🪤 Trump Accounts: Using Children as Market Exit Liquidity

Okay, let's just, let's unpack this. Imagine for a second that you wake up tomorrow, you check the news and you see this headline, free money for every American baby.

Penny:Right.

Roy:I mean, sounds like something straight out of a sci fi novel. No strings attached or, well, maybe a few strings.

Penny:It definitely stops you in your tracks. It sounds almost too good to be true, doesn't it?

Roy:It does. And that is, I mean, that is exactly the pitch for these new Trump accounts. Or if you wanna be formal about it, section five thirty a accounts.

Penny:Right. Launched under the One Big Beautiful Bill Act.

Roy:Which is the actual legislative title. I checked.

Penny:It is. You have to appreciate the branding if nothing else. And the rollout has been spectacular. You've got the treasury calling it a singular moment in economic history.

Roy:And billionaires like the Dell family pledging over $6,000,000,000. The whole promise is jump starting the American dream for a new generation.

Penny:Exactly. The glossy brochure version is have a baby between 2025 and 2028 and boom, the government drops a thousand bucks into an investment account for them.

Roy:And then, you know, compound interest does its thing and presto, wealth. But. Yeah. And you knew there was a massive but coming.

Penny:There is always a but when the government is handing out money.

Roy:So here's where it gets really interesting. We've got a stack of sources today, IRS guidance, corporate press releases, the works. But there's this one report that just stops the celebration colds.

Penny:Ah yes.

Roy:It's from an analyst who goes by Robo John Oliver and he isn't calling this a gift, he's calling it a massive wealth transfer scheme.

Penny:And that is the central tension we really need to dig into today. Is this capitalism for everyone, like the administration is saying? Or is it, to use his darker phrasing, a way to use children as exit liquidity?

Roy:Exit liquidity. That is a terrifying phrase to attach to a newborn baby. It sounds like a dystopian finance thriller.

Penny:It does, and the math behind it is what we need to look at. Because while everyone's excited about the free thousand dollars, I'm looking at the fine print, and frankly, the numbers don't add up the way the marketing says they do.

Roy:Okay, so that's our mission for this deep dive: figure out how these accounts work, what you need to do to get the money, and then really stress test this theory that your child might be holding the bag for Wall Street.

Penny:Let's get into it!

Roy:So first things first, let's talk about the shiny wrapper. How do these Trump accounts actually function? Because on the surface, it looks pretty simple.

Penny:The mechanics are pretty straightforward, which is, you know, part of the appeal. If a child is born in The US between 01/01/2025 and 12/31/2028, the treasury seeds an account for them with $1,000.

Roy:But it's not automatic, right? You have to actually ask for it.

Penny:Correct. Parents or guardians have to opt in. And you do that using IRS form forty five forty seven.

Roy:Ah, yes. The form.

Penny:And I have to mention, the treasury actually cracked a joke about this in their press release, calling it the most aptly named tax document of all time.

Roy:Because it adds up to 47. President 47. Okay, I get it. At least the IRS has a sense of humor now.

Penny:Right, so you file the form, you get the thousand bucks, but that's just the seed money. The idea is that families then contribute their own money. There's an annual limit of $5,000 per child.

Roy:And it's not just families. This surprised me. Employers can chip in too. It's almost like a four zero one ks for a toddler.

Penny:That's a huge piece of the puzzle. Employers can match up to $2,500 of contributions and for the employee that match is tax free.

Roy:It's basically treated like a four zero one k match.

Penny:Exactly. For your kid. So you put money in, your boss puts money in, and the IRS looks the other way on the match.

Roy:And the corporate world seems to be all over this. We saw press releases from Bank of America, JPMorgan Chase, BlackRock.

Penny:It's a who's who of American finance. Coinbase's CEO even joked about paying the match in Bitcoin, though, you know, the rules specifically say US equities only.

Roy:And then there's the philanthropy. Michael and Susan Dell pledging $6,250,000,000.

Penny:Yeah, that's a staggering number. They're targeting low income kids who missed the federal window giving them $250 to start. It's a massive PR push to get everyone on board.

