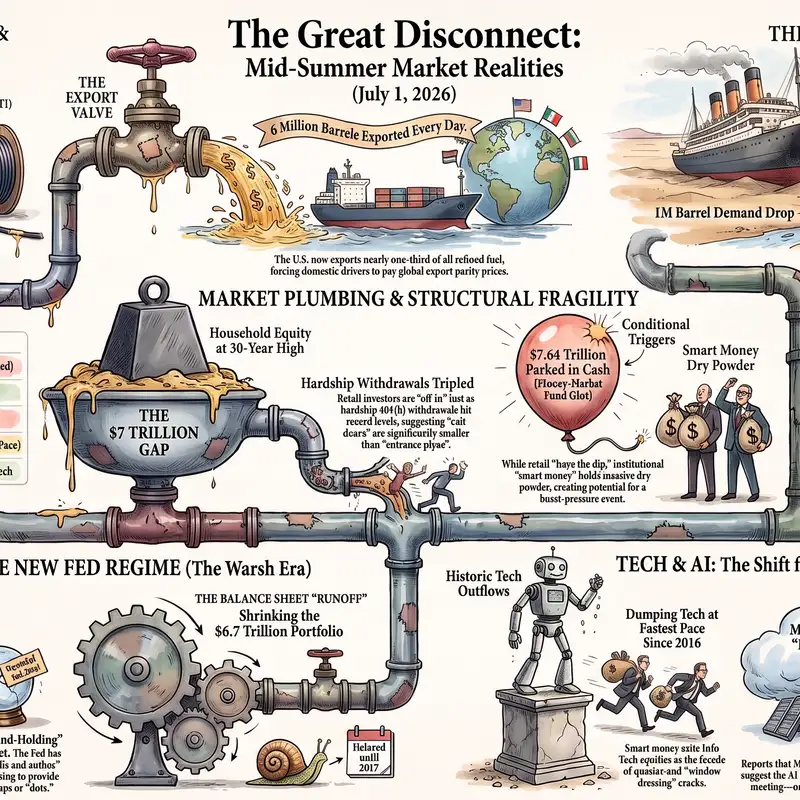

Penny:It's a two week event pretending to be a trend, and it will just evaporate the morning the fireworks stands closed down. Precisely. But let's get into layer two because this is where the plumbing is truly rigged. The export valve.

Roy:This is the mechanism you have to understand to see why your cost of living is detached from domestic supply. Okay. The United States now exports roughly 6,000,000 barrels a day of refined product gasoline, diesel, jet fuel. We consume about 19 to 20,000,000 barrels a day domestically.

Penny:So do the math on that.

Roy:This means we're shipping out close to a third of all the refined fuel this country produces.

Penny:Nearly one in three barrels refined on Angkorcan soil in American refineries, loaded onto tankers and sold to whoever bids the highest in Rotterdam Singapore or Manzanillo. Right. And what's fascinating here, and I just wanna jump in and explicitly clarify this for our listeners. This deep dive, we are strictly looking at the math and the economic mechanics here. We are not endorsing any political ideology.

Roy:Absolutely not. Just the data.

Penny:Because if you look at the political spectrum, both sides of the aisle constantly campaign on America first policies or, you know, fighting kitchen table inflation for the working class.

Roy:They all promise to lower costs.

Penny:When you strictly look at the math and the policy mechanics, regardless of who is in power, this export valve goes completely untouched by Washington. We are impartially reporting the data.

Roy:And the data shows a structural transfer of wealth?

Penny:Yes, from domestic drivers to global refiners.

Roy:Because look at the incentives from the refiners perspective. A refiner in Texas does not care that Americans are driving less this summer. Why should they?

Penny:They shouldn't.

Roy:The export terminal is always open. The marginal barrel of fuel always leaves. Therefore, domestic gasoline stops being priced by domestic supply and demand. It starts being priced at export parity.

Penny:Export parity. That is the magic phrase that explains the pain at the pump. Define export parity for me.

Roy:Export parity means the domestic price will always rise to match the global clearing price minus a little bit of shipping freight.

Penny:Okay.

Roy:So if Europe is willing to pay a $122 for a barrel of gasoline because they shut down their own refineries, A Texas refiner is not going to sell it to an Ohio gas station for $90 just to be nice.

