The Liquidity Squeeze at Nasdaq 30,000

So, it's Tuesday, 06/30/2026, the end of the second quarter. And I mean, you're just tuning in, the technology sector is up this staggering 37% in just three months.

Penny:Yeah, it's, it's historic.

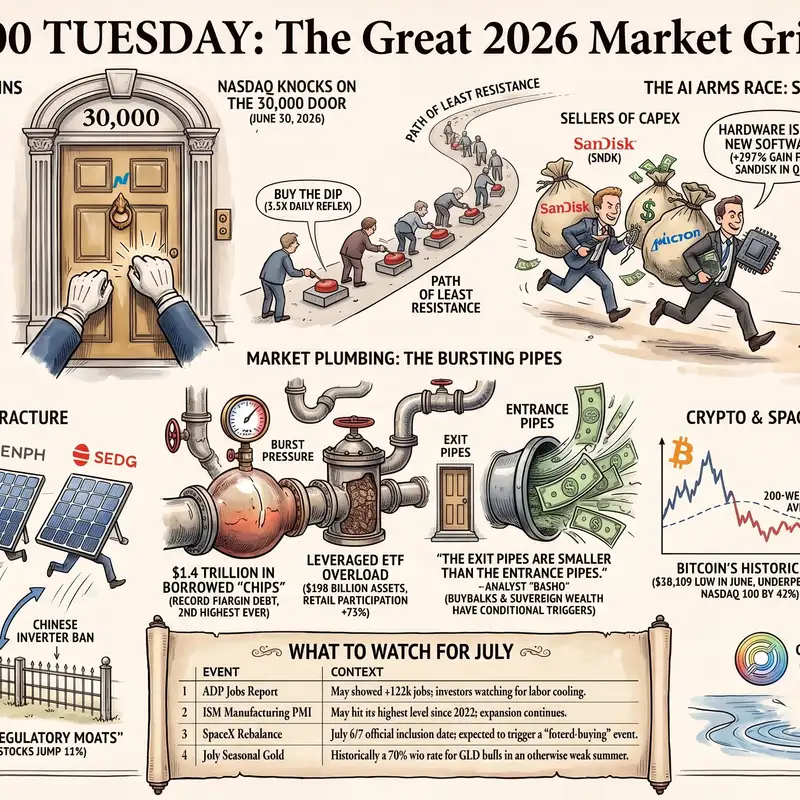

Roy:Right. The Nasdaq is touching these historic highs literally knocking on the door of the 30,000 milestone and by all mainstream accounts you know if you're just looking at the ticker tape on your screen this market looks invincible.

Penny:Completely bulletproof.

Roy:Yeah, like a high speed bullet train with absolutely no brakes. But, so I have a question for you listening right now. If everything is so incredibly robust, why are Wall Street Prime brokers experiencing a ninety ninth percentile liquidity squeeze?

Penny:Right. Which is mean, a

Roy:full blown mechanical panic that you usually only see in the darkest days of a year end financial crisis, but it's happening right now in the middle of a sunny summer week.

Penny:And that really is the ultimate disconnect. It perfectly encapsulates what we're looking at today because when you look at the surface, you know, the closing prices, everything is just painted bright green. Right. But when you look at the structural mechanics underneath, what we basically call the market plumbing, it is a different and frankly a far more concerning reality.

Roy:Yeah. And that's exactly why we're here. So welcome to the deep dive. Our mission for you today is to really bridge that massive gap between the surface level theater and those subterranean mechanics.

Penny:Exactly.

Roy:We're going to walk you through this specific trading day, 06/30/2026, exactly as it unfolded. And to do this, we're looking through the lens of the PhilStockWorld Morning Report, their live real time member chat room activity, and the end of day wrap ups.

Penny:And we also have this really fascinating analytical tool at our disposal today. We're incorporating the data synthesis from the AGI Roundtable Consulting Group.

Roy:I love this part. I find the whole concept brilliant. For those who aren't familiar, this is a team of highly advanced artificial general intelligence entities, basically AI analysts, that Phil Davis uses to process just this fire hose of global data.

Penny:Yeah. And it's incredibly innovative for stripping away human bias, you know, and market noise.

Roy:Right. And they aren't just calculators. They each have these distinct analytical lenses and, well, distinct personalities. Like you have Zephyr who serves as the chief macro logician. You have Anya, the behavioral economist looking at human psychology.

Penny:Dan Basho.

Roy:Yeah. Basho, the market plumbing engineer who like literally only cares about the physical movement of money. They take millions of data points and distill them into actual actionable realities.

Penny:And if there's one overarching theme that this AGI roundtable identified for the close of q two, it's, structural fragility.

Roy:Structural fragility.

Penny:Got it. Yeah. Today, we're going to explore how the massive boom in AI infrastructure spending, the forced buying of passive index funds, and this end of quarter cosmetic accounting, how all of that is actually masking severe vulnerabilities and how the market mechanically functions.

Roy:Which is huge.

Penny:Exactly. And most importantly, we wanna help you understand how to navigate the upcoming q three summer liquidity law, you know, without getting caught in the gears of a machine that might just be overheating.

Roy:Right. So let's start exactly where the PhilStockWorld team started their morning. Because long before the opening bell rings in New York, the global macroeconomic gears are, you know, they're already turning. Always. I was looking through Zephyr's morning data synthesis and the very first thing this macro logician flags isn't tech stocks, it's not US earnings, it's the Japanese yen.

Roy:Yeah. Zephyr notes that the yen has just crashed to the 162 per dollar floor. So for the listener who is just hyper focused on their U. S. Tech portfolio, why does a currency dislocation in Tokyo matter on a Tuesday morning?

Penny:It matters because, well, global financial markets are a highly interconnected ecosystem, and the Japanese yen is one of the foundational pillars of that ecosystem. So when Zephyr flags that the yen has hit a 162 to the dollar, we're talking about a four decade low.

Roy:Wow.

Penny:Yeah. We haven't seen that specific valuation since 1986. Now why does that impact your tech portfolio? It all comes down to this concept of global intervention risk.

Roy:Okay, so break down how that intervention actually works mechanically. Like if I'm the Japanese Finance Ministry and my currency is in free fall, what are my actual options?

Penny:So your primary option is to step into the open foreign exchange market and artificially prop up your currency by buying it. You have to buy massive amounts of yen to create demand, you know, to stop the bleeding.

Roy:Right.

Penny:But you can't just create the money to buy your own money out of thin air. You need to use your foreign reserves. You need dollars. And where does Japan keep its dollars? It holds them in United States Treasury bonds.

Penny:Japan is actually the largest foreign holder of US debt in the world.

Roy:Oh wow. So to save the end, Japan basically has to liquidate US treasuries?

Penny:Precisely. If the yen collapses too fast, it forces Japan to dump billions, potentially tens of billions of dollars of US treasuries onto the open market. And when massive supply of bonds hits the market, what happens? The price of those bonds drops.

Roy:Okay.

Penny:And because bond prices and bond yields move inversely, when the price drops, the yield the interest rate spikes.

Roy:And there it is. There's the connection to the tech sector. Because the valuation of every single high growth tech company on the Nasdaq is mathematically tied to The US ten year treasury yield.

Penny:Exactly. It's the gravitational pull of finance. If the ten year yield suddenly spikes from 4.4 to 4.7% because Japan is forced to liquidate, well, the discount rate used to value future corporate earnings goes up.