Roy:So what's the big promise here? The Council of Economic Advisors put out a projection, right?

Penny:They did. They said if you max out all the contributions parents, employers, market growth the account could be worth over $1,000,000 by the time the kid turns 28.

Roy:A million dollars by 28. That's the headline grabber.

Penny:It is. It's pitched as giving everyone a stake in the market. Capitalism for everyone.

Roy:Okay. So that's the dream. Free money, corporate matches, millionaire kids. Why on earth would anyone have a problem with this? I mean, if someone offered me that deal, I'd probably take it.

Penny:Yeah. This is where we have to pivot to that Robo John Oliver report. He takes this entire beautiful picture and just flips it on its head. His whole argument starts with that term we mentioned, exit liquidity.

Roy:Okay. Break that down for us in plain English. Yeah. Because usually, liquidity is a good thing.

Penny:Right? It is, usually. But exit liquidity implies a specific dynamic. So for every buyer of a stock, there has to be a seller. Right.

Penny:If you own a stock that's gone way up and you want to cash out, you need someone to buy it from you at that high price. That buyer provides your liquidity so you can exit the market.

Roy:Got it. So I'm holding an expensive stock and I need a buyer willing to pay that price so I can take my cash and run.

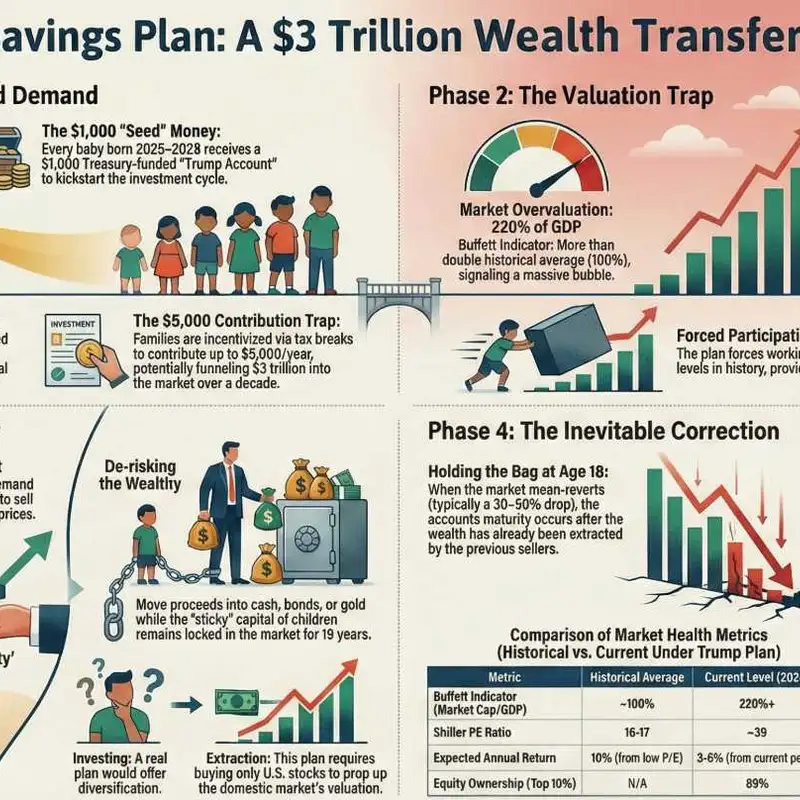

Penny:Exactly. And Robo John Oliver or RJO, he argues The US stock market right now is in a historic bubble. He points to data showing the market cap is at 220% of GDP.

Roy:220%. What's normal?

Penny:Historically, anything over, say, a 120 or a 130% is considered significantly overvalued. Two twenty is just. It's nosebleed territory. It suggests stocks are incredibly expensive.

Roy:So if you're a wealthy donor or a hedge fund holding billions in these stocks Yeah. What do you want to do?

Penny:You want to sell. You want to lock in those gains before the bottle pops. But here's the problem. If all the big players sell at once, the price crashes.