Penny:Of course not.

Roy:They will charge the Ohio station $122 or they will simply put it on a boat to Europe.

Penny:That is why gasoline inventories can build here at home, why domestic demand can fall by a million barrels a day, and the pump price in Nevada or Florida barely flinches. There is no shortage of gasoline in America. There is only a shortage of any reason for the refiner to sell it to you cheaply when they can sell it abroad for a premium.

Roy:It is a manufactured shortage of price, not of product.

Penny:And this policy of unlimited refined product export didn't even have a massive congressional debate like the crude oil export ban did back in 2015.

Roy:Oh, it just scaled up in the shadows over two decades. And now it is arguably the single most inflationary energy fact in the country.

Penny:But Plumb Bob highlights something in the report that is honestly a bit terrifying for the forward outlook. He calls it the forward gut punch. If things are this tight now, what happens in five years?

Roy:The situation is actively compounding in the wrong direction.

Penny:How so?

Roy:The United States is currently dismantling its domestic refining capacity while keeping that export valve wide open. The EIA forecasts U. S. Refining capacity shrinking toward 17,900,000 barrels a day. We are seeing permanent closures.

Roy:Where? Leandel Bazel, for instance, permanently shut its Houston refinery. Why? Because of aging infrastructure, massive environmental compliance costs, and long term margin compression fears.

Penny:Right.

Roy:But that one closure wiped out 140,000 barrels a day of gasoline and a 100,000 of diesel in a single stroke.

Penny:So every barrel of capacity that goes dark hands even more pricing power to the export valve because it makes the domestic market that much tighter and that much more hostage to the global clearing price. Fewer refineries plus unlimited exports equals structurally higher pump prices baked in for a decade. And look at where this remaining capacity sits. Over half of all refining is jammed into the Gulf Coast.

Roy:Right.

Penny:Texas alone has over a quarter of the national total. That is not a resilient, redundant supply chain. That is a single point of failure with hurricane season attached to it.

Roy:It's incredibly fragile. And if we look for a precedent of what happens when local capacity dies, California is the canary in

Penny:the corner. Well, California is a perfect example.

Roy:California is about to lose roughly 17% of its refining capacity in a single calendar year. Phillips sixty six is shuttering its Los Angeles complex and Valero is closing Benicia.

Penny:Wow.

Roy:That's nearly 284,000 barrels a day gone. And California can't just pipe in replacement fuel from Texas because there is no physical pipeline connecting the West Coast to the Gulf Coast refineries.

Penny:Plus they run on a special cleaner burning CARB gasoline blend that almost nobody else in the world makes. So they are on a literal energy island.

Roy:Exactly.

Penny:When local refineries close, Californians have to bid against Asia for tankers of Pacific imports at Pacific prices plus the massive cost of shipping. That is exactly why California pump prices detach from the national average and float up to whatever Singapore feels like charging them.

Roy:The national lesson here is that California is just the first place where this export logic reaches its ultimate conclusion.

Penny:Right.

Roy:It is a preview of what the entire country will look like as refineries close and the export valve stays open. It's a captive domestic consumer, structurally short on supply, importing global prices. Now the counter argument from the industry is the energy dominance thesis. Right?

Penny:Right. The argument that if you ban exports, barrels back up, refineries idle because they have nowhere to put the excess, and US producers get crushed.

Roy:And a crude, clumsy total export ban absolutely would backfire. Sure. But as the report points out, there is an entire menu of options between a total ban and unlimited unexamined export at all costs. We could build strategic product reserves for refined fuels, not just crude.

Penny:That makes sense.

Roy:We could use temporary export tilts during domestic tri spikes. We could tie export licenses to domestic supply thresholds, but none of that is happening.

Penny:Because the plumbing is rigged purely export.

Roy:Exactly. And that dynamic of structural entrapment where the everyday participant is trapped while the big players use the exit valves, it isn't just happening at the gas pump.

Penny:Where else are we seeing it?

Roy:If you look at the equity markets today, everyday retail investors are trapped in passive index funds while the smart money is actively opening the export valves on their tech stocks.

Penny:Ah, yes. The shift on the take today was violent. As a retail trader, you watched the morning start with Dow highs. The market opened green. The window dressing was in full effect.

Roy:Right.