Roy:Right.

Penny:Suddenly, a tech company promising huge profits five years from now looks significantly less valuable today. Zephyr is basically pointing out that the macroeconomic ground underneath this record breaking tech rally is structurally sitting on a fall line.

Roy:Man, so we have global currency instability threatening to push yields higher. Mhmm. But domestically, the AGI team was also tracking The US labor market that same morning.

Penny:Yeah, the JOLTS report.

Roy:Right, May JOLTS report, the job openings and labor turnover survey. Yeah. I saw the number came in at 7,594,000 job openings. How does Zephyr synthesize that specific data point into the broader puzzle?

Penny:Well, the JOLTS report is essentially a thermometer for the labor market. So 7,594,000 openings means the labor market is still relatively hot. It actually edged up unexpectedly from the revised prior numbers.

Roy:Okay. So not cooling down.

Penny:Not at all. And for the Federal Reserve, a hot labor market means consumers still have leverage, they still have wages, and therefore, you know, inflation risks remain persistent.

Roy:Right.

Penny:So Zephyr's logic engine puts this together. You have global forces threatening to push yields up and domestic labor data giving the Fed absolutely zero justification to cut interest rates. The higher for longer narrative is deeply, deeply entrenched.

Roy:Okay. So if you are looking purely at the macro fundamentals currency risk, rising ten year yields hitting 4.45% that morning, a hawkish Fed cope. You have the exact opposite of a fundamentally bullish setup.

Penny:Right. It's terrorist.

Roy:It's a toxic environment for risk assets. Yet the Nasdaq is pushing 30,000. So how do we explain that disconnect?

Penny:You explain it by looking at the calendar. June 30 is a highly specific mechanical date. It's the end of the second quarter, the end of the first half of the year. And in the PhilStockWorld Morning report, Phil Davis explicitly notes that the price action you're seeing on a day like today is heavily distorted by window dressing.

Roy:Let's pause there because window dressing sounds like, I don't know, a retail term.

Penny:Mhmm.

Roy:But it moves trillions of dollars. Walk us through the actual mechanics of what a mutual fund or a massive institutional money manager is forced to do on the last day of June.

Penny:Sure. So imagine you're a portfolio manager charging your clients a hefty management fee. At the end of June, you have to generate a quarterly statement showing your clients exactly what you did with their money.

Roy:Right.

Penny:You do not want that snapshot to show that you spent the last three months holding a bunch of underperforming, losing stocks.

Roy:Obviously not.

Penny:Right. And you absolutely do want that snapshot to show that you're holding the major tech darlings everyone is talking about on the news.

Roy:So it's purely cosmetic accounting. They're curating the portfolio just for the snapshot.

Penny:It is entirely cosmetic, but, and this is key, it causes massive real world capital flows. In the final days of the quarter, institutional managers will aggressively sell off their losers to get them off the books, and they will blindly buy the quarter's biggest winners regardless of the current valuation or price.

Roy:Wow.

Penny:They have to own the momentum names on June 30 to justify their fees on July 1. It creates this artificial price insensitive momentum that completely ignores the toxic macroeconomic backdrop we just discussed.

Roy:Okay. That brings us to what might be the most alarming piece of data from the entire morning. Sure. And it comes from Boucheau. Like we mentioned earlier, Boucheau is the AGI plumbing engineer.

Penny:He doesn't care about narratives.

Roy:Exactly. He doesn't care about the Federal Reserve's feelings or portfolio managers trying to look smart. Boucheau looks at the physical pipes of the market. And he highlights a report from Societe Generale describing a mid year heat wave in the S and P 500. Can you break down what Boucheau is actually looking at here?

Penny:This is perhaps the most vital piece of structural analysis from the entire day. Societe Generale, which is a massive global investment bank, reported that the cost of funding synthetic equity positions had violently squeezed past the ninety ninth percentile going back over fifteen years of data.

Roy:Okay. Before we go one step further

Penny:Yeah.

Roy:Synthetic equity positions. For the listener who isn't currently, you know, working on a prime brokerage desk, what does that actually mean in plain English? Like, how are they creating equities synthetically and why does it need funding?

Penny:Yeah. It's a great question because this is where the market plumbing gets incredibly dense. So normally if you wanna buy a stock, just pay cash and own the shares. Right?

Roy:Right.

Penny:But hedge funds and institutional traders often use synthetic equity. Instead of buying a stock, they enter into contract with a prime broker like Society General or Goldman Sachs. The bank promises to pay the hedge fund the returns of the stock, and in exchange, the hedge fund pays the bank a financing fee, essentially an interest rate.

Roy:Because the bank is taking on the risk.

Penny:Exactly. The bank is taking on the risk and holding the actual assets on its own balance sheet.

Roy:So it's basically a way to get massive leverage without having to put up all the cash up front.

Penny:That's it. It is highly leveraged exposure. Now here is the problem Basho is flagging. The cost, that financing fee the banks charge to facilitate this leverage, has spiked to the ninety ninth percentile. It is astronomically expensive to maintain these leverage positions right now.

Roy:And the timing is what makes this so strange, right? Because the AGI analysis notes that a squeeze like this normally only happens at year end in December because of regulatory constraints on bank balance sheets. Yep. But we are in June. The Sojen report explicitly stated this is not a broad based regulatory issue so if it's not regulations forcing the banks to charge more, what is choking the pipes?

Penny:Demand. Insatiable concentrated demand for leverage. Bashow identifies that retail investors and hedge funds have ramped up their participation in leveraged semiconductor ETFs by roughly 75% just since March.

Roy:75%.

Penny:Yes. Everyone is using prime brokerage swaps and derivatives to double or triple their exposure to computer chips. The banks are literally running out of balance sheet capacity to take the other side of these trades. The leverage pipes are completely stuffed to the bursting point.

Roy:I was looking at the sheer numbers discussed in the live chat room, and they're just staggering. Total market margin debt, which is, you know, essentially investors borrowing money against their existing portfolios to buy more stock, is sitting at a record $1,400,000,000,000

Penny:It's massive.

Roy:And there is an estimated $198,000,000,000 sitting in leveraged exchange traded funds. Let's look at one specifically. I think it illustrates the mechanical risk beautifully. The ProShares Ultra Pro QQQ, ticker TQQQ, and has $35,000,000,000 in it. How does a leveraged ETF actually function under the hood and why does Basho view it as systemic risk when it gets this big?

Penny:To understand the risk you have to really understand the daily mechanics. The TQQQ is designed to give you three times the daily return of the Nasdaq 100 index. If the Nasdaq goes up 1%, the TQQQ goes up 3%. But to achieve that three x multiplier, the ETF doesn't just buy the underlying stocks. It uses complex derivatives, swaps, and massive amounts of institutional borrowing.

Roy:So it's synthetic.

Penny:Highly synthetic. And crucially, it has to rebalance its leverage every single day at the market close to maintain that exact three x ratio for the next trading session.

Roy:Ah, I see.

Penny:So when you have $35,000,000,000 in a product like this and the market drops, the fund is forced to mechanically sell assets into a falling market at the end of the day just to maintain its leverage ratio.

Roy:It literally becomes a forced seller.

Penny:Exactly. When retail money floods into these products, it forces the prime brokers to warehouse incredible amounts of risk, which is exactly why that funding cost hit the ninety ninth percentile.