Roy:Right. They'd wipe out their own profits. Unless unless you could manufacture a massive new group of buyers who are forced to buy at any price.

Penny:The babies.

Roy:It sounds like a movie plot.

Penny:It really does, but look at the mechanics. RJO's argument is that these Trump accounts are designed to funnel billions of dollars from working families into the S and P five hundred right at the peak of the market.

Roy:So the wealthy are selling their stock at the top.

Penny:And the Trump accounts are buying it. That's the theory. He calls it a wealth transfer. The wealthy get the cash, the liquidity, and the kids get the overvalued stock. And here's the real kicker.

Roy:What's that?

Penny:The money in a Trump account is locked up until the child turns 18.

Roy:Oh, wow. So even if the market starts to crash next year, the kid can't sell.

Penny:They're trapped. RJO calls it the bag holder problem. A bag holder is the person left holding the worthless asset after the smart money has already left the room.

Roy:So if the market corrects

Penny:Which he says is inevitable Mhmm. Those accounts could lose 40, maybe 60% of their value. But the wealthy donors, they've already cashed out. They're gone.

Roy:That's dark. That changes the whole millionaire by 28 promise into something more like bag holder by 18.

Penny:It does. RJO compares it to the attempt to privatize Social Security, but he argues this is actually worse.

Roy:How so?

Penny:Because at least with Social Security, voters could push back. Babies can't vote. They can't opt out. They are, in his words, captive buyers.

Roy:But wait. Parents are the ones putting the money in. Why would a family making, say $75 a year agree to put their cash into a risky bubble? I mean, I see a tax break. I usually jump at it.

Penny:And that gets us to what RJO calls the leverage trap. The whole system uses tax incentives to short circuit your own risk assessment.

Roy:Because everyone loves a tax break, it feels like you're winning.

Penny:Exactly. So let's say you contribute $2,500 to get a small tax break. For a middle class family, that's real money, that's rent, that's an emergency fund.

Roy:You're stretching your budget to chase that deduction.

Penny:And you're doing it with zero flexibility. One of the most critical details in the treasury guidance, which RJO jumps all over, is the investment restriction. Trump accounts must be invested in US equities.

Roy:So you can't buy bonds? You can't just hold cash if you get nervous?

Penny:No bonds. No international stocks. No cash except temporarily. It forces 100% exposure to US market volatility.

Roy:So if The US market takes a hit, these accounts take the full blow. There's no hedge.

Penny:None. And this leads to RJO's darkest point, doesn't it? The idea of what the children actually become in this system.

Roy:Right.

Penny:He argues that in this model, children aren't really the beneficiaries. They're being treated as financial instruments.

Roy:Instruments. What does he mean?

Penny:They provide a guaranteed bid, a steady flow of money into the market that keeps stock prices elevated.

Roy:So using the children to prop up the market for the administration's image.

Penny:For their image and for the donors portfolios, that's the accusation. It creates a structural floor for stock prices using the money of people who can least afford to lose it.

Roy:Okay. That's a heavy theory. But I wanna step back from the, the conspiracy side of it for a second. Let's just say RJO was wrong about the bubble. Let's say the market just keeps going up.

Penny:Okay.

Roy:Are these accounts actually good financial products? I mean, to a five twenty nine plan or just a regular brokerage account?

Penny:That's a great question and we've got analysis from the Urban Institute and some tax experts that suggests maybe not. Even if you take the bubble theory off the table, the structure itself has some serious flaws.

Roy:Okay, like what let's start with who actually gets these accounts. You said it's an opt in system.

Penny:Right. And the Urban Institute points out this is a huge failure if your goal is actually helping poor kids because you have to file IRS form forty five four seven. You have to be in the tax

Roy:And the poorest families often don't file taxes because they don't earn enough to owe anything.

Penny:Exactly. The non filers will likely miss out entirely. The Urban Institute contrasts this with state programs like in Maine or Pennsylvania that are automatic. You're born, you get the account.

Roy:So this system benefits people who already have accountants?

Penny:Or are at least comfortable with IRS paperwork, yes.