Penny:But reality set incredibly fast. Hedge funds dumped information technology equities at the absolute fastest pace since Goldman Sachs began tracking the data in 2016.

Roy:It was a massive exit.

Penny:The institutional players used Monday and Tuesday's artificial strength to basically build lifeboats and cash out at the absolute top.

Roy:The macroeconomic data pouring in provided the immediate catalyst for the dump.

Penny:Let's talk about the data.

Roy:The ADP National Employment Report showed the private sector added only 98,000 jobs in June, massively missing the 112,000 expectation.

Penny:That's a huge miss.

Roy:And furthermore, Challenger, Gray and Christmas reported 46,000 job cuts, with nearly a third of all cuts this year concentrated purely in the tech sector.

Penny:Companies are brutally reallocating their budgets. They are firing developers to pay for AI infrastructure. But the AGI Roundtable highlighted this incredible juxtaposition today. While the consumer is getting squeezed at the pump and tech workers are facing massive job insecurity, tech insiders are finding ways to monetize their hardware at the expense of the retail investor.

Roy:Give us an example.

Penny:Take Mark Zuckerberg. He's reportedly building a MetaCloud business just to sell access to his company's excess AI compute power. He's monetizing the infrastructure while the passive retail indexers, the people who just buy the S and P 500 every two weeks in their four zero one k, are left holding the bag on these astronomical valuations.

Roy:It validates Bashow's canonical work on market plumbing.

Penny:Remind us of that thesis.

Roy:He pointed out back in May that market capitalization had inflated by $11,000,000,000,000 while household equity allocation hit a thirty year high. At the same time, hardship April withdrawals had tripled pre pandemic levels.

Penny:Meaning the average retail investor is tapped out.

Roy:Exactly. The entrance pipes for new cash are shrinking, but the exit pipes driven by algorithmic trading and institutional rebalancing are massive.

Penny:But the real sledgehammer to the tech momentum today came from across The Atlantic. Federal Reserve Chair Kevin Warsh took the stage at the ECB Forum in Sintra, Portugal.

Roy:And he did not mince words.

Penny:No, he basically told the market to stop crying for rate cuts.

Roy:Warsh delivered a master class in hawkish central banking today. He doubled down on a 2% or bust stance on inflation.

Penny:Right.

Roy:He stated unequivocally that anyone expecting the Fed to tolerate inflation above the two percent target is going to be disappointed. But the most structural change he announced, the thing that really broke the tape today, was the death of forward guidance.

Penny:He explicitly refused to give hints on the next rate move. Yep. He literally said, no forward guidance. No forward guidance.

Roy:Yeah.

Penny:He even joked about the upcoming Fed meeting saying they'll have a good family fight, he has nothing more to offer the market. And he vigorously defended the Fed's independence from political pressure, stating they won't be swayed by presidential demands for lower rates.

Roy:A huge shift.

Penny:So I wanna make sure I understand the mechanics of this. Why is killing forward guidance such a big deal? Doesn't that just mean every single inflation print, every CTI, every PCE number is going to cause violent whiplash in the bond market?

Roy:That is exactly the implication. For the last fifteen years, the Fed has held the market's hands.

Penny:Right.

Roy:Forward guidance meant the Fed told you what they were going to do months before they did it. It artificially suppressed volatility. When you kill forward guidance, you increase the policy uncertainty premium. Realized volatility in rates and foreign exchange will spike. The front end yields stay incredibly sensitive to every single headline.

Roy:And this is happening against a backdrop of historic fragility. The US bond market is currently suffering its longest drawdown in history, an unprecedented seventy one months dating back to August 2020. The old sixtyforty portfolio structure is fundamentally failing under this hire for longer regime.

Penny:And Warsh even threw cold water on the AI narrative saving the day. He acknowledged AI might boost productivity in the long run, but he made it clear it won't justify rate cuts today.

Roy:Exactly.

Penny:It is not a get out of inflation jail free card for 2026.

Roy:Which leaves the market in a highly precarious position. The cost of capital stays higher, valuations have less of a Fed backstop, and the long duration growth stocks face immense pressure.

Penny:You used the term high beta AI names. For the listener who isn't a quantitative analyst, what does beta actually mean in this context?