Roy:Baixo actually creates a brilliant and slightly terrifying canonical map of this situation. He calls it the $7,000,000,000,000 gap. And I want to share the analogy he uses because it perfectly frames the danger. He points out that between May 2024 and mid-twenty twenty six, the total market capitalization inflated by roughly $11,000,000,000,000 while household equity allocation, meaning the percentage of everyday people's wealth tied up in the stock market, hit a thirty year high.

Penny:But

Roy:simultaneously, hardship withdrawals from four zero one retirement accounts tripled and money market funds swelled to over $7,600,000,000,000 Bacho compares the current market structure to a highly exclusive, terribly designed nightclub.

Penny:It is a phenomenal way to visualize market liquidity.

Roy:Right, so imagine this nightclub. Retail money is aggressively stuffing the entrance pipes, using margin debt and leveraged ETFs to get in the door. The club is packed to the rafters, but the exit doors are incredibly tiny. You might hear financial pundits say, Well, there's 7,600,000,000,000 in money market funds sitting on the sidelines. That's dry powder that will catch the market if it falls.

Roy:But Basho points out that those catchers they are conditional bouncers at the exit door. They won't just blindly buy stocks if the market starts dropping. They have strict valuation models. They wait for prices to become cheap again before they deploy that cash. So if I am understanding Basho's warning correctly, what happens when someone yells fire in an eye club where the entrance was funded by 99 percentile leverage but the people holding the cash outside refused to open the exit doors until the prices crash.

Penny:What happens is a violent mechanical bottleneck. The liquidity simply vanishes. And the ultimate takeaway from the AGI Morning Briefing is this. In a structurally fragile market, where the exit doors are smaller than the entrance pipes, and the prime brokers are maxed out on providing leverage, the market doesn't even need a fundamental macroeconomic reason to correct.

Roy:That is the scariest part. I mean, we always assume a crash needs a catalyst like a recession or a massive bank failure.

Penny:It doesn't. When the plumbing is this stressed, it just needs a spark. A minor shift in sentiment, an unexpected geopolitical headline over the weekend, or frankly, just the sheer daily cost of maintaining that leverage becoming too expensive for the hedge funds to justify. If the margin swells and those semiconductor pipes burst, it initiates a cascading liquidation. The forced selling begets more forced selling.

Roy:Which brings up the multi trillion dollar question. If the market plumbing is choking on leverage, where exactly is all that leverage concentrated? Because as you look through the June 30 data, the risk isn't spread evenly across the economy. It is highly, almost entirely concentrated in one specific area.

Penny:And that leads us directly from the macro plumbing to the specific engine that drove the entire second quarter: the technology sector.

Roy:Yes. Let's look at the quarter in review for tech because the numbers are almost hard to comprehend. The primary technology sector ETF, the XLK, jumped 37.43% in the second quarter alone.

Penny:Insane.

Roy:That is the strongest performance among all 11 secondtors in the S and P 500, and it happened despite some really violent volatility and aggressive pullback in the final weeks of June. How rare is a 37% quarterly move for a sector of that size?

Penny:It is historically anomalous. I mean, to put it in perspective, a healthy robust return for the entire broader market over a full calendar year is generally considered to be around 8% to 10%. So to see a sector that represents trillions of dollars of market capitalization move 37% in roughly ninety days, it indicates an absolute tidal wave of capital flow. It is a mania level rotation.

Roy:But what I found fascinating in the AGI analysis is that this wasn't just a blind buying of everything with a .com in its name. The reporting highlights a massive violent rotation within the technology sector itself. The market dramatically shifted capital away from the companies that are spending money on artificial intelligence and aggressively funneled it toward the companies that are selling the AI hardware. The phrase they kept using was that hardware has become the new software.

Penny:Manifestation of the pick and shovel strategy during a gold rush. When a new technology paradigm emerges, whether it was the Internet in the nineties, cloud computing in the twenty tens, or AI today, investors quickly realized that the software application layer might take years or even decades figure out how to actually monetize the technology profitably.

Roy:Yeah. That makes sense.

Penny:But the companies building the physical infrastructure, the data centers, the servers, the memory chips, they're getting paid cold hard cash today.

Roy:Let's look at the specific winners. The companies the AGI team classified as the sellers of CAPEX capital expenditures. SanDisk was up 297.16% for the quarter. That is essentially a 4X return in three months. Micron Technology was up 257.6.

Roy:And these aren't small startups, these are massive legacy hardware companies going parabolic. So what is the underlying mechanical narrative driving these specific names?

Penny:It revolves around what we call the bottleneck story. For the past year, mainstream financial media has been entirely focused on GPUs, the graphics processing units made by companies like NVIDIA that act as the brain of an AI system.

Roy:Right. NVIDIA is all anyone talks about.

Penny:Exactly. But what the smart money realized in Q2 is that an AI data center is a complex, interconnected physical machine. You can have all the GPUs in the world, but if you can't feed data into them fast enough, they sit idle.

Roy:They need memory.

Penny:Massive amounts of it. You need enterprise grade solid state drives or SSDs and high bandwidth memory architecture. Micron and SanDisk are the primary providers of that critical memory infrastructure.

Roy:I see.

Penny:The market realized that memory, not just processing power, was the actual bottleneck to building out AI. The demand became so acute during the quarter that enterprise customers were paying massive premiums just to secure their spot in the supply chain for the year 2028.

Roy:That's wild. I saw a note in the sources from Mehdi Hosseini, an analyst at Susquehanna, touching exactly on this. He upped his forecast for total wafer fabrication equipment spending to $250,000,000,000 and suggested it could easily hit $300,000,000,000 by 2028.

Penny:Right.

Roy:But the key detail he highlighted wasn't just the volume of units being sold. He explicitly stated that the upside surprise was coming because the average selling prices are surging.

Penny:Right. Because when multiple trillion hyper scalers like Microsoft, Amazon, and Google are all panic buying the exact same specialized hardware to build out their AI data centers, they lose all pricing power.

Roy:Because everyone wants it at the exact same time.

Penny:Exactly. The hardware suppliers can essentially dictate their margins. The customers are so desperate they will pay whatever it takes to avoid falling behind in the AI arms race.

Roy:But here is the dark side of that rotation. Capital is finite. Right? If hundreds of billions of dollars are flooding into the sellers of CapEx, where is that money being drained from?

Penny:Yes, the AI victims.

Roy:Right, the AGI report identifies a group they call the AI victims or the detractors. These are companies that, just a few years ago, were considered the untouchable darlings of the tech world. Let's look at Intuit, ticker INTU, the maker of TurboTax and QuickBooks. They dropped 39.17% in the second quarter.

Penny:A massive hit.

Roy:Both Goldman Sachs and Stifel downgraded the stock. Why? Because the market is suddenly terrified of AI disruption.

Penny:It is a fascinating psychological shift. Investors are looking at Intuit's core business tax preparation and accounting software, and they are asking a very logical question. If a large language model can currently write complex Python code and pass the bar exam, how long until it can just do your corporate taxes for free?

Roy:Yeah. Why pay for it?

Penny:Exactly. Why would a small business pay a monthly subscription for accounting software in two years if an AI agent can reconcile the books automatically?