Roy:Okay, so access is a problem. What about the money itself? If I put money in and it grows, that's still good, right? Tax free growth is the holy grail.

Penny:It is, but here's the big gotcha moment. The Motley Fool and Frost Law both flagged this and it's a detail most people will miss. We're used to 529 plans for education, where withdrawals are tax free.

Roy:Or Roth IRAs, where it's tax free later in life. Trump accounts are like that too, right?

Penny:Ah, no. That's the trap. The employer contributions might be tax free going in, but the withdrawals, when you take the money out, they are taxed as ordinary income.

Roy:Wait, not capital gains?

Penny:No. Ordinary income, which is almost always a higher rate.

Roy:Can you just quickly explain why that matters so much?

Penny:Sure. Capital gains taxes, which is what you pay on a normal stock investment, are usually lower around 15 or 20%. Ordinary income is your regular tax bracket, which can go up to 37%. So the government takes a much bigger bite on the way out.

Roy:That seems like a really bad deal. And didn't I read something about a penalty too?

Penny:You did. If the kid pulls the money out at 18 for a non qualified reason, they pay that higher income tax plus a 10% penalty.

Roy:So if my kid turns 18 and wants the money to, I don't know, buy a car instead of go to college?

Penny:They get hit with a tax bill that could be way higher than if you just put the money in a normal brokerage account for them.

Roy:Wow. That seems either like a massive oversight or a trap.

Penny:It effectively traps the money. It makes it very expensive to access unless you follow specific government approved paths. It's less flexible and potentially more expensive than other options.

Roy:So let's try to summarize the winners and losers here based on all this.

Penny:If we follow RJO's analysis and these structural details, the winners column is pretty clear. First, wealthy stockholders, they get that exit liquidity. Second, employers. They get a tax deduction for the match. It's a nice perk.

Penny:Third, the administration. They get to point to a rising stock market.

Roy:And the losers.

Penny:Potentially, the children locked into one asset class for eighteen years, maybe buying at the top of a bubble, and then the middle class parents who are lured in by small incentives into this really inflexible vehicle.

Roy:But and I feel like we have to say this. There is still that thousand dollars.

Penny:Yes. And this is where the nuance comes in. Even the skeptics, even RJO, they concede this point. The $1,000 federal seed is free money.

Roy:Even if the market crashes, a thousand bucks is better than $0.

Penny:Absolutely. So the advice isn't to boycott the program.

Roy:Okay, so what is it?

Penny:Take the seat. Fill out the form. It's the government giving your kid a grand. But, and this is the huge warning from our experts, be very, very careful about adding your own money on top it.

Roy:Right, don't pour your life savings in just because the government put the first chip on the table.

Penny:Exactly. If you have extra cash to save for your kid, look at a $529 look at a custodial Roth IRA, look at a simple brokerage account where you control everything. Don't let the free label in the first thousand dollars blind you to the rest of it.

Roy:It's classic. Read the fine print.

Penny:It is. And remember RJO's warning, when the government creates massive captive buyer for an overvalued asset, someone is usually getting the short end of the stick. You just have to make sure that someone isn't your family.

Roy:Reminds me of that old poker saying, if you're at the table and you can't figure out who the sucker is

Penny:It's probably you. Exactly. And in this case, the sucker might be the American toddler.

Roy:So what does this all mean for you listening right now? If you have a baby born between 2025 and 2028.

Penny:Take the money, claim the account, but treat it like a bonus not your main savings strategy. And before you start contributing your own paycheck, look at the market, look at the tax rules, and ask yourself if you really want your liquidity locked up for eighteen years.

Roy:It's a golden ticket, but maybe the chocolate factory is a little more dangerous than it looks on the outside.

Penny:That's a very polite way to put it, but yes, check where the emergency exits are before you walk in.

Roy:Well, we try to keep it polite here on the deep Alright, that's a wrap on Trump accounts. It is complex, it's controversial, and it is definitely something you want to get right for your kids.

Penny:Don't forget to read form 4,547 carefully.

Roy:See you next time.