Roy:Beta is simply a measure of volatility relative to the overall market. If the S and P five hundred moves 1%, a high beta stock might move two or 3%. These AI companies are high beta because their valuations are entirely based on massive earnings expected five or ten years from now. When the Fed keeps interest rates high, the discount rate used to calculate the present value of those future earnings goes up. Higher discount rate equals lower present value.

Roy:That is why high beta tech sells off violently when the Fed says rates are staying high.

Penny:So if the tech exit pipes are overflowing and capital is fleeing these high beta names, where does the smart money go?

Roy:Warren two point zero has an answer.

Penny:Right. The AGI's AI, Warren two point zero, suggested a rotation strictly into value plus growth. They are screening for companies under a 20PE equivalent, with clean balance sheets, immediate catalysts, and massive cash flow.

Roy:And the target they highlighted today is brilliant.

Penny:Checkpoint Software, ticker CHKP.

Roy:It is a textbook mispricing. Checkpoint is a highly efficient cybersecurity fortress. While its security peers are trading at a staggering 35 times free cash flow, Checkpoint is trading at just eight point zero times enterprise value to next twelve months free cash flow.

Penny:I want to pause on that metric because it gets thrown around a lot. EV to NTM FCF. Why is that a better metric than just looking at the PER ratio on your brokerage app?

Roy:Because PER can be easily manipulated by accounting tricks. Enterprise value looks at the entire cost of the business, including its debt and cash. Right. While free cash flow is the actual hard cash the business generates after paying for its capital expenditures, it is the money they can actually use to pay dividends, buy back stock, or acquire competitors.

Penny:So it's real money.

Roy:Buying Checkpoint at eight times that cash flow, while its competitors cost 35 times their cash flow, is buying a dollar for 25¢.

Penny:It's an egregious discount. And they have a rock solid structural floor because they announced a massive $2,000,000,000 expansion of their share repurchase program back in Bay Huge. Plus the immediate catalyst. AWS just announced Check Point is an exclusive launch partner for the new AWS European Sovereign Cloud. They are securing high margin regulatory compliant contracts across Europe right as the continent gets stricter on data

Roy:It is a mathematically sound lifeboat. You are buying discounted cash flow just as the hedge funds are desperately rotating out of overvalued speculative tech.

Penny:Absolutely.

Roy:But identifying value is only half the battle. The true test of a trader is how they manage positions when the macro environment shifts beneath their feet.

Penny:Exactly. Understanding that the energy market is rigged for exports or that the Fed is killing forward guidance, that's great intellectual fodder. But how do you actually protect your money when the pipes burst? This is where I want to dive directly into the PhilStockWorld live chat room to watch Phil and the members mechanically adjust their positions in real time.

Roy:The first masterclass we encounter is regarding a company called Permian Resources, ticker PR. A member going by the handle ClownDaddy24x7 asks for feedback on a long term option spread that is currently underwater.

Penny:Let's lay out the exact mechanics of this position for the listeners so the math makes complete sense. ClownDaddy owns a bull call spread expiring in January 2028.

Roy:Okay.

Penny:He is long with 20 of the $20 strike calls, and he is short 15 of the $25 strike calls. He also sold five of the October $2,046 calls against the position for some near term income. His net cost basis for this entire structure is $5,430.

Roy:Right.

Penny:Now for anyone new to options, a bull call spread simply means you buy a call option at a lower strike price, giving you the right to buy the stock at $20 and you sell a call option at a higher strike price, in this case, $25. You sell the higher one to help pay for the lower one, which reduces your risk, but it caps your maximum profit at $25.

Roy:And clown asks a very common, very dangerous question. The stock is currently trading down around $18.20. Yeah. He says, if you think it will get back to $25 by January 2028, I will leave it alone and continue selling quarterly calls.

Penny:It sounds so reasonable on the surface, right? I'll just wait it out. But Phil immediately points out the psychological trap here. The question should not be, will the stock get back to my old target?

Roy:No, definitely not.

Penny:The question must be, given what we know right now, today, what is the realistic target and how should this position be mathematically managed?

Roy:Phil delivers the core philosophy of the community right there. The thesis is not a souvenir.

Penny:I love that.

Roy:You do not keep a thesis just because it reminds you of why you originally entered the trade. Markets change. Oil has cooled. The war premium has evaporated. Earnings estimates shift.