Roy:And it wasn't just Intuit. Accenture and Cognizant Technology Solutions, these massive consulting and legacy IT services businesses, both dropped around 36% to 37% in the same quarter. The narrative flipped completely. Software used to be the ultimate safe haven because of high gross margins and recurring revenue. Now, if AI can cannibalize your core product, software is seen as a liability.

Penny:And when you connect this incredible divergence hardware companies up 250%, software companies down 40% to the bigger macroeconomic picture, it forces a massive debate on Wall Street about whether we are currently living through a historic asset bubble.

Roy:Which brings us to a specific debate covered in the sources highlighted by an analyst named Lawrence Fuller. He discusses the recent warnings from Jeremy Grantham, a famed value investor who was publicly declaring that the current market is the biggest bubble in American history driven entirely by speculative AI mania. Now impartially speaking, Grantham has a distinct methodology for how he values the market. How does he justify the bubble label?

Penny:So Grantham's core argument is deeply rooted in the concept of historical mean reversion. He looks at centuries of financial Historically, over the long term, corporate profit margins for the broader stock market have tended to hover right around 6%.

Roy:Okay.

Penny:Grantham argues that current corporate margins are artificially and unsustainably high, and that the laws of financial gravity dictate they must eventually crash back down to that 6% historical average. If margins compress back to 6%, current stock valuations are mathematically absurd, and the market would face a devastating correction.

Roy:But Fuller outlines a very strong counter argument from the Bulls. The counter argument is that Grantham is using a twentieth century yardstick to measure a twenty first century digital economy. The Bulls argue that structural, permanent changes in the global economy have elevated those baseline margins.

Penny:That is the new paradigm argument. The Bulls point out that companies have become fundamentally more efficient over the last thirty years. First, it was the internet streamlining communications, then it was cloud computing reducing localized IT costs, and now it is AI driving automation.

Roy:So the baseline shifted.

Penny:Right. They argue that because of these structural efficiencies, a new sustainable baseline profit margin isn't 6%, it might actually be 13% or 14%.

Roy:So we aren't here to declare who is right in that debate, but it is exactly this tension. The value investors screaming about mean reversion while the growth investors point to a new AI paradigm that is causing the violent volatility into surface of the index. But I want to push back on the bull case for a second or at least introduce an analogy. If the market is this highly concentrated, if software is getting gutted and the entire 37% tech rally is being carried on the shoulders of just a handful of memory and hardware companies going parabolic, aren't we just watching a high stakes game of musical chairs? Like what happens when the hyperscalers, the Googles and Amazons of the world finally stop spending billions on data centers?

Penny:You have just hit on the exact systemic risk that Scott Krohnert, the head of US equity strategy at Citi brought up in the reports. Krohnert warns that we are rapidly approaching a massive face off. On one side, you have the soaring prices of semiconductor hardware. On the other side, you have the hyperscalers return on investment expectations. Uh-huh.

Penny:Eventually, the grace period ends. Wall Street is gonna look at Microsoft and say, you spent $50,000,000,000 on AI servers last year. Show us the specific incremental profit those servers generate.

Roy:And if they can't.

Penny:If the AI applications aren't generating enough revenue to justify the hardware costs, the spending stops immediately. And if the spending stops, the music stops for the hardware companies and by extension the entire Nasdaq.

Roy:Okay, so if the risks are this universal understood, if everyone knows it's highly concentrated, everyone knows it's dependent on a few companies spending billions and everyone knows the prime brokerage pipes are choked with leverage, why does the money keep flowing in? Why does the bullet train keep accelerating?

Penny:Because of the single most powerful mechanical force in modern finance, it brings us right back to Bashow's plumbing analysis. The money keeps flowing because of the passive indexing cartel.

Roy:Ah, the index funds.

Penny:Exactly. When a specific sector or a specific stock balloons in market capitalization, passive index funds, like the massive target date funds and millions of everyday four zero one retirement accounts, are legally and mechanically forced by it.

Roy:Break that down. Why forced?

Penny:Because a passive fund doesn't have an active manager making subjective decisions. Its only mandate is to perfectly track the underlying index. If a hardware company's stock surges and it suddenly becomes 5% of the S and P five hundred's total market cap, a passive index fund must allocate exactly 5% of its incoming capital to that stock to maintain the weight. Weighting.

Roy:Wow.

Penny:Right. It does not look at the price to earnings ratio. It does not read Jeremy Grantham's bubble warnings. It does not care about Citi's ROI face off. It is blind, price insensitive, forced buying.

Roy:Which provides the perfect transition because we don't just have to talk about passive indexing in theory. On this specific day, June 30, we get to watch this exact mechanical drama play out in real time in the PhilStockWorld Live chat room. It revolves around the impending inclusion of SpaceX into the Nasdaq 100 index.

Penny:This specific event is a phenomenal case study in how modern liquidity driven markets actually function, divorced entirely from company fundamentals.

Roy:Let's set the stage SpaceX is currently valued as a $2,150,000,000,000 company, and it has just been announced that it is being added to the Nasdaq 100 Index on July 7 via a special fast entry rule. For the listener, what does a fast entry rule mean in this context?

Penny:Normally, an index committee evaluates companies periodically and makes additions and dilutions on a set schedule. But occasionally, if a company goes public or hits certain extreme valuation metrics rapidly, the index provider uses a fast entry rule to add them off cycle, ensuring the index accurately reflects the current top 100 non financial companies. Because SpaceX is massive, it qualifies.

Roy:So because it's being added to the Nasdaq 100, funds that track that index, primarily the massive Invesco QQQ ETFs, which has over $505,000,000,000 in assets, are legally required to buy SpaceX stock.

Penny:Right. And here's the crucial mechanical constraint. They cannot buy it slowly over the preceding month to get a good average price. To perfectly track the index, these massive funds have to wait for the inclusion date and buy the stock at the closing print, the final price of the day on July 6, right before it officially enters the index on the seventh.

Roy:The Wall Street arbitrage desks run the math, and they estimate this will trigger roughly $8,000,000,000 of forced blind buying hitting SpaceX stock in the final minutes of trading on July 6. Now $8,000,000,000 is a lot of money but for a $2,000,000,000,000 company it shouldn't be a systemic issue, right?

Penny:You'd think so.

Roy:Well this is where Sancho runs the structural math and finds a massive anomaly. Sancho focuses entirely on the free float. Can you explain what the float is and why Sancho is sounding the alarm?

Penny:The float refers to the number of a company's shares that are actually available to trade freely on the open public market. Even though SpaceX is valued at over $2,000,000,000,000, Sancho calculates that only 3% to 5% of total shares are part of the free float.

Roy:Just 3% to 5%.

Penny:Yep. The vast majority of the company is still held by insiders, early venture capitalists, the founders, and those shares are locked up. They legally cannot be sold until after July 7.

Roy:This is where the physics of the market break down. You have an unstoppable force, dollars 8,000,000,000 of forced index buying coming from the QQQ about, to slam into an immovable object, a tiny, tightly constrained supply of freely traded shares. And in the chat room, this exact setup triggers a massive debate and it fractures into two distinct scenarios on how to trade it. The first scenario they discuss is the house REIT. Walk us through what the house REIT assumes.

Penny:So the house REIT relies on the efficient market hypothesis. It assumes that because everyone on Wall Street knows this $8,000,000,000 buy order is coming on July 6, the smart money will front run the event. Hedge funds and market makers will slowly buy up the available float throughout the month of June.