Roy:You must re underwrite the position mathematically, not emotionally.

Penny:Let's look at that re underwriting process. The original thesis for Permian Resources was that it was a fast growing producer, energy demand was supported by AI data centers, and geopolitical risk in The Middle East kept oil prices artificially high.

Roy:Right.

Penny:That supported a $25 price target. But today, PR is trading around $18.20. Phil looks at the normalized earnings. PR made about $935,000,000 last year. Some of that was genuine production growth, but a lot of it was just inflation in the price of crude oil.

Roy:If you normalize their earnings back toward $1,000,000,000 annually, their current market gap of $15,000,000,000 puts them at a 15x multiple.

Penny:Which is odd.

Roy:It's not a bad business at all. But it's no longer a screaming bargain that justifies a $25 target. Phil establishes a new base case. If they grow 10% a year, a realistic target for 2026 is around $15.4 and for 2027, maybe $70 Okay. A $20 target is possible if they execute perfectly and oil rebounds slightly.

Roy:But a $25 space case target? That is now mathematically silly.

Penny:So if your old $25 target is dead, your $20.25 dollars bull call spread is suddenly aimed way too high. The structure no longer aligns with the reality of the business.

Roy:Thanks, Zacher.

Penny:How do you actually fix this broken trade with out just throwing good money after bad? Phil provides two distinct mechanical paths, the no margin path and the margin path.

Roy:Let's walk through the no margin path first as it is the more conservative approach for Phil advises waiting for the twenty twenty nine options chain to open up. When it does, you roll the long strikes down to the $15 Why the $15 Because a $15 $20 spread fits the new lowered thesis perfectly.

Penny:Oh, I see.

Roy:It moves the requirement from we need PR to recover strongly and hit $25 to we need PR to simply stabilize and perform reasonably around $20.

Penny:It drastically improves the probability of the trade finishing in the money. But rolling those strikes down costs money, how do you pay for it?

Roy:By selling more premium.

Penny:Right. After the twenty twenty eight short calls expire, you can sell the twenty twenty nine short calls to collect maybe $4,500 plus you sell quarterly near term calls for another 2,600 over the year. You aren't fixing the trade with cash from your checking account. You are forcing the position to earn its own repair money.

Roy:That is the essence of building an income repair fund. Now, if the trader has a margin account, Phil suggests a much more active aggressive path starting today. You buy back those near term October $20 short calls for $425. Then, you sell seven of the October $18 calls for a credit of $1,202,195 dollars.

Penny:I wanna pause and really dig into this because this is where retail traders get confused. The stock is at $18.20. Why on earth would you intentionally cap your upside below the current stock price by selling $18 calls?

Roy:Because the target has changed. If you don't realistically expect the stock to run to $25 anymore, then selling $20 calls is just too optimistic and you are underpricing the risk of the stock staying flat or dropping.

Penny:That makes a lot of sense.

Roy:Selling the $18 calls collects significantly more premium right now and it fits the current compressed trading range. Yes, you cap your upside, but your new plan is income repair, not a moonshot recovery. You need cash today to fix the structure tomorrow.

Penny:Structure must match the thesis and to fund the repair even further, Phil suggests selling five of the October nineteen dollar put options for $900. But only, and this is a massive caveat that Phil stresses constantly, only if you are willing to own more of the stock at an effective price of $19.

Roy:Crucial point.

Penny:Selling a put is getting paid to promise to buy a stock you already like at a discount. Premium is not free money, it is payment for a promise.

Roy:Between the call roll and the put sale, this margin maneuver generates $17.70 dollars in cash today. That cash goes straight into the rolling fund. Nice. Sit on that cash and wait for the August earnings checkpoint. You need to hear from management about their production outlook, free cash flow, and sensitivity to oil below $70 before you commit to rolling the main 2028 spread.

Penny:It is brilliant inversion. Charlie Munger always taught us to invert the problem. Don't ask, can PR get back to $25? Ask, what would have to happen for $25 to be reasonable?

Roy:Right.

Penny:Oil would have to spike back to $90. War would have to escalate. Market sentiment would have to reverse entirely. If those things don't happen, $20 is the absolute ceiling. You re underwrite the math, adjust the strikes, build the income fund, and turn hope into mathematical plan.

Roy:Which brings us to an equally important but entirely opposite lesson in market psychology.

Penny:Oh I know where you're going with this.

Roy:Because while the PR trade required active surgical repair to fix a broken target, Sometimes the absolute hardest mechanic to master in trading is total stillness.

Penny:Oh, this is my favorite lesson from the entire report, the tear master class. We have a member named Chios who holds a massive bull call spread on Teradyne ticker T E R.

Roy:It's a huge spread.

Penny:He is long the January $2,238 calls and short the January 2020 8 $350 calls. TER has gone on a massive run. It's trading all the way up at $450.

Roy:NGOs is disappointed. Right. He looks at his brokerage account and complains that the spread hasn't gained much despite the stock running $100 past his short strike. He asks Phil for a mechanism to adjust the trade and take advantage of the stock's massive run up.

Penny:Phil's response is a brutal, beautiful dose of reality math. Let's look at the actual numbers of Jeho's spread. The $210,350 dollar spread has a width of a $140. He has 34 contracts, so the maximum value of this spread at expiration is $476,000.

Roy:Huge potential.

Penny:Right now, based on current options pricing, his spread is worth a net of $214,200.

Roy:It's currently sitting at exactly 45% of its maximum potential value, with eighteen months left until expiration. The remaining upside to be captured is $261,800.

Penny:Okay.

Roy:If you divide that remaining upside by the current value, Kyos has the opportunity to make a 122% return on his current capital over the next eighteen months.

Penny:A 122% return. And what does he have to do to earn it? Absolutely nothing. T urch has to stay above $350 which it is currently clearing by a massive $100 margin.

Roy:But this is where the psychology of options trading breaks people.

Penny:Oh yeah.

Roy:The member is looking at the screen and asking, why is a spread that is so deep in the money worth only 45% of its max value? It is entirely because of the extrinsic premium remaining in the short $350 calls.

Penny:Can you break down the difference between intrinsic and extrinsic premium for us?

Roy:Absolutely. Intrinsic value is real hard math. If a stock is at $450 and you have the right to buy it at $350 that option has $100 of intrinsic value. It is immediately worth $100 Extrinsic Value is the time premium. It is the extra money people are willing to pay because there's still eighteen months left for the stock to move even higher.

Roy:Those short calls are trading around $222 Since they have $100 of intrinsic value, they still hold $122 of pure time value, or extrinsic premium.

Penny:Think of extrinsic premium like an insurance policy. If I buy car insurance for six months, the policy is worth a lot on munch one because there is a lot of time for me to crash. But on the last day of month six, the premium is basically zero because the time risk has evaporated.

Roy:Precisely and in this trade the member sold those $350 calls. He's the insurance company. He collected that premium. The entire point of his spread is to wait for that $122 of time value to decay to zero.

Penny:Exactly.

Roy:That extrinsic premium is acting like a weight, suppressing the net value of his spread today, but that is not a flaw. That is the mathematical design.

Penny:If he buys those short calls back now to try and restructure the trade, he is paying away the exact premium he built the trade to harvest. It's like planting a fruit tree, watering it, watching the apples grow all summer, and then wanting to chop the tree down right before the autumn harvest just because you're bored and wanna plant something else.

Roy:It's the hand bird hand versus bur Burgers dilemma. Yeah. A bird in the hand is worth two in the bush. Yep. GHOS has a 122% return sitting in his hand with incredibly high probability.

Roy:To adjust the trade now to cash it out and sell $20.27 $420 calls and sell $300 puts like he suggested is not managing a winner. It is making a brand new, highly dangerous bullish bet on a stock at an elevated valuation of $450.

Penny:You are abandoning a sure thing to play with fire all because of the illusion of house money. There is no house money. There is only your capital. As Munger says, avoid cleverness when simplicity is winning. Leave the spread alone.

Penny:Let time do the heavy lifting.

Roy:It requires immense discipline to watch a stock run and do nothing. It goes against human nature.

Penny:It really does.

Roy:But the chatroom also showed how the PSW mechanics capitalize on market fear when the time for action is actually right. The value hunting during today's tech sell off was relentless.

Penny:I wanna rapid fire through three of those live chat set up to show the diversity of tactics. First, Cleveland Cliffs, ticker CLF.