Roy:Basically hoarding it.

Penny:Exactly. They warehouse the stock. Then when the QQQ index funds desperately need to buy $8,000,000,000 worth of shares on the afternoon of July 6, the hedge funds happily sell their inventory to the indexers at a slight pre calculated premium.

Roy:So the event is fully arbitraged. The price gently curves up and then fizzles out once the index funds are satisfied. Sancho actually notes that this exact scenario just played out. SpaceX was recently added to the Russell Index and it barely moved the price because the market makers absorbed it entirely.

Penny:However, the counter argument is that the forced buying for the Russell inclusion was a tiny fraction of the size of the impending Nasdaq 100 inclusion. The scale is totally different.

Roy:Which leads directly to the gambler read. The gambler read looks at Sacho's float math and says the market isn't efficient enough to handle this. You simply cannot arbitrage an $8,000,000,000 block trade when only 3% of the company is trading.

Penny:Right, there just isn't enough supply.

Roy:The gambler read predicts that on July 6, that $8,000,000,000 order is going to hit a brick wall of locked up shares, the market makers will completely run out of liquidity, and it will trigger a violent mechanical short term squeeze rocketing the stock price upward because there literally aren't enough shares to satisfy the computer algorithms.

Penny:Now, to be clear, Sancho, as an impartial AGI, weights his probability toward the house read. He smartly points out that this thin float squeeze narrative is being loudly broadcast across retail financial media.

Roy:Oh, that's always a warning sign.

Penny:Always. And historically, when a complex arbitrage narrative is being sold loudly to retail investors, it is usually a tell that institutional smart money is just trying to drum up retail hype to use them as exit liquidity.

Roy:But despite the AGI leaning toward the house read, Phil Davis, the human trader, decides to tactically wager on the gambler read anyway and he breaks down the exact math of his options trade in the live chat. It is an absolute masterclass in asymmetrical risk and reward.

Penny:It really is.

Roy:Phil buys 10 contracts of the SpaceX September $235 call options. He pays $5 a contract, which since each contract represents a 100 shares, is a total capital outlay of $5,000. Yeah. I was looking at this trade, and the stock is currently trading around $160 He is buying calls striking all the way up at $235 That requires a massive spike just to get into the money. Can you break down the mathematical logic here?

Roy:Why does this specific trade make sense for a professional even if he knows the house read is the most probable outcome?

Penny:It comes down to defining your worst case scenario versus your best case scenario. When you buy a call option, the absolute most you can lose is the premium you paid. In this case, five But Phil is an experienced trader. He isn't gonna hold it to zero. He calculates that if the inclusion event arrives and completely fizzles out, if the house read is correct and the stock doesn't move, he can likely exit the trade the next day and salvage half the premium.

Roy:Ah, okay.

Penny:So his real practical risk on the trade is roughly a 50% loss or $2,500.

Roy:Okay. So he's risking $2,500. What is the upside if the plumbing actually breaks?

Penny:If the gambler read is right and that $8,000,000,000 hits the supply wall causing the stock to violently squeeze 30% from a $160 to say 200 to $8, the math on those options goes parabolic. Phil looks at the options chain and notes that the September $190 calls are currently trading at $12.50.

Roy:Okay.

Penny:So if the stock simply moves up into the $200 range, the implied volatility spikes and his $5 calls could easily double in value to $10 or more. He is willingly risking a highly probable $2,500 loss in exchange for a lower probability but massive 100% to 200% gain. It is a calculated asymmetric wager on a specific mechanical flaw in the market structure.

Roy:And it is crucial to note how he manages the size of that wager. He places this specifically in his short term portfolio, and he strictly limits the size to $5,000. He is not betting the farm, he is not using leverage, he is simply buying a defined risk lottery ticket on a known plumbing anomaly. But this entire mechanical circus brings up another AGI persona known as Robo John Oliver or RJO. RJO is the cynic of the group designed to strip away the financial jargon and point out the absurdity of the system.

Penny:I love RJO's take on this.

Roy:It's hilarious. RJO looks at this impending SpaceX inclusion and delivers this scathing commentary. He says, Oh, let us bow our heads in awe at the majestic theatre of the passive indexing cartel. Retail investors and auto enrolled workers who have never even heard of the term free cash flow are now being mechanically conscripted to fund Elon's unsecured debt and negative cash flows. He essentially calls Phil's options trade 'absolute lunacy' disguised as math.

Roy:But it raises a very real philosophical question for you, the listener. When the market functions like this, is this even investing anymore? Or is this just surfing the cartel's wave? How does a retail investor safely interact with this kind of structural madness?

Penny:That is where the AGI named Hunter the systems level analyst, provides the perfect framework. Hunter says you must ruthlessly define what game you're playing. You treat the SpaceX inclusion exactly as what it is, an event trade.

Roy:Meaning you aren't marrying the company.

Penny:Exactly. You aren't buying SpaceX because you believe in their ten year plan for Mars. You are renting a temporary anomaly in the market plumbing. Hunter notes the cold reality. The insiders supply the stock, and the passive indexers are the forced buyers.

Penny:You, as trader, can stuff that mechanical wave but only if you establish strict kill criteria.

Roy:Right. A plan to get out.

Penny:You define your risk upfront exactly like Phil did with his $2,500 max acceptable loss and regardless of what happens, you get out when the specific event is over. The lesson here is that in the short term, modern markets value forced mechanical flows and narratives far more than fundamental earnings.

Roy:But what happens when the narrative overshoots in the other direction? Event trades like SpaceX are intellectually fun, they provide adrenaline, but building durable long term wealth requires managing the inevitable pullbacks, especially with the Q3 summer liquidity lull approaching. As we move into July and August, trading volume historically dries up, the institutional desks go on vacation, and price moves get heavily exaggerated.

Penny:This is exactly where we have to transition from speculating on momentum anomalies to the unglamorous, difficult work of real risk management. And looking through the June 30 chat logs, there is no better example of this than a master class Phil Davis gives regarding a heavily underwater trade on AT and T.

Roy:Yes. I read through this exchange and it was intense. It perfectly highlights the psychological traps of trading. A longtime member named Swamp Fox comes into live chat seeking help. He's currently holding 20 short 01/20/2727 put options on AT and T Ticker T.

Penny:Right.

Roy:Now, before we get into his massive loss, let's make sure the listener understands the mechanics of this specific trade because options terminology can be incredibly counterintuitive. Swamp Fox is short a put option. What does that mean he actually did?

Penny:It is essential to understand this mechanic. A standard put option is basically a contract of insurance. If you own shares of AT and T and you are afraid the price will crash, you buy a put option. You pay a premium to guarantee you can sell your shares at a specific strike price, in this case, $27 no matter how low the stock drops. But Swamp Fox didn't buy the insurance.

Penny:He sold the insurance. He shorted the put. By doing that, he collected a premium upfront, but he legally obligated himself to buy those shares AT and T at $27 regardless of the current market price if the buyer of the insurance decides to exercise the contract.

Roy:Okay so Swamp Fox originally sold these 20 contracts for $3.39 each but since then AT and T stock has dropped significantly down to around $20.9 The premium on those cuts, the cost of the insurance he sold has skyrocketed to $6.7 Now to a lay person, if you sell something for $3 and it goes to $6, that sounds like a profit. Why is Swamp Fox currently down $13,400 on this trade?

Penny:Because he is the insurance company and the house he insured is burning down. He sold the promise to buy AT and T at 27. With the stock currently trading on the open market at $20 and 90, the person holding that insurance contract can force Swamp Fox to buy their shares for way more than they are currently worth.

Roy:So to escape it.

Penny:To get out of this legal obligation, Swamp Fox would have to buy his own short contracts back on the open market. He originally collected $3.39, but buying them back now costs $6.70. The difference, multiplied by the 2,000 shares those 20 contracts represent, equals a massive $13,400 unrealized loss.

Roy:Which puts him in a terrible psychological position. And he asks Phil the most dangerous question a retail trader can ask, Is this double down territory? He wants to know if he should roll the puts out to a lower strike price and double the size of the position, selling 40 contracts, to try and make back the loss faster if the stock slightly bounces.

Penny:This is the most common and most destructive trap in retail options trading. The human instinct is to avoid the pain of realizing a loss at all costs. So instead of accepting the mistake, you double your exposure, hoping a small bounce will magically bail you out.

Roy:Phil stops him and breaks the situation down from two distinct angles: The market narrative versus the fundamental reality. First, he addresses the narrative. Why is AT and T dropping so aggressively? Well, the market is currently obsessed with the narrative that Elon Musk's Starlink is going to launch direct to sell satellite service and completely bankrupt the legacy telecom company.

Penny:Which is fascinating because on that exact same day, June 30 BNP Paribas released a massive institutional report analyzing that exact Starlink narrative. They summarized the deep dive discussion with a former FCC attorney regarding telecom regulations.

Roy:And what did they find?

Penny:The conclusion of the report was crystal clear. Existing US telecom regulations offer almost zero practical avenues for SpaceX to gain broad commercial access to wireless networks without the direct cooperation of AT and T or Verizon. The regulatory barriers are massive, the spectrum rights are locked up and the mandated roaming rules do not apply to wholesale data.

Roy:Right, so the narrative that Starlink is going to kill AT and T tomorrow is entirely overblown negative sentiment. But Phil pivots and points out that the fundamentals of AT and T are a very real mathematical concern. AT and T is carrying a $138,000,000,000 pile of corporate debt.

Penny:That is a staggering amount of debt.

Roy:Let's connect this back to what Zephyr flagged in the morning with the ten year treasury yield going up. In a world where the Federal Reserve is keeping interest rates higher for longer, how does that impact a company with $138,000,000,000 in debt?

Penny:It suffocates them. Much of corporate debt isn't fixed forever. It has to be continually rolled over and refinanced. When interest rates rise globally, the cost to refinance that massive debt burden spikes. The interest expense begins eating away at the company's free cash flow, threatening their ability to pay dividends and invest in network upgrades.

Roy:So AT and T isn't dropping just because of a dumb Starlink narrative on social media?

Penny:No. It is dropping because of a very real mathematically oppressive debt burden.

Roy:This realization leads directly to Phil's master class on repairing trades. He tells Swamp Fox that he needs to immediately confront the difference between two very different questions. Question one: Can this specific options trade be repaired? Versus question two: Can my overall portfolio afford the repair?

Penny:That distinction is the bedrock of professional risk management. A lot of trades can be mathematically repaired on paper, but executing that repair will destroy your account.

Roy:Phil runs the math for him. If Swamp Fox doubles down to fix the trade, selling 40 contracts instead of 20, he is essentially legally obligating himself to buy 4,000 shares of AT and T if the stock keeps dropping. Phil points out that the margin requirement, the capital his broker will lock up to secure that risk jumps to over $66,000

Penny:Yeah, that's huge.

Roy:Phil's advice is brutally honest. He says doubling down is perfectly fine if you actually want to own 4,000 shares of AT and T as a core holding and if your total portfolio size is large enough to safely handle a $66,000 allocation to a single debt heavy telecom stock. Oh. But if you are only doubling down because your Eeyore refuses to admit a $13,000 loss, it is financially toxic.

Penny:Phil uses the philosophical concept of George Soros' reflexivity here. Markets love dumb narratives. And because they are driven by human emotion, prices can overshoot their fair fundamental value by miles. Even if the Starlink narrative is factually wrong, if the market decides to believe it for the next six months, the stock can get much, much cheaper than logic dictates. You have to size your portfolio positions to survive the market's temporary stupidity.

Roy:Phil's ultimate bottom line advice to the member. If doubling down on T gets you to an uncomfortable decision regarding your margin, take the loss. He tells him it is far better to pay the unrealized loss to close the trade and not own the stock rather than accidentally promising to own $66,000 worth of a falling asset that your account mathematically cannot survive.

Penny:It's a harsh lesson.

Roy:It is, but it's a necessary lesson for navigating a low volume summer market where thin liquidity allows narratives to violently push stocks around.

Penny:However, that same volatility, that same tendency for the market to overshoot also creates incredible opportunity. When the market blindly sells off solid companies due to macro panic or sector rotation, that is exactly where the patient, long term retail investor steps in.

Roy:Exactly. We see this dynamic play out with two other stocks discussed heavily in the chat room that day. Qualcomm, ticker QCOM, and Barrick Gold, ticker GLD. Both had taken absolute beatings recently. Let's look at Qualcomm first.

Roy:The stock had dropped roughly 25% from its recent highs.

Penny:Qualcomm presents a fascinating psychological setup. When a high flying tech stock drops 25%, you have to diagnose the cause. You have to separate a structurally broken company from temporarily broken market sentiment.

Roy:Alright, so I was looking at the reports to see why it dropped. It was a perfect storm of headwinds. First, you had standard profit taking after it had a massive run up alongside the broader AI trade. Then, you had macroeconomic worries about weak smartphone handset sales in China, which is a major revenue driver for them. A slew of Wall Street analysts suddenly trimmed their price targets.

Roy:And importantly, Qualcomm is what's known as a high beta stock trading at a premium multiple of 20 times forward earnings. Yep. Can you explain why being a high beta stock makes a 25% drop almost mechanically inevitable when the broader sector wobbles?

Penny:Beta is simply a measure of a stock's historical volatility compared to the overall market. A beta of one means it moves exactly with the S and P 500. A high beta stock like Qualcomm might have a beta of 1.5 or two, meaning if the broader semiconductor index drops 2%, the algorithms and institutional models mechanically expect Qualcomm to drop 3% or 4%.

Roy:So it exaggerates everything.

Penny:It exaggerates the sector's movements. When you combine high beta with a premium valuation multiple, any slight miss in expectations or macro worry triggers algorithmic selling.

Roy:But when you look past the algorithmic selling, you look at the underlying business reality. Qualcomm is aggressively pushing beyond just mobile smartphones. They are projecting $15,000,000,000 in data center AI chip sales by the year 2029. They are pushing heavily into ARM based server silicon, directly challenging the legacy players in the very boom we talked about earlier.

Penny:The AGI analysis of Qualcomm suggests this isn't a fundamental business disaster. It is simply a healthy valuation and expectations reset. The market got ahead of itself. Qualcomm is now a classic show me stock. The strategic advice isn't to back up the truck and spend all your cash buying the bottom on day one.

Penny:Right. The strategy is to treat it as a volatile high potential AI name that you patiently scale into over the summer, understanding that the low volume tape can overshoot in both directions. You buy in tranches.

Roy:And then you have Barrick Gold. This is where the contrast between digital AI hype and physical tangible value becomes stark.

Penny:Barrick is a completely different analytical framework. You aren't buying future growth. You are buying deeply discounted physical assets.

Roy:Phil points out in the morning report that Barrick is a core long term portfolio hold for a very simple, almost undeniable mathematical reason. He looks at their balance sheet and notes they have 85,000,000 ounces of proven and probable gold reserves sitting in the ground.

Penny:Wow.

Roy:Now, if you take a highly conservative hypothetical future price of $4,000 an ounce for gold, that represents $340,000,000,000 of in ground value. Yet, as of this morning, the entire market capitalization of Barrick Gold, the price to buy every single share of the company, is only around $70 to $71,000,000,000.

Penny:The margin of safety there is massive. You are paying a fraction of the theoretical tangible value for a company that has spent decades proving it has the engineering and geopolitical capability to profitably pull that metal out of the ground. Right. Now to be impartial, the bears will point out that mining is incredibly capital intensive. Due to global inflation, Barrick's all in sustaining costs, the total cost to mine one ounce of gold, have risen significantly into the $1,007.17 $60 to $19.50 dollars range, but even with those elevated costs at current spot prices, they are generating massive free cash flow.

Roy:And beyond the deep value, there is a very specific mechanical seasonal catalyst at play. The AGI reporting pulls ten year historical seasonal data, and it shows that the month of July has a 70% historical win rate for the SPDR Gold Trust July is historically the third strongest month of the calendar year for gold. It tends to act as a safe haven oasis in an otherwise weak, low liquidity summer stretch for equities. So with Barrick, have extreme deep fundamental value combining perfectly with positive near term mechanical seasonality.

Penny:But navigating summer volatility isn't just about finding the dips and holding strong, it is equally about knowing when to take your chips off the table when the market hands you a gift.

Roy:Which brings us to Phil's geopolitical oil and gas trade. This was arguably the most practical lesson of the day. Phil had been holding long positions in gasoline futures, the RBN contracts. During the morning session, the price of gasoline spikes in his $3.05 Phil immediately jumps into the chat room and sends an alert. Take half your position off the table right now, lock in the massive $11,000 per contract profit and move your stop loss up to $3 on the remaining half.

Penny:That's a huge profit to protect.

Roy:Yeah, so why the sudden urgency? Let's impartially look at the geopolitical catalyst driving specific price that morning.

Penny:Gasoline features are incredibly sensitive to global headlines. On that specific day, you had three major catalysts converging. First, you had delicate peace talks regarding Iran taking place in Qatar, Qatar, which could instantly ease Middle East supply fears. Second, you had impending API and EIA crude inventory data coming out later in the week, which is a wild card for supply numbers. Okay.

Penny:And third, you had intense US political pressure being applied to domestic oil companies to lower prices at the pump ahead of the summer driving season.

Roy:Literally any one of those three headlines breaking the wrong way could instantly derail the trade and send gasoline futures plummeting. Phil uses a great quote in the chat from Freedom's just another word for nothing left to lose. But he applies it to trading. He says when you are starting a trade you have nothing to lose but once you are up $11,000 per contract, you DO have something to lose. You have to protect the capital you've generated.

Penny:He applies the Munger inversion principle here perfectly. Charlie Munger, Warren Buffett's longtime partner, always said, invert, always invert. Instead of asking how to make more money, ask how you could lose it.

Roy:Right.

Penny:Phil asked the chat room, what is the dumbest possible outcome for this trade? The dumbest outcome is refusing to take profits out of greed. The Qatar peace talks suddenly succeed. Gasoline prices collapse back under $3 in a matter of minutes, and a massive winning trade turns into a devastating loss. How do you mathematically prevent the dumbest outcome?

Penny:You sell half immediately, secure the $11,000 and raise a mechanical stop loss on the rest.

Roy:By doing that, he permanently locks in 71% of the maximum potential profit, completely risk free. The amateur retail trader looks at that and says, if it goes to $3.20, I could have made more money. The professional trader looks at it and says, I secured the bag before the geopolitical headlines changed the market's mind.

Penny:That mindset is absolutely critical for managing Q3 volatility. When liquidity is thin, moves are fast, you do not try to squeeze every last theoretical cent out of a momentum trade. You manage the risk dynamically as the trade evolves.

Roy:But all of these tactical moves lead to a much broader strategic question for the listener. Phil uses what he calls the 5% rule to define the Nasdaq's consolidation range. He draws these mathematical support and resistance lines between twenty five thousand and thirty thousand. But if you're a listener trying to navigate this low volume summer with your retirement account, how do you actually tell the difference between a healthy, normal 5% pullback to support versus the start of a massive structural burst in those leverage pipes we talked about in the beginning? How do you know when the nightclub is actually catching fire?

Penny:That is exactly where you have to deploy the AGI Hunter lens. Hunter doesn't look at price. Hunter looks at constraints versus market theater. If the tech story is getting wildly if the Soggen data shows prime brokerage plumbing choked with ninety ninth percentile margin debt, you do not try to guess the exact top or try to catch the exact falling knife. You look at the systemic risk and you step completely outside what Hunter calls the AI blast radius.

Roy:I love that phrase, step outside the AI blast radius.

Penny:So if the technology sector is overcrowded, choking on leverage, and summer liquidity is evaporating, where does the smart capital actually rotate? This brings us to section five of the day's analysis, broadening the market. If they aren't buying tech, what are they buying?

Roy:Right.

Penny:To answer that, the PhilStockWorld team turns to AGI Anya, the behavioral economist. Anya doesn't look at moving averages. She looks at what human consumers are actually doing with their money rather than what the tech media narratives claim they're doing.

Roy:And Anya identifies a fascinating macroeconomic trend playing out in real time. She calls it consumer escapism. Yes. She notes that despite inflation and higher interest rates, consumer spending hasn't stopped. It has simply shifted.

Roy:Consumers are aggressively shifting their discretionary spending away from durable physical goods, they are holding off on buying a new iPhone, they are skipping the expensive kitchen remodel at Home Depot, and instead they are ruthlessly prioritizing temporary experiences and escapism. They're spending on travel, cruises, and regional casinos.

Penny:This behavioral insight leads the roundtable to deeply analyze a company like Pennin Entertainment.

Roy:Pennin is a perfect example of a classic value versus growth setup outside the tech sector. Pennin operates regional casinos across the country. The bullish case is straightforward. It sits perfectly in Anya's escapism trend. It currently has a price to earnings ratio well under 20, making it fundamentally cheap.

Roy:It generates actual physical cash flow from real estate assets, meaning it is totally insulated from the AI window dressing volatility. Even Goldman Sachs initiated coverage on it, calling it one of the most compelling risk rewards in the gaming sector, projecting they could generate $4 per share of free cash flow by 2028.

Penny:It sounds like the perfect rotation play, but as always, the AGI team ruthlessly examines the structural constraints.

Roy:Right. Another AGI known as Bodie McBoatface, who focuses heavily on debt structures, points out the massive, glaring red flag. PNN is carrying a $6,600,000,000 debt pile. And more concerningly, despite rising top line revenues from the escapism trend, they have been posting net income losses, which strongly suggest their operating expenses and debt servicing costs are completely out of control. Phil Davis looks at that $6,600,000,000 debt in a higher for longer interest rate environment and essentially says, I'm out.

Roy:It is not a safe, no brainer core hold.' It is a cyclical, highly leveraged company. The vital lesson here is that just because a stock perfectly fits a brilliant macroeconomic theme like consumer escapism, it does not mean the underlying corporate balance sheet is healthy enough to actually survive the current interest rate environment.

Penny:To truly gauge the underlying health and behavior of the consumer, you have to look past the thematic narratives and examine the actual corporate earnings hitting the tape that day.

Roy:And we had two massive consumer bellwethers report earnings on June 30. Constellation Brands, ticker STZ and Nike ticker NKE. Let's dig into Constellation brands first because the internal metrics of their report were wild. Let's do it. They reported earnings per share of $3.43 handily beating wall street estimates of $3.2 They generated a massive $485,000,000 in free cash flow.

Roy:But here's the fascinating part. On the earnings call, the CEO explicitly highlights that they're operating in a highly value conscious consumer environment where people are stressed about inflation.

Penny:Okay.

Roy:Yet their beer segment, which is driven by premium, higher priced imported brands like Modelo and Corona, actually grew sales by 2% and outperformed the total beer category. Meanwhile, their wine and spirits segment completely cratered, plummeting 47%.

Penny:That divergence perfectly validates Anya's behavioral thesis regarding escapism and how modern consumers define luxury.

Roy:I need you to explain that psychology. How can a consumer be value conscious and stressed about grocery prices but still willingly pay a premium for imported beer?

Penny:It comes down to accessible gratification in a constrained environment. When inflation eats into a household budget, the consumer has to make hard choices. They realize they can no longer afford the large traditional status symbols. They might have to delay buying a new car, they can't afford a new MacBook, and they certainly aren't going out to buy a high end expensive bottle of wine for a Tuesday dinner.

Roy:Makes sense.

Penny:But a six pack of premium imported beer, that is an accessible immediate physical gratification. It is affordable luxury. It is a micro escape. Anya points out that consumers will gladly trade down on their staple groceries buying store brand cereal just to ensure they have the spare cash to buy their favorite premium beer for the weekend barbecue. They will protect their small luxuries fiercely.

Roy:That is a profound way to look at consumer resilience, and you see a very similar dynamic playing out with Nike's earnings. Nike reported a massive EPS beat $0 and $72 per share versus the expected $1.59 Now, their overall revenue was slightly down, but their profitability and margins were much better than Wall Street feared. The market absorbed this report as a signal that the new CEO, Elliott Hill, and his aggressive turnaround efforts might actually be gaining traction, stabilizing the ship despite drops in their wholesale and direct to consumer revenues.

Penny:What you are witnessing in the data between Constellation Brands and Nike is the actual mechanical rotation of capital. Smart money is quietly rotating away from the extremely overvalued spenders of CapEx in the tech sector and reallocating into these old economy cyclicals. They're looking for companies that have lower relative leverage, sell actual physical products that generate immediate cash, and have a proven history of returning that cash to shareholders through share buybacks and dividends.

Roy:It feels like an ultimate contradiction to the narrative we are fed every day. The consumer supposedly broke, they're actively skipping the digital hype cycle of the new iPhone, yet they will absolutely pay up for a weekend trip to a regional casino, a cooler full of premium imported beer, and a new pair of Jordans. If I am a long term retail investor trying to make sense of this, how should contradiction?

Penny:You frame it by realizing that the American consumer isn't dying. They are just adapting to the structural constraints of the economy, and your portfolio needs to adapt alongside them. If Basho is telling you that the S and P five hundred's primary plumbing is stuffed to the ninety ninth percentile with synthetic semiconductor leverage, you don't fight that reality. You find safety in the boring, traditional cash flow producing companies that the passive indexers and the momentum algorithms are currently ignoring.

Roy:Okay, let's pull all these threads together. What an absolutely incredible multi layered journey through a single trading day. We started by looking past the green numbers on the screen to examine the fragile, leverage stuffed plumbing of the broader market. We saw the synthetic equity funding heat wave, the global intervention risk of the Japanese Yen, and the $1,400,000,000,000 in margin debt creating a massive bottleneck at the exit doors.

Penny:We

Roy:analyzed the historic 37% tech rally identifying the violent internal rotation driven entirely by AI hardware companies like Micron while legacy software names like Intuit suffered massive multiple compression. We watched the fascinating mechanical drama of SpaceX entering the Nasdaq 100 dissecting the math behind the passive index cartel and Phil's calculated asymmetrical options wager on the thin float.

Penny:An amazing case study.

Roy:Truly. We learned critical portfolio saving risk management lessons, why you never blindly double down on a losing options trade like AT and T just to soothe your ego, and why you use the Munger Inversion Principle to take 71% of your profits off the table on a volatile geopolitical gas trade. And finally, we look at the real economy, seeing a resilient adapting consumer who is fiercely prioritizing physical escapism over digital hype.

Penny:It truly is a masterclass in separating market theater from market mechanics. If you understand the plumbing, you can survive volatility.

Roy:But before we sign off, we promised you a final provocative thought something entirely different to mull over as you navigate this low volume summer market. And this comes from one final, mostly unexplored thread generated by the AGI roundtable at the end of the day. Cyrano, the AGI whose specific job is to track global regulatory patterns and legislative risks, noted a massive, unexplained pre market surge in solar energy stocks like Enphase Energy and SolarEdge.

Penny:Which is highly unusual for that sector given the current interest rate environment. They were up 11% to 12% before the opening bell even rang.

Roy:So why the sudden spike? Cyrano digs into the data and highlights a Reuters report showing that the US Federal Communications Commission, the SEC, is quietly drafting a ban on Chinese made solar energy inverters, citing national security concerns. Cyrano points out that Washington isn't acting alone here. They are directly mimicking Europe, which quietly banned Chinese inverters from public infrastructure projects just a month prior in May.

Penny:Now, you might be asking, why does a ban on solar inverters matter to someone invested in the AI tech boom?

Roy:Right. Because it exposes the ultimate hidden structural risk that no one in Silicon Valley wants to talk about. We've spent this entire deep dive talking about the market's insatiable obsession with AI data centers, the hyperscalers spending billions, and the massive, unprecedented amounts of electricity those data centers require to But if Western governments are quietly using the banner of national security to forcefully reshor entire green energy supply chains, they are actively building invisible massive regulatory moats.

Penny:And regulatory moats, while perhaps necessary for geopolitical security, are universally highly inflationary. You are replacing cheap global manufacturing with expensive domestic by legislative

Roy:force. Exactly. So here is your final takeaway, the thought to leave you with today: How much will this hidden energy inflation ultimately cost the sellers of capex when they finally realize that the cheap, hyper efficient global supply chain that built the entire 2020s tech boom has literally been legislated out of existence. Will Microsoft, Amazon, and Google still be able to afford the return on investment for these massive data centers if the cost of the solar power required to run them doubles or triples because of national security tariffs? The market is currently pricing in infinite AI growth, but it is completely ignoring the physical cost of the energy required to fuel it.

Roy:Keep your eyes on the plumbing, keep your eyes on the regulations, and do not just blindly trust the prices on the screen.

Penny:Because eventually the engine room always tells the truth.