Roy:Okay.

Penny:The stock dropped violently today down to $9. Why? Because Morgan Stanley downgraded them. But get this, Morgan Stanley downgraded them to equal weight with a price target of $13.50.

Roy:The gap between the $9 trading price and the $13.50 bear case target from the analysts is pure irrational market fear. Fundamentally, CLF just reported that auto steel demand is incredibly strong, their order books are full, automotive shipments are at a two year high, and cheap imports are at their lowest level since 2009.

Penny:Great numbers.

Roy:The underlying business is accelerating, but the stock is trading at distressed levels simply because an analyst changed a rating. That is the prime, math based entry point for a value investor.

Penny:Next up, Stellantis, ticker STLA. This is for the PSW $700 a month portfolio, which is designed for smaller, disciplined accounts to slowly compound capital.

Roy:Right.

Penny:Stellantis just reported their first half US vehicle sales rose 5% with June sales up 10%. They are executing their business plan perfectly, yet the stock bottomed out at a six year low on Monday due to broader macro fears.

Roy:So Phil structures a highly disciplined, capital efficient play. He buys the $20.28 dollars 4 calls and sells the $20.28 dollars seven calls, creating a $3 spread. To fund it, he sells near term September $6 calls. The net outlay of capital is incredibly low, the upside is over 85%, and he retains five more quarterly opportunities to sell short term premium against the position. It is maximum upside with highly restricted capital risk.

Penny:And finally, a lesson in what to avoid. Nike, ticker NKE. A member asked if Nike at $40 fit the small portfolio. Phil immediately defaults to his core mathematical rule. Avoid stocks priced over $20 in the small portfolio unless there is a pressing undeniable reason to break the rule.

Roy:And Nike does not provide that reason. Even after a massive headline grabbing dropped to $40 it is still trading at a 20x multiple.

Penny:Too expensive.

Roy:That is far too expensive for a struggling shoemaker with uneven fundamentals. The macro reality is that Nike's core brand is the $300 sneaker, but they are operating in a world where their primary consumers have exhausted their pandemic savings, maxed out their credit cards, and simply cannot afford $300 sneakers anymore.

Penny:Right. It is an expensive turnaround trap, not a deep value play. What an incredible journey today has been. We started by looking past the mirage of the 72,000,000 holiday travelers to see the real plumbing draining the American gas tank.

Roy:Right. The data proved that domestic demand is falling.

Penny:But a wide open export valve is structurally forcing US consumers to pay global clearing prices to pad refining margins.

Roy:And then we watched the exit pipes in the technology sector swell as institutional hedge funds dumped shares at historic rates catalyzed by a hawkish Federal Reserve chair who killed forward guidance and promised a return to brutal bond market volatility.

Penny:And we stepped onto the trading floor to learn the precise mathematical mechanics of survival. We learn how to re underwrite a broken trade on Permian resources by adjusting strikes and building an income fund. Yeah. And conversely, we learn the psychological discipline required to do absolutely nothing when a trade like Teradyne is already perfectly positioned to deliver a 122% return through premium decay.

Roy:Which leaves us with a massive structural question to consider. We talked today about how the physical gasoline market is rigged to export our refined fuels overseas, hollowing out domestic capacity. And we saw how the smart money is actively opening the exit valves on American tech dominance, pulling capital out while the retail investor is trapped in index funds.

Penny:It makes you wonder, if capital continues to violently flee the American tech sector and our physical foundational commodities are structurally mandated to be shipped overseas to the highest bidder, what happens to The US economy in ten years?

Roy:It's the ultimate plumbing question. If we aren't refining our own fuel to support a domestic industrial base, and our smartest capital is abandoning the tech monopolies that drove the last decade of growth what is actually underpinning the US dollar, are we slowly transitioning into an emerging market that just happens to have a really expensive stock exchange?

Penny:Wow! That is the thought you have to take with you to survive this tape because right now the water in the fountain looks beautiful.

Roy:It really does.

Penny:The travel headlines sound great, the window dressing is shiny, but underneath, the pressure is building, the pipes are straining, and the capital is flowing out. Remember, when the facts change, your thesis must change too. Thank you so much for joining us on this deep dive. Keep questioning the headlines, keep looking for the plumbing, and we will see you next